Embarking on the journey to homeownership is an exciting prospect, and for many, the 30-year fixed-rate mortgage stands out as the most popular financing choice. Its extended repayment period offers the appeal of lower monthly payments, making homeownership more accessible and budget-friendly. Understanding today’s 30 year loan rates is crucial for securing a favorable deal, as these rates directly impact the affordability and long-term cost of your home. This comprehensive guide will walk you through everything you need to know, from understanding how these loans work to finding the most competitive rates available.

Understanding 30-Year Mortgage Loans

A 30-year mortgage is a home loan repaid over three decades, typically with a fixed interest rate. This means your principal and interest payments remain constant for the entire 360 months, providing remarkable stability and predictability for your budget. Unlike shorter-term loans, the extended repayment schedule significantly reduces the size of your monthly obligations, making it a preferred option for first-time homebuyers and those looking for payment predictability.

Advantages of 30-Year Mortgages

The widespread popularity of 30-year mortgages is due to several key benefits they offer to borrowers.

- Lower Monthly Payments: Spreading the loan over a longer period results in smaller monthly installments, improving cash flow and making homeownership more affordable.

- Financial Flexibility: Lower payments free up funds that can be used for other financial goals, such as saving for retirement, investing, or handling unexpected expenses.

- Predictability: With a fixed interest rate, your principal and interest payment remains the same, protecting you from market fluctuations and making budgeting straightforward.

- Tax Deductions: Mortgage interest can often be tax-deductible, offering a potential financial advantage for homeowners.

Disadvantages of 30-Year Mortgages

While offering significant advantages, 30-year mortgages also come with certain drawbacks that borrowers should consider.

- Higher Total Interest Paid: Over 30 years, you will typically pay significantly more in total interest compared to a 15-year mortgage, even if the interest rate is similar.

- Slower Equity Build-Up: A larger portion of your early payments goes towards interest, meaning you build equity in your home at a slower pace initially.

- Longer Commitment: A three-decade commitment is substantial, and your financial circumstances may change significantly over that time.

Key Factors Influencing 30 Year Loan Rates

30 year loan rates are not static; they fluctuate daily based on a complex interplay of economic forces and individual borrower characteristics. Understanding these factors can help you make informed decisions when applying for a mortgage and seeking competitive rates.

Economic Indicators

Broader economic conditions play a significant role in determining mortgage rates. Key indicators include:

- Federal Reserve Policy: While the Fed doesn’t directly set mortgage rates, its actions on the federal funds rate influence the overall cost of borrowing.

- Inflation: Lenders typically demand higher interest rates during periods of high inflation to protect the real value of their returns.

- Bond Yields: Mortgage rates often move in tandem with the yield on 10-year Treasury bonds, as they compete for investor attention.

Borrower-Specific Factors

Your personal financial profile heavily influences the interest rate you’ll be offered.

- Credit Score: A higher credit score (generally 740 and above) signals lower risk to lenders, leading to more favorable interest rates.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, often resulting in lower rates and potentially avoiding private mortgage insurance (PMI).

- Debt-to-Income (DTI) Ratio: Lenders assess your DTI to ensure you can comfortably manage your monthly mortgage payments alongside existing debts. A lower DTI is preferable.

- Loan Type: Different loan types (Conventional, FHA, VA, USDA) have varying eligibility criteria and rate structures.

Step-by-Step Guide to Securing the Best 30 Year Loan Rates

Finding the most competitive 30 year loan rates requires a strategic approach. Follow these steps to maximize your chances of securing a great deal.

- Assess Your Financial Health: Before approaching lenders, review your credit report for inaccuracies, improve your credit score if needed, and calculate your debt-to-income ratio. The stronger your financial profile, the better rates you’ll attract.

- Shop Around Extensively: This is perhaps the most crucial step. Don’t settle for the first offer. Contact multiple lenders—banks, credit unions, and mortgage brokers—to compare their rates and terms. Utilize online comparison tools to broaden your search.

- Get Pre-Approved: A pre-approval letter not only shows sellers you’re a serious buyer but also gives you a clear idea of how much you can borrow and at what rate. It helps lock in a rate for a limited period, protecting you from sudden market upticks.

- Understand Rate Locks: A rate lock guarantees your interest rate for a specific period (e.g., 30, 45, or 60 days) while your loan processes. Discuss the terms and any associated fees with your lender.

- Review Loan Estimates Carefully: Once you apply for a mortgage, lenders are required to provide a Loan Estimate within three business days. This document details the interest rate, monthly payment, and estimated closing costs. Compare these estimates from different lenders side-by-side. The Consumer Financial Protection Bureau (CFPB) provides excellent resources on how to compare these documents effectively. You can learn more at consumerfinance.gov.

- Negotiate Terms: Don’t be afraid to leverage competing offers. If one lender offers a lower rate or fewer fees, ask other lenders if they can match or beat it.

How Mortgage Payments Are Calculated (The Simple Way)

While the underlying math can be complex, understanding your mortgage payment is straightforward: it’s determined by your loan amount, the interest rate, and the loan term. For a 30-year fixed-rate mortgage, the monthly principal and interest payment remains constant throughout the loan’s life. This allows for predictable budgeting.

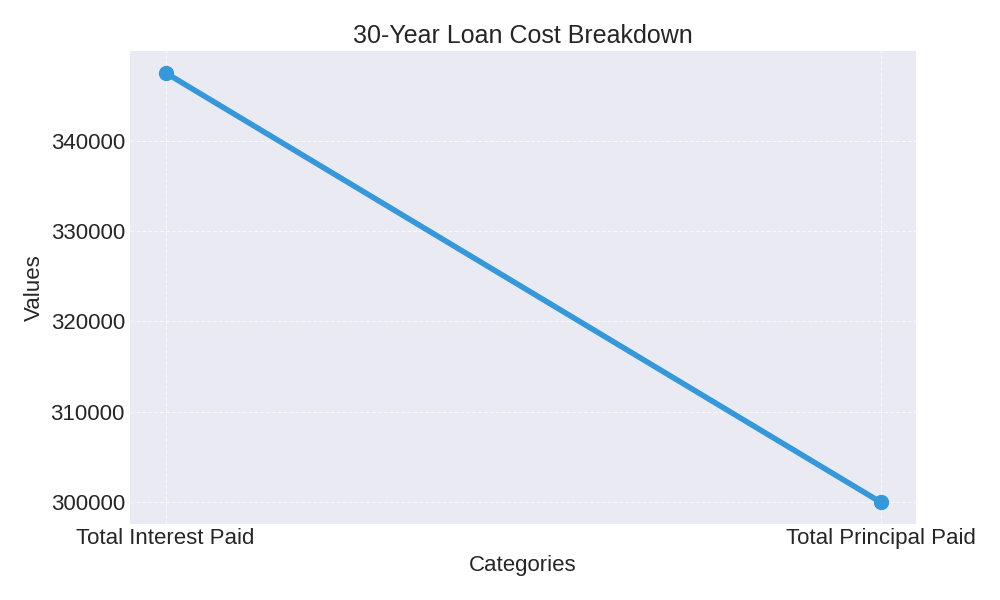

For example, if you borrow $300,000 at a 6.00% annual interest rate for a 30-year term, your monthly principal and interest payment would be approximately $1,798.65. Over the life of the loan, you would pay a total of $647,514, with $347,514 of that being interest. This simple calculation highlights the long-term cost of borrowing, which is crucial for financial planning.

| Loan Term | Approx. Remaining Balance | Monthly P&I Payment |

|---|---|---|

| Start (Month 0) | $300,000.00 | $1,798.65 |

| Year 5 (Month 60) | $276,467.22 | $1,798.65 |

| Year 15 (Month 180) | $209,726.49 | $1,798.65 |

| Year 30 (Month 360) | $0.00 | $1,798.65 |

Monthly Payment Calculator

FAQ: Your Questions About 30 Year Loan Rates Answered

What is considered a “good” 30 year loan rate?

A “good” rate is highly subjective and depends on the current market environment, your financial profile, and prevailing economic conditions. What might be an excellent rate today could be average in a different market. Always compare offers from multiple lenders to determine what’s competitive for your specific situation. Reviewing historical data from sources like the Federal Reserve can provide context.

Can I refinance a 30-year mortgage?

Yes, refinancing is a common strategy. If interest rates drop significantly after you’ve secured your mortgage, or if your credit score has improved, refinancing allows you to replace your existing loan with a new one, often with a lower interest rate or different terms. This can reduce your monthly payments or the total interest paid over time.

Is a fixed-rate 30-year loan always better than an adjustable-rate mortgage (ARM)?

Not always. A fixed-rate loan offers predictability and stability, protecting you from rising rates. An ARM, however, may offer a lower initial interest rate for a few years, which can be beneficial if you plan to sell your home or refinance before the rate adjusts. Your choice depends on your financial goals, risk tolerance, and anticipated housing timeline.

What are closing costs, and do they affect my 30 year loan rates?

Closing costs are fees paid at the closing of a real estate transaction. They include various charges such as origination fees, appraisal fees, title insurance, and more. While closing costs don’t directly affect your interest rate, they are an essential part of the overall cost of your mortgage. Sometimes, you can “buy down” your interest rate by paying extra closing costs, known as points. Compare options at sites like Bankrate for an overview.

How does my credit score affect my interest rate?

Your credit score plays a key role in determining the interest rate lenders offer you. A higher credit score signals lower risk, which often results in lower interest rates and better loan terms. Conversely, a lower score may lead to higher rates, increasing the overall cost of borrowing. Even a small difference in interest rates can significantly impact long-term payments. Maintaining a strong credit profile helps you access more affordable financing options and greater financial flexibility.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.