Do you ever feel like you’re constantly treading water, barely keeping your head above the rising tide of debt? You’re not alone. The weight of a significant loan can be crushing, turning dreams of financial freedom into a constant struggle. Perhaps you lie awake at night, staring at the ceiling, replaying interest rates and minimum payments in your mind. That nagging feeling of being trapped, the stress of endless bills, and the fear that you’ll never truly get ahead – these are the heavy burdens that countless individuals carry every single day because of debt.

It’s an exhausting cycle, but it’s not a life sentence. This article isn’t about shaming you or offering quick fixes. Instead, it’s an empathetic guide, a compassionate roadmap designed to help you understand your situation, reclaim control, and chart a clear course toward becoming debt-free. We’re going to explore practical, actionable strategies to break free from the grip of your loan obligations and build a more secure financial future. Your escape plan starts here.

Understanding Your Debt Landscape

Before you can construct an effective escape route, you need to understand the terrain. This means facing your debt head-on, no matter how uncomfortable it might feel. Ignoring it only allows it to grow silently, like a vine strangling your financial well-being.

The Pain Points

The emotional and practical toll of debt is immense. You might experience chronic stress, anxiety, or even depression. The constant pressure of payments can strain relationships, limit opportunities for personal growth, and prevent you from saving for crucial life events like retirement or your children’s education. It erodes your sense of security and freedom, making every financial decision feel like a gamble. Acknowledge these feelings; they are valid.

Getting a Clear Picture

The first practical step is to create a detailed inventory of all your outstanding loans and other debts. This isn’t about judgment; it’s about clarity. Gather statements for every credit card, personal loan, mortgage, student loan, or auto financing you have. For each debt, write down the following key pieces of information:

- Type of Debt: Is it a credit card, personal loan, mortgage, etc.?

- Lender: Who do you owe money to?

- Current Balance: The total amount you still owe.

- Interest Rate: This is crucial. Knowing which debts carry the highest interest will inform your strategy.

- Minimum Monthly Payment: What you absolutely must pay to avoid late fees.

- Due Date: When each payment is expected.

This comprehensive list will serve as your war map, showing you exactly what you’re up against. It might seem daunting at first, but having this information organized is the cornerstone of your escape plan.

Crafting Your Escape Strategy

With a clear understanding of your debt, you can now begin to formulate a plan. This involves strategic budgeting, choosing a repayment method, and understanding the mechanics of your loan.

Budgeting for Freedom

A budget isn’t about deprivation; it’s about empowerment. It’s a tool that gives you control over your money, allowing you to intentionally direct funds towards debt repayment. Start by tracking every dollar you earn and every dollar you spend for at least a month. Categorize your expenses into fixed (rent, loan payments) and variable (groceries, entertainment). Look for areas where you can cut back, even temporarily.

Every dollar you free up from discretionary spending can be redirected towards your debt, accelerating your journey to freedom. Think of it as “found money” dedicated to your escape. For practical help with creating a budget, resources like NerdWallet offer excellent tools and guidance.

The Avalanche vs. Snowball Methods

Once you have extra funds, how do you best apply them? Two popular strategies offer different approaches:

- The Debt Avalanche: This method focuses on efficiency. You make minimum payments on all debts except the one with the highest interest rate. All extra money goes towards that high-interest debt until it’s paid off. Then, you roll that payment (minimum + extra) into the next highest interest debt. This method saves you the most money on interest over time.

- The Debt Snowball: This method focuses on motivation. You make minimum payments on all debts except the one with the smallest balance. All extra money goes towards that small debt until it’s paid off. Then, you roll that payment (minimum + extra) into the next smallest debt. This method provides quicker wins, which can be incredibly motivating for those who need psychological boosts to stay committed.

Choose the method that best suits your personality and financial discipline. Both are effective, but one might resonate more with your approach to tackling big challenges.

Understanding Your Loan Repayment

Understanding how your loan is repaid, specifically through a process called amortization, is key. When you make a monthly payment on a loan, a portion goes towards the interest you owe, and another portion goes towards reducing the principal (the original amount you borrowed). Early in a loan’s term, a larger share of your payment often goes to interest. Over time, as the principal balance decreases, more of your payment is applied to the principal.

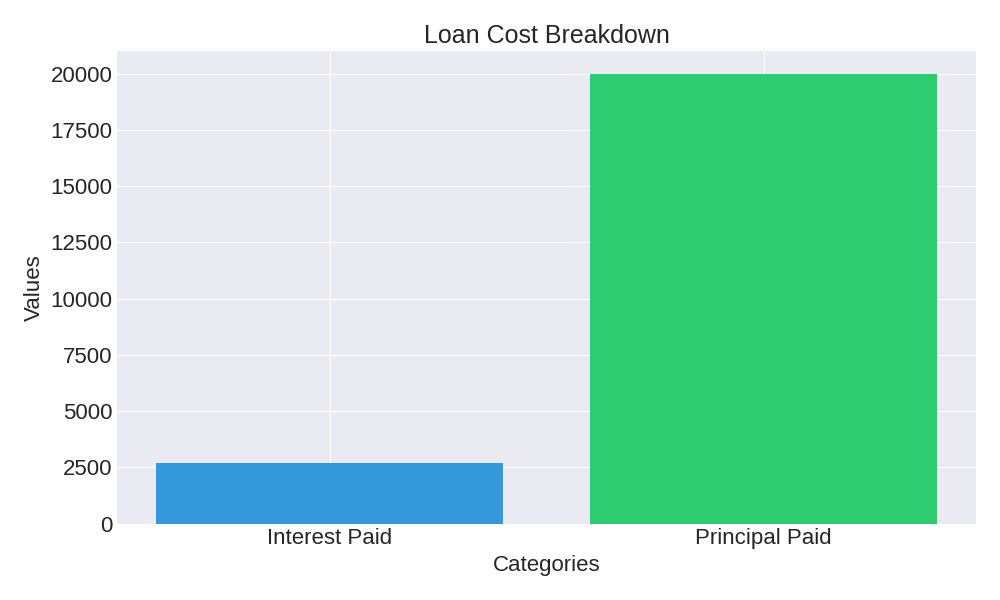

Let’s look at a concrete example. If you borrow $20,000 for 5 years at a 5% annual interest rate, your monthly payment would be approximately $377.42. Over the entire 5-year term, you would pay back your original $20,000 principal plus about $2,645.20 in interest, totaling $22,645.20.

Here’s a simplified look at how the balance and cumulative interest paid would decrease over time for this example:

| Year | Remaining Balance | Cumulative Interest Paid |

|---|---|---|

| 0 (Start) | $20,000.00 | $0.00 |

| 1 | $16,391.85 | $920.89 |

| 2 | $12,603.52 | $1,661.60 |

| 3 | $8,625.97 | $2,213.09 |

| 4 | $4,448.95 | $2,565.11 |

| 5 | $0.00 | $2,645.20 |

Monthly Payment Calculator

Accelerating Your Escape

Beyond budgeting and choosing a repayment strategy, there are powerful tools you can use to significantly speed up your debt repayment journey.

Refinancing and Consolidation

If you have multiple high-interest debts, exploring options like refinancing or consolidation could be beneficial. Debt consolidation involves taking out a new loan to pay off several smaller debts, leaving you with just one monthly payment. Refinancing is similar, but it specifically means taking out a new loan to replace an existing one, usually to secure a lower interest rate or different terms.

These strategies can simplify your payments and, crucially, potentially reduce the total interest you pay over the life of the loan. However, be cautious: ensure the new terms truly benefit you, and watch out for hidden fees or extending the repayment period so much that you end up paying more in interest despite a lower rate. Resources like the Federal Reserve provide impartial information on these financial products.

Increasing Your Income

Sometimes, simply cutting expenses isn’t enough. Actively seeking ways to boost your income can pour gasoline on your debt repayment fire. Consider a temporary side hustle, selling items you no longer need, negotiating a raise at your current job, or even taking on extra shifts. Every additional dollar you earn can be directly funneled into your debt repayment plan, shaving months, or even years, off your debt journey. This isn’t about working yourself to exhaustion, but strategically using your time and skills to accelerate your financial freedom.

The Power of Extra Payments

Even small extra payments can have a dramatic impact. Imagine you have a $10,000 personal loan at 7% interest over 4 years. Your monthly payment is about $239. Adding just $50 to that payment each month could reduce your repayment time by nearly a year and save you hundreds in interest. The sooner you pay down the principal, the less interest accrues over time. This principle is a powerful accelerant for any debt repayment plan.

Maintaining Momentum and Future Proofing

Getting out of debt is a huge accomplishment, but staying out requires ongoing vigilance and smart financial habits. This phase is about building resilience and preventing future debt traps.

Building an Emergency Fund

Once you start seeing significant progress on your debt, it’s critical to shift some focus to building an emergency fund. Life is unpredictable; car repairs, medical emergencies, or job loss can quickly derail your progress and force you back into debt. Aim to save at least three to six months’ worth of essential living expenses in an easily accessible, separate savings accoun

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.