Embarking on the journey to homeownership is an exciting prospect, and one of the most critical elements you’ll encounter is understanding the rate for home loan. Securing a favorable mortgage interest rate can save you tens of thousands of dollars over the life of your loan, significantly impacting your monthly budget and overall financial health.

This comprehensive guide will walk you through everything you need to know about navigating the world of mortgage rates, ensuring you’re empowered to find the lowest possible rate for home loan for your dream home. Knowing your options and what influences your potential interest rate is the first step toward making an informed decision.

Understanding Your Home Loan Rate

The interest rate is essentially the cost of borrowing money from a lender. When you take out a mortgage, the interest rate dictates how much extra you’ll pay each month on top of the principal amount you borrowed. A small difference in your rate can lead to substantial savings or additional costs over 15 or 30 years.

What is a Mortgage Interest Rate?

A mortgage interest rate is expressed as a percentage of the principal loan amount. This percentage is the fee you pay to the lender for the privilege of borrowing their money. It’s crucial to distinguish between the interest rate and the Annual Percentage Rate (APR). While the interest rate reflects just the cost of borrowing the principal, the APR includes the interest rate plus other loan costs, such as points, mortgage broker fees, and other charges. The APR provides a more comprehensive picture of the true cost of your loan.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

When selecting a mortgage, you’ll generally choose between two main types:

- Fixed-Rate Mortgage: With a fixed-rate mortgage, your interest rate remains the same for the entire term of the loan, typically 15 or 30 years. This offers predictable monthly payments, making budgeting easier and protecting you from future interest rate increases. It’s ideal for homeowners who prefer stability and plan to stay in their home long-term.

- Adjustable-Rate Mortgage (ARM): An ARM typically starts with a lower interest rate for an initial period (e.g., 3, 5, 7, or 10 years). After this introductory period, the rate adjusts periodically based on an economic index. While ARMs can offer lower initial payments, they carry the risk of higher payments if rates rise in the future. They might be suitable for those who plan to sell or refinance before the adjustable period begins.

Factors Influencing Your Rate for Home Loan

Several key factors determine the interest rate you qualify for. Understanding these can help you position yourself to receive the most competitive offer possible. Lenders assess risk, and your financial profile dictates how risky you appear.

Your Credit Score

Your credit score is one of the most significant determinants of your mortgage rate. A higher credit score (generally 740 and above) signals to lenders that you are a responsible borrower, resulting in lower interest rates. Conversely, a lower score indicates higher risk and will likely lead to a higher rate. It’s wise to check your credit report and score well in advance of applying for a mortgage.

Down Payment Amount

The size of your down payment directly impacts your loan-to-value (LTV) ratio. A larger down payment reduces the amount you need to borrow and, consequently, reduces the lender’s risk. This often translates into a lower interest rate. A down payment of 20% or more also typically helps you avoid private mortgage insurance (PMI).

Loan-to-Value (LTV) Ratio

The LTV ratio compares the amount of your loan to the appraised value of the home. For example, a $160,000 loan on a $200,000 home results in an 80% LTV. A lower LTV (meaning a larger down payment) generally qualifies you for a better interest rate because there’s less risk for the lender.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio measures how much of your monthly gross income goes towards paying debts. Lenders typically prefer a DTI ratio of 36% or less, though some programs allow up to 43% or higher. A lower DTI ratio indicates you have more disposable income to cover your mortgage payments, making you a less risky borrower and potentially qualifying you for a lower rate.

Loan Term and Type

The length of your mortgage (e.g., 15-year vs. 30-year) also affects the interest rate. Shorter-term loans generally come with lower interest rates because the lender’s risk is spread over a shorter period. Additionally, government-backed loans (FHA, VA, USDA) may offer different rates compared to conventional loans, often targeting specific borrower groups or financial situations.

Economic Conditions

Broader economic factors play a huge role in the prevailing mortgage rates. The Federal Reserve’s monetary policy, inflation, and the bond market directly influence where mortgage rates stand. When the economy is strong and inflation is a concern, rates tend to rise. Conversely, during economic slowdowns, rates may fall. Keep an eye on economic indicators and reports from the Federal Reserve for insights into market trends.

Step-by-Step Guide to Securing the Best Rate

Finding the most competitive rate for home loan requires diligence and strategic planning. Follow these steps to maximize your chances of securing an excellent deal.

- Check Your Credit Score and Report: Obtain your credit report from all three major bureaus (Experian, Equifax, TransUnion) and dispute any errors. Aim to improve your score by paying down debt and avoiding new credit inquiries before applying.

- Determine Your Budget and Affordability: Before shopping for rates, understand how much house you can truly afford. Factor in not just the mortgage payment, but also property taxes, homeowner’s insurance, and potential HOA fees.

- Save for a Larger Down Payment: As discussed, a larger down payment can significantly lower your interest rate and reduce your overall loan costs. Aim for at least 20% if possible.

- Shop Around and Compare Lenders: Don’t settle for the first offer. Contact multiple lenders—banks, credit unions, and mortgage brokers—to compare their rates, fees, and loan programs. Even a difference of 0.25% can save you thousands.

- Understand Closing Costs and APR: When comparing offers, look beyond just the interest rate. Compare the Annual Percentage Rate (APR), which includes most fees, to get a clearer picture of the total cost. Also, scrutinize the closing costs associated with each loan. The Consumer Financial Protection Bureau (CFPB) offers resources to help you understand these costs.

- Lock Your Rate: Once you find a satisfactory rate, ask your lender about “locking” it in. A rate lock guarantees your quoted interest rate for a specific period (e.g., 30-60 days) while your loan application is processed, protecting you from potential rate increases.

Calculating Your Mortgage Payments (Simplified)

While the exact mathematical formulas for calculating mortgage payments can be complex, understanding the principle is straightforward. If you borrow a certain amount at a given interest rate for a specific term, you will have a fixed monthly payment that includes both principal and interest. Initially, a larger portion of your payment goes towards interest; as the loan matures, more goes towards paying down the principal.

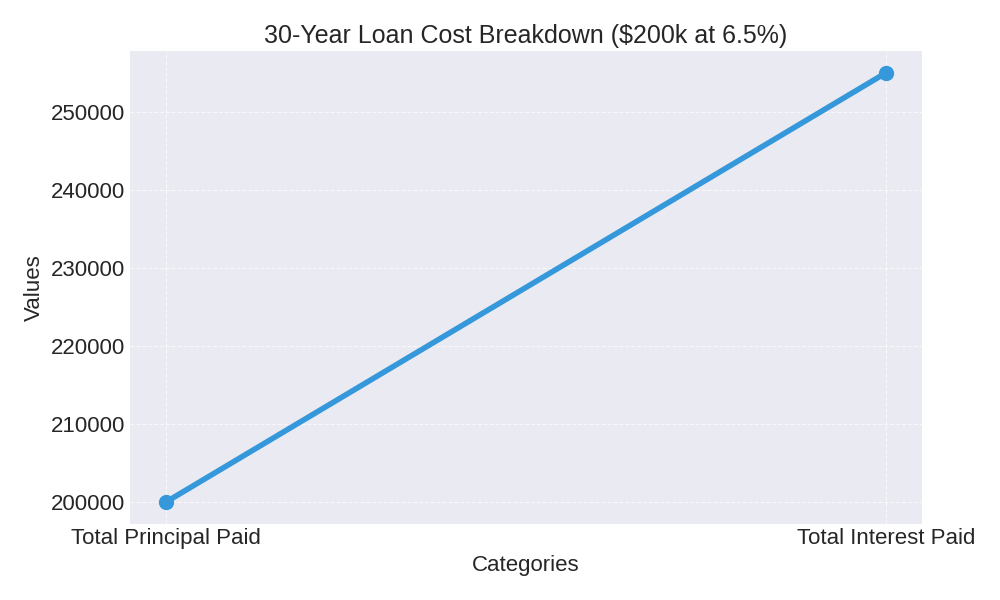

For example, if you borrow $200,000 for a 30-year fixed mortgage at an interest rate of 6.5%, your monthly principal and interest payment would be approximately $1,264. This means over 30 years, you would pay back your original $200,000 plus an additional $255,040 in interest, totaling $455,040.

| Year | Remaining Balance | Monthly Payment (P&I) |

|---|---|---|

| 0 (Initial) | $200,000.00 | – |

| 1 | $197,358.00 | $1,264.12 |

| 5 | $185,556.00 | $1,264.12 |

| 10 | $165,835.00 | $1,264.12 |

| 20 | $104,821.00 | $1,264.12 |

| 30 (Final) | $0.00 | $1,264.12 |

Monthly Payment Calculator

FAQ About Home Loan Rates

Here are answers to some frequently asked questions about mortgage interest rates.

- Q: How often do mortgage rates change?

A: Mortgage rates can change daily, sometimes even multiple times a day. They are influenced by economic news, bond market performance, and signals from the Federal Reserve. - Q: What is a “point” in a mortgage?

A: A point, also known as a discount point, is a fee paid to the lender at closing to “buy down” your interest rate. One point typically equals 1% of the loan amount. For example, on a $200,000 loan, one point would be $2,000. - Q: Can I negotiate my mortgage interest rate?

A: While lenders have standard rates, there is often some room for negotiation, especially if you have a strong credit profile and are comparing offers from multiple lenders. Don’t hesitate to ask if a lender can beat a competitor’s offer or waive certain fees in exchange for a slightly higher rate, or vice-versa.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.