Are you feeling trapped in a relentless cycle of debt, dreading the next bill, and constantly scrambling to cover essential expenses? You’re not alone. Many individuals find themselves overwhelmed by the burden of high-interest credit, especially when facing the pressures of a looming loan pay day. That feeling of relief from quick cash often gives way to a crushing weight, as astronomical interest rates make repayment seem impossible.

If you’ve been caught in the whirlpool of short-term loans, juggling payments, and seeing your financial future dim, this article is for you. We understand the stress, the sleepless nights, and the desperate search for a way out. This isn’t just about money; it’s about reclaiming your peace of mind and building a stable future. Let’s explore how you can escape the grasp of burdensome debt and find real, lasting solutions.

Understanding the Cycle of High-Interest Debt

You might have initially turned to a short-term loan out of necessity. Perhaps an unexpected car repair, a medical emergency, or a sudden gap in income left you with no other perceived option. These loans promise fast cash with minimal hassle, making them seem like a lifeline in urgent situations. However, this immediate relief often comes at a steep price, ensnaring you in a debt trap that’s incredibly difficult to escape.

The Immediate Relief, The Long-Term Trap

The appeal of a quick cash injection is undeniable when you’re facing a crisis. Lenders often market these products as a convenient solution for bridging financial gaps until your next paycheck arrives. What isn’t always clear upfront, or easily understood in a moment of desperation, is just how quickly these loans can compound. You might pay off one loan only to immediately take out another, simply to cover new expenses or even the interest on the previous one. This creates a relentless cycle where you’re perpetually borrowing to pay off old debt.

Sky-High Interest Rates

One of the most insidious aspects of many short-term loans is their exorbitant interest rates. While traditional loans might have annual percentage rates (APRs) ranging from 5% to 36%, some short-term loans can carry APRs in the triple digits, sometimes even exceeding 400%. This means that borrowing a relatively small amount, say $500, can quickly balloon into a much larger sum due to interest alone. You end up paying significantly more than the original principal, effectively throwing money away that could have been used to improve your financial standing. Understanding these high costs is the first step toward breaking free.

Recognizing the Red Flags

It’s crucial to honestly assess your situation. Are you merely experiencing a temporary crunch, or have you slipped into a pattern of reliance on high-interest credit? Recognizing the signs of a problematic debt cycle is essential for seeking help before the situation becomes unmanageable. If you identify with several of these points, it’s a strong indicator that it’s time to take decisive action.

- You rely on high-interest loans to cover recurring expenses like rent, utilities, or groceries.

- You frequently extend or roll over existing loans, incurring additional fees and interest charges.

- You’re using one loan to pay off another, creating a constant merry-go-round of debt.

- Your credit score is declining, making it harder to access more affordable traditional credit options.

- You feel constant stress, anxiety, or guilt about your financial situation.

- You’ve started hiding your financial struggles from family or friends.

- You’re receiving frequent calls or letters from collectors.

If these sound familiar, remember that acknowledging the problem is the most courageous step you can take. You have options, and there’s help available to guide you towards financial stability.

Your Path to Freedom: Actionable Solutions

Breaking free from the grip of high-interest debt requires a multi-faceted approach. There’s no single magic bullet, but a combination of strategies can significantly improve your situation. The key is to be proactive and persistent. Let’s explore some proven methods to help you regain control.

Reaching Out for Professional Help

One of the most effective first steps is to seek guidance from a non-profit credit counseling agency. These agencies offer free or low-cost advice on managing your money and debt. They can review your entire financial situation, help you create a realistic budget, and explore debt relief options tailored to your specific needs. They can also mediate with creditors on your behalf, sometimes negotiating lower interest rates or more manageable payment plans. For reliable, unbiased advice, consider reaching out to organizations like the Federal Trade Commission (FTC) for consumer protection resources.

Debt Consolidation and Refinancing

Consolidating your debt can be a game-changer, especially when dealing with multiple high-interest loans. This involves taking out a new, lower-interest loan to pay off all your existing debts. The goal is to replace several high-cost payments with a single, more affordable monthly payment at a significantly lower interest rate. This simplifies your finances and can save you thousands of dollars in interest over time.

If your credit score has improved since taking out the initial loans, or if you have collateral, you might qualify for a personal loan from a bank or credit union. Another option could be a balance transfer credit card with an introductory 0% APR, though these require strict discipline to pay off the balance before the promotional period ends. Learn more about debt consolidation options on sites like NerdWallet.

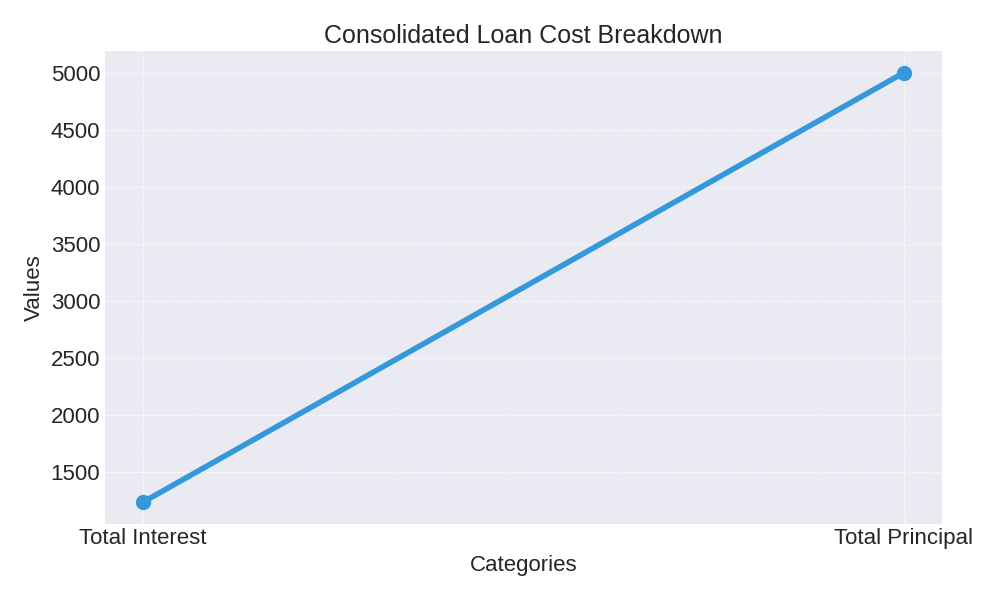

To illustrate the power of debt consolidation, consider this example: if you’re struggling with $5,000 in high-interest loans, consolidating it into a personal loan with a 15% APR over three years can dramatically reduce your monthly payments and total interest paid. Here’s a simplified view of how your payments would reduce your balance:

| Time Point | Remaining Loan Balance | Monthly Payment |

|---|---|---|

| Start (Month 0) | $5,000.00 | N/A |

| After 12 Months | $3,633.47 | $173.33 |

| After 24 Months | $2,188.15 | $173.33 |

| After 36 Months | $0.00 | $173.33 |

Monthly Payment Calculator

As you can see, a consistent monthly payment systematically reduces your principal balance, leading to a clear end date for your debt. Over the three-year term, your total payments would amount to approximately $6,239.88, meaning you’d pay around $1,239.88 in interest. Compare this to the potentially thousands you could pay on a revolving door of high-interest loans.

Negotiating with Lenders

If you’re severely behind on payments, directly contacting your lenders can sometimes lead to a solution. Some lenders may be willing to work with you, especially if you demonstrate a genuine effort to repay. They might offer a temporary hardship plan, reduce your interest rate, or even settle for a lower lump-sum payment if you’re in a position to do so. This is often an option when the lender believes recovering some money is better than recovering none.

Budgeting and Financial Planning

Beyond addressing existing debt, a fundamental step is creating and sticking to a realistic budget. Understanding exactly where your money goes each month is empowering. Track your income and expenses to identify areas where you can cut back. Even small changes, like cutting down on non-essential subscriptions or dining out less frequently, can free up funds to put towards debt repayment. A solid budget is your roadmap to financial stability, preventing you from falling back into debt after you’ve worked so hard to get out.

Building a Stronger Financial Future

Escaping the debt cycle is just the beginning. The next crucial step is to build a robust financial foundation that protects you from future emergencies and reduces the temptation of short-term, high-interest loans. This proactive approach ensures that your hard-won freedom from debt lasts.

Emergency Fund First

A primary reason people turn to quick cash solutions is the lack of an emergency fund. Aim to build a savings cushion covering at least three to six months of essential living expenses. This fund acts as your personal financial safety net, allowing you to handle unexpected costs—like job loss, medical bills, or car repairs—without resorting to high-cost borrowing. Start small, even $10 or $20 a week, and gradually increase your contributions. The Consumer Financial Protection Bureau (CFPB) offers excellent resources on managing your money and saving effectively.

Understanding Your Credit

Your credit score plays a vital role in your financial life. A good credit score can unlock access to more affordable loans, better interest rates, and even impact things like insurance premiums and housing applications. Regularly check your credit report for errors and understand the factors that influence your score. Making on-time payments, keeping credit utilization low, and avoiding new unnecessary debt are all critical for building and maintaining healthy credit. This will be invaluable should you ever need to borrow responsibly in the future.

Conclusion

Breaking free from the burden of high-interest debt, especially the relentless cycle of a loan pay day, is an achievable goal. It requires courage, commitment, and a willingness to seek and accept help. You don’t have to navigate these challenges alone. By understanding your situation, exploring debt consolidation, negotiatiating with creditors, and building healthier financial habits, you can regain control of your finances. Each step you take toward reducing debt and strengthening savings brings you closer to lasting financial stability. Remember that progress may be gradual, but consistency is what creates meaningful change. With the right tools, support, and mindset, you can move beyond short-term solutions and build a more secure, confident financial future.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.