Life has an uncanny way of throwing unexpected financial curveballs. A sudden car repair, an unforeseen medical bill, or an urgent home appliance breakdown can quickly derail a carefully managed budget. When these moments hit, and your next paycheck feels a lifetime away, the stress can be overwhelming. Staring at immediate bills with no clear path to funds is not just an inconvenience; it’s a genuine pain point that impacts peace of mind and can lead to desperate measures. Many individuals find themselves in this predicament, wondering how to bridge the gap until their next direct deposit.

In such scenarios, a payroll loan may appear as a rapid, albeit potentially costly, option for urgent cash needs. This article aims to provide a clear understanding of what these loans entail, their potential benefits, and crucial considerations before committing.

The Financial Tightrope: When Every Dollar Counts

Living paycheck to paycheck is a reality for a significant portion of the working population. Despite careful budgeting and expense tracking, a single unexpected event can throw everything into disarray. The anxiety of not having enough money to cover immediate necessities is profound, potentially leading to late fees, utility shut-offs, or damage to credit scores if bills go unpaid.

Traditional lenders often have lengthy approval processes, strict credit requirements, and may not provide funds quickly enough for truly urgent situations. Borrowing from friends or family can be uncomfortable or simply not an option for everyone. Credit cards, while offering quick access to funds, can lead to spiraling debt if not managed carefully, especially given the typically high interest rates on cash advances.

For those seeking immediate funds based on their earned income, certain short-term loan options exist, but it’s vital to understand their full implications.

Understanding the Urgency: Why Traditional Options May Fall Short

When immediate cash is required, standard financial avenues often move too slowly or present significant barriers. Applying for a personal loan from a bank can take days or even weeks, involving extensive paperwork and a deep dive into credit history. A less-than-perfect credit score might lead to outright denial, leaving an applicant back at square one. High-interest credit card cash advances, while fast, come with immediate fees and often higher APRs than purchases, positioning them as an expensive last resort.

The emotional toll of searching for funds under pressure is immense. Many seek a clear, straightforward path to temporary relief. In such contexts, the specific structure of a payroll loan, leveraging consistent income for speed and accessibility, can be a consideration, though its costs demand careful evaluation.

Payroll Loans: A High-Cost, Short-Term Option

A payroll loan, often known by various names such as a payday loan or a short-term installment loan linked to your paycheck, is designed to provide rapid access to funds. It typically functions as an advance on upcoming wages, repaid on your next payday or over a short series of installments. Unlike traditional bank loans that rely heavily on your credit score, these loans often prioritize employment status and regular income as primary qualification criteria, making them accessible to those with a less-than-perfect credit history but a stable job.

For individuals facing an immediate financial shortfall, the speed of a payroll loan can be a significant factor. The application process is generally streamlined, often completed online within minutes, with funds potentially deposited into your account remarkably fast—sometimes within the same business day. This rapid turnaround time can address emergencies that simply cannot wait. However, it is crucial to understand that this speed and accessibility often come with significantly higher costs compared to conventional lending options, which must be carefully weighed against the urgency of the need.

Potential Advantages of a Payroll Loan for Specific Situations

When considering this type of financial product, you may find several distinct features relevant to urgent needs:

- Quick Approval and Funding: A primary characteristic is speed. Applications are typically processed rapidly, and if approved, funds can often be disbursed to your bank account very quickly, sometimes within hours.

- Less Stringent Credit Requirements: While a credit check may occur, the primary focus for approval often centers on employment stability and income, rather than solely on a perfect credit score. This can be a factor for individuals who have been turned down by traditional lenders.

- Direct and Structured Repayment: Repayment terms are usually tied to your pay schedule, often with automatic deductions from your bank account on your payday. While this simplifies the process, ensuring sufficient funds are available on the repayment date is critical.

- Bridging Short-Term Gaps: Payroll loans are designed specifically to cover short-term financial gaps, not long-term debt. They can provide temporary relief to get to your next paycheck, but should not be used for ongoing financial challenges.

Navigating the Landscape: Essential Considerations

While a payroll loan *might be a consideration* in an emergency, it’s crucial to approach it with extreme caution and careful consideration. Not all lenders are created equal, and understanding the terms and conditions is paramount to protecting your financial well-being. Being an informed borrower is essential to ensure this option, if chosen, truly helps rather than exacerbates your situation.

Always prioritize transparency. Seek out lenders who clearly disclose all fees, interest rates, and repayment schedules upfront. Pay close attention to the Annual Percentage Rate (APR), which reflects the true cost of borrowing over a year. For short-term loans, the APR can be exceptionally high, indicating a very expensive borrowing option. Be highly wary of hidden fees or ambiguous language in the loan agreement. You have a right to understand exactly what financial commitment you are making. Review reputable online resources like NerdWallet for guidance on smart borrowing practices and comparing financial products.

When to Consider a Payroll Loan (and When Not To)

A payroll loan should be considered only for genuine, acute, short-term financial emergencies where you have a clear, realistic plan for full repayment from your very next paycheck. Appropriate scenarios *might* include:

- An immediate, unexpected medical expense.

- An urgent car repair critically needed for employment.

- A sudden home repair that poses an immediate safety risk and cannot wait.

- Avoiding severe late fees on essential bills, provided your paycheck is imminent and can cover the full repayment.

It is critically important to understand that these loans are absolutely not designed for long-term financial problems, such as consolidating existing debt, funding discretionary purchases, or covering recurring expenses. Using a payroll loan repeatedly, or “rolling it over” (extending the repayment with additional fees), can quickly lead to a detrimental cycle of debt, making your financial situation significantly worse in the long run. If you frequently find yourself needing short-term loans, this is a strong signal to explore more comprehensive financial planning, budgeting strategies, and building an emergency fund.

Calculating Your Payroll Loan: Understanding the True Cost

Understanding the *total* cost of a payroll loan is absolutely essential before you commit. While you won’t need to perform complex mathematical formulas yourself, you must grasp the full amount you will repay. The core logic is straightforward: if you borrow a specific amount (the principal), you will repay that amount plus additional charges (typically interest and/or fees) over a set, usually short, period.

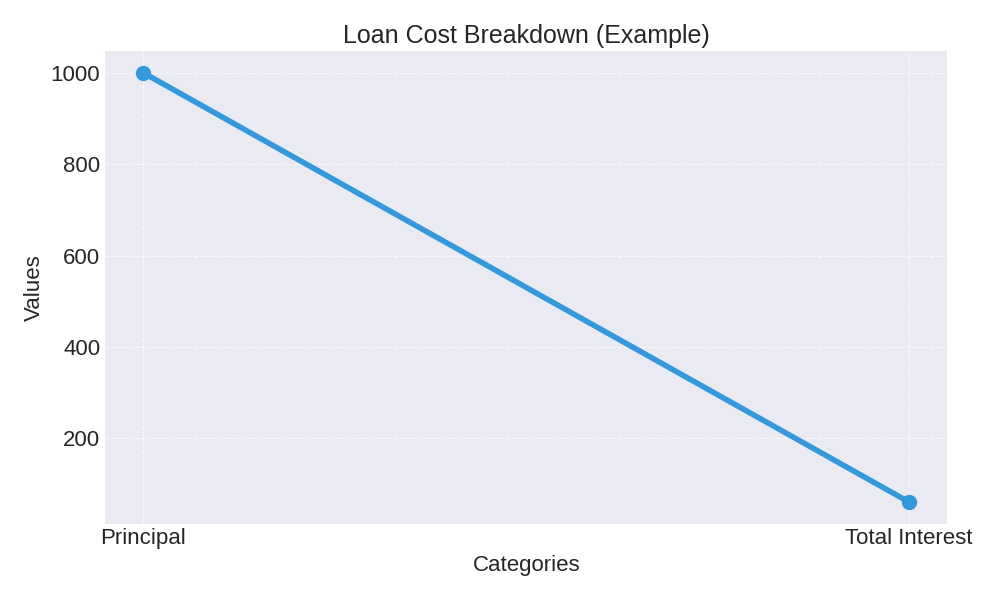

Let’s illustrate with an example for a short-term installment loan. Suppose you need to borrow $1,000 to cover an unexpected expense, and you plan to repay it over three months. With an APR of 50%, which, while high, is not uncommon for some shorter-term, less traditional loans, here’s how your repayment might look:

| Month | Monthly Payment | Remaining Balance |

|---|---|---|

| 1 | $353.60 | $688.07 |

| 2 | $353.60 | $363.14 |

| 3 | $353.60 | $0.00 (approx) |

In this scenario, for a $1,000 loan at 50% APR over three months, your total interest paid would be approximately $60.80, making the total repayment around $1,060.80. Understanding these numbers upfront is crucial to budgeting effectively and confirming you can genuinely afford the repayments without further financial strain. Always use a loan calculator provided by the lender, or consult directly with them, to get precise figures before signing any agreement. For more insights on understanding loan terms and interest rates, you can visit reputable resources like FederalReserve.gov.

Protecting Yourself: Smart Borrowing Practices and Alternatives

Even when faced with urgent financial needs, acting wisely is your strongest defense against potential financial pitfalls. Before committing to any payroll loan, *thoroughly* review the loan agreement. Pay meticulous attention to the total repayment amount, including all fees and interest, and confirm that there are no hidden charges or prepayment penalties if you wish to pay it off early. Ensure you fully understand the repayment schedule and exactly how payments will be collected.

A cardinal rule of short-term borrowing is to borrow only what you absolutely need and to have a clear, realistic plan for full repayment from your next available funds. Consider creating a temporary, stringent budget that explicitly accounts for the loan payment to ensure you do not overextend yourself further. Crucially, consider this experience an impetus to build or fortify an emergency fund. Even a small savings cushion can significantly mitigate the need for future high-cost urgent loans, providing true financial resilience for unexpected expenses. The goal should be to not just solve an immediate problem, but to fortify your financial future and avoid similar predicaments.

Conclusion: Navigating Urgent Gaps Responsibly

Facing an urgent financial need can be a daunting experience. While a payroll loan *may appear* as a rapid option, it is paramount to approach it with a clear understanding of its significant costs and risks. Such loans are highly specific financial products, offering fast access to funds based on consistent income, but they are designed for very short-term, acute emergencies only.

Responsible use involves borrowing only what is strictly necessary, having an immediate and reliable repayment plan, and thoroughly understanding all terms and conditions, especially the APR. Ultimately, while a payroll loan can provide a temporary bridge, the long-term solution lies in proactive financial planning, diligent budgeting, and building an emergency fund to create lasting financial security.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.