Are you feeling overwhelmed by multiple monthly payments, varied interest rates, and scattered due dates? A debt consolidation loan could be a powerful solution you’ve been searching for. This financial tool simplifies your debt repayment by combining several existing debts into one new loan. Utilizing a debt consolidation loan can offer a clear path to financial simplification, transforming a confusing array of bills into a single, manageable payment. Understanding how a debt consolidation loan works is the first step towards achieving financial clarity and potentially saving money over time.

What is a Debt Consolidation Loan?

A debt consolidation loan is a type of personal loan designed to roll multiple existing debts—such as credit card balances, medical bills, or other unsecured loans—into one new loan. Instead of making several payments to different creditors each month, you make a single, fixed payment to one lender. The goal is often to secure a lower overall interest rate, reduce your monthly payment, or simply streamline your finances. This approach can make managing your debt significantly easier and more predictable.

Benefits of a Debt Consolidation Loan

Consolidating your debts can provide several advantages, making your financial life less stressful and more organized. Exploring these benefits can help you decide if this strategy aligns with your financial goals.

- Simplified Payments: The most immediate benefit is having only one monthly payment instead of several. This reduces the chance of missing a payment and helps organize your finances.

- Potentially Lower Interest Rates: If you have high-interest debts like credit card balances, a consolidation loan can offer a lower overall interest rate. This could save you a significant amount of money over the life of the loan.

- Clear Path to Debt Freedom: With a fixed repayment schedule and a single payment, you can see a definite end date for your debt. This can provide motivation and a clearer understanding of your financial progress.

- Improved Credit Score (Indirectly): Successfully making consistent, on-time payments on a consolidation loan can positively impact your credit score over time. Reducing credit utilization by paying off revolving debts can also be beneficial.

- Reduced Stress: The mental burden of managing multiple debts can be immense. Consolidating can alleviate this stress, allowing you to focus on other financial goals.

Potential Drawbacks and Risks

While debt consolidation offers many benefits, it’s crucial to be aware of the potential downsides. Understanding these risks will help you make an informed decision and avoid common pitfalls.

- Longer Repayment Period: While monthly payments might be lower, extending the loan term can mean paying more interest over the total life of the loan, even with a lower interest rate.

- Fees and Charges: Some consolidation loans come with origination fees, closing costs, or prepayment penalties. Always read the fine print to understand all associated costs.

- Risk of Accumulating New Debt: If you consolidate and then continue to use your credit cards or take on new loans, you could end up in a worse financial situation than before.

- Impact on Credit Score: Applying for a new loan can result in a temporary dip in your credit score due to a hard inquiry. If you close old credit accounts after consolidation, it might also affect your credit utilization ratio or credit history length.

- Not a Universal Solution: Debt consolidation is not suitable for everyone. It requires discipline and a commitment to not accrue new debt.

Step-by-Step Guide to Getting a Debt Consolidation Loan

Navigating the process of obtaining a debt consolidation loan can seem daunting, but breaking it down into manageable steps makes it much clearer. Follow these steps to guide you through the process.

- Assess Your Debts: List all your current debts, including balances, interest rates, and minimum monthly payments. This will give you a clear picture of what you need to consolidate. Prioritize high-interest debts for the most impact.

- Check Your Credit Score: Your credit score significantly influences the interest rate you’ll be offered. A higher score typically qualifies you for better rates. Obtain your credit report from one of the three major credit bureaus.

- Research Lenders and Compare Offers: Look for banks, credit unions, and online lenders that offer debt consolidation loans. Compare interest rates, fees (like origination fees), repayment terms, and customer reviews. Don’t settle for the first offer you receive.

- Apply for the Loan: Once you’ve chosen a lender, complete their application. You’ll typically need to provide personal information, proof of income, and details about the debts you wish to consolidate.

- Receive Funds and Pay Off Old Debts: If approved, the funds from your new loan will either be disbursed to you directly or sent to your creditors on your behalf. Ensure all old accounts are fully paid off and closed if desired, to prevent future use.

- Make New, Consolidated Payments: Set up automatic payments for your new consolidation loan to ensure you never miss a due date. Stick to your budget and avoid taking on new debt to maintain financial stability.

How to Calculate Your Potential Savings

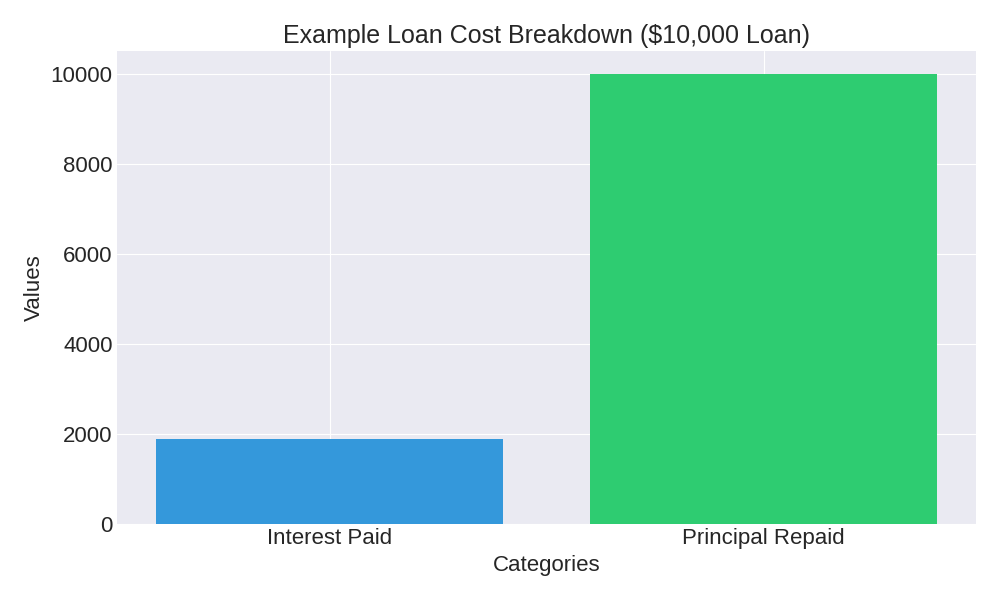

Understanding the financial impact of a debt consolidation loan doesn’t require complex mathematics. It’s about comparing your current total monthly payments and interest with what you’d pay on a new consolidated loan. If you borrow, for example, $10,000 at a 7% interest rate over a 5-year term, your monthly payment will be approximately $198. Over the entire loan period, the total interest paid would be around $1,880. This simplified calculation helps illustrate how a lower interest rate or extended term can affect your monthly outlay and overall cost.

| Year | Remaining Balance | Monthly Payment |

|---|---|---|

| 1 | $8,103 | $198 |

| 2 | $6,104 | $198 |

| 3 | $4,000 | $198 |

| 4 | $1,787 | $198 |

| 5 | $0 | $198 |

Monthly Payment Calculator

Alternatives to Debt Consolidation Loans

A debt consolidation loan is one of several strategies to manage and reduce debt. Depending on your financial situation and goals, other options might be more suitable. Consider these alternatives before making a decision.

- Balance Transfer Credit Cards: These cards offer a promotional 0% APR period on transferred balances for a set number of months. This can be effective if you can pay off the entire balance before the promotional period ends, but watch out for balance transfer fees and the high APR that kicks in afterward.

- Debt Management Plans (DMPs): Offered by non-profit credit counseling agencies, DMPs consolidate your unsecured debts into one monthly payment to the agency. They then distribute payments to your creditors, often negotiating lower interest rates and waiving fees. You can find accredited agencies via the Consumer Financial Protection Bureau.

- Home Equity Loans or HELOCs: If you own a home, you might use your home equity to secure a loan. These often have lower interest rates because they are secured by your home, but they put your home at risk if you fail to repay.

- Negotiating with Creditors: Sometimes, you can directly contact your creditors to negotiate lower interest rates, reduced monthly payments, or even a settlement for a lower total amount, especially if you’re experiencing financial hardship.

Frequently Asked Questions (FAQ)

Q: Who typically qualifies for a debt consolidation loan?

A: Qualification generally depends on your creditworthiness, income, and debt-to-income ratio. Lenders look for applicants with a good credit score (often 670 or higher), stable employment, and enough disposable income to comfortably make the new loan payments.

Q: Will a debt consolidation loan hurt my credit score?

A: Initially, applying for a new loan can cause a temporary dip due to a hard inquiry. However, if you use the loan to pay off high-interest revolving debt (like credit cards) and consistently make on-time payments, it can improve your credit score over the long term. Reducing your credit utilization ratio is a significant positive factor.

Q: What interest rate can I expect?

A: Interest rates vary widely based on your credit score, the loan term, and the lender. Applicants with excellent credit typically receive the lowest rates, while those with fair credit may face higher rates. It’s crucial to compare offers to find the most competitive rate available to you.

Q: Can I consolidate student loans with a personal debt consolidation loan?

A: Generally, private student loans can sometimes be consolidated with a personal debt consolidation loan, but federal student loans have specific protections and repayment options that may be lost if consolidated into a private personal loan. It’s important to weigh these factors carefully.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.