Are you feeling the pinch of high monthly car payments? Or perhaps you’ve improved your credit score since you first bought your vehicle? If so, vehicle loan refinancing could be your ticket to significant savings and more manageable finances. Refinancing your car loan means getting a new loan to pay off your existing one, often with better terms like a lower interest rate or a more favorable repayment period. This comprehensive guide will walk you through everything you need to know about vehicle loan refinancing, helping you slash payments and save money.

What is Vehicle Loan Refinancing?

Vehicle loan refinancing involves taking out a new loan to pay off your current auto loan. The primary goal is usually to secure a better deal than your original loan. This could mean a lower interest rate, a smaller monthly payment, or a different loan term (either shorter or longer). It’s a strategic financial move that can significantly impact your budget.

Think of it like this: if you originally took out a loan for your car at 7% interest and your credit has since improved, you might now qualify for a loan at 4% interest. Refinancing allows you to swap your old, more expensive loan for the new, cheaper one. The new lender pays off your old loan, and you then make payments to the new lender under the revised terms.

Why Refinance Your Vehicle Loan? Benefits You Can’t Ignore

Refinancing offers several compelling benefits that can improve your financial situation. Understanding these advantages can help you decide if it’s the right move for you.

Lower Monthly Payments

- Reducing your interest rate or extending your loan term can significantly lower your monthly payment. This frees up cash in your budget, making it easier to manage other expenses or save money.

Save Money on Interest

- A lower interest rate means you’ll pay less in total interest over the life of the loan. This can amount to hundreds, or even thousands, of dollars saved.

Change Loan Term

- Shorten Your Term: If you want to pay off your car faster and can afford higher monthly payments, a shorter loan term will save you a substantial amount in total interest.

- Extend Your Term: If you need to reduce your monthly expenses, extending the loan term can lower your payments. However, be aware that this might increase the total interest paid over the life of the loan.

Remove a Co-signer

- If you initially needed a co-signer due to your credit history, refinancing could allow you to remove them once your credit has improved, relieving them of their obligation.

Access to Cash (Cash-out Refinance)

- Some lenders offer “cash-out” refinancing, where you borrow more than you owe on the car and receive the difference in cash. This is typically used for other expenses but should be approached with caution as it increases your debt.

When is the Right Time for Vehicle Loan Refinancing?

Deciding when to refinance your car loan is crucial. Several factors can indicate an opportune moment.

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan, you’re likely to qualify for a better interest rate.

- Interest Rates Have Dropped: A general decline in market interest rates can make refinancing attractive, even if your credit hasn’t changed.

- You Have a High-Interest Rate: If your original loan came with a high APR, especially if you had less-than-perfect credit at the time, refinancing is often a wise choice.

- Financial Strain: If you’re struggling with your current monthly payment, extending the loan term through refinancing can provide immediate relief.

- Desire to Pay Off Faster: If your financial situation has improved, you might want to refinance into a shorter term to save on total interest.

It’s always a good idea to monitor market conditions and your credit health. For insights into current economic factors affecting interest rates, you can consult resources like the Federal Reserve’s official website.

Step-by-Step Guide to Easy Vehicle Loan Refinancing

Refinancing your car loan is a straightforward process when you know the steps involved.

Step 1: Check Your Credit Score

- Your credit score is the most significant factor determining your new interest rate. Access your credit report from the three major bureaus (Equifax, Experian, TransUnion) to understand your standing. You can get a free report annually from AnnualCreditReport.com. Aim for a score above 660 for competitive rates.

Step 2: Gather Necessary Documents

- Prepare documents such as your current loan statements, vehicle registration, driver’s license, proof of insurance, and income verification (pay stubs, tax returns).

Step 3: Shop Around for Lenders

- Don’t settle for the first offer. Check rates from various banks, credit unions, and online lenders. Each lender has different criteria and rates. Websites like Bankrate can help you compare options.

Step 4: Compare Loan Offers

- Look beyond just the interest rate. Compare the APR (Annual Percentage Rate, which includes fees), loan term, monthly payment, and any associated fees (e.g., application fees, prepayment penalties).

Step 5: Apply for the New Loan

- Once you’ve chosen the best offer, complete the loan application. This usually involves a hard credit inquiry, which might temporarily lower your score by a few points. However, multiple inquiries within a short period (typically 14-45 days) for the same type of loan are often treated as a single inquiry.

Step 6: Finalize and Pay Off Your Old Loan

- Upon approval, sign the new loan documents. The new lender will typically send funds directly to your old lender to pay off your original loan. Ensure you receive confirmation that your old loan has been fully satisfied.

How to Calculate Your Potential Savings

Understanding your potential savings is key to making an informed decision. While complex formulas can show precise figures, we’ll simplify it to show the impact on your monthly payments and total interest.

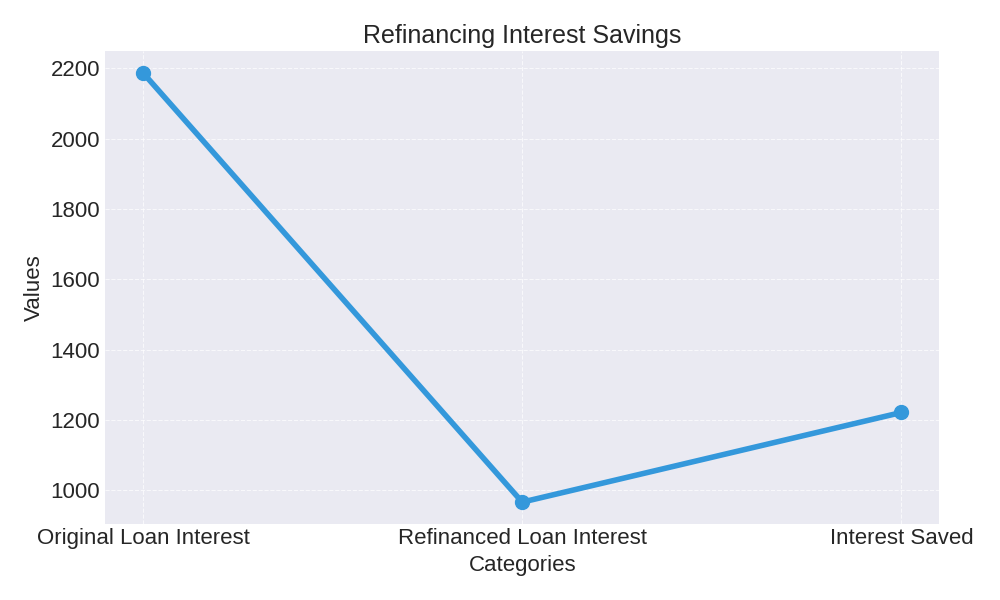

Consider this example: You have a remaining balance of $16,000 on your vehicle loan, with 3 years (36 months) left at an 8% APR. Your current monthly payment is approximately $501.37, and you would pay roughly $1,049 in interest over these remaining 36 months.

Now, imagine you refinance that $16,000 at a new, lower 4% APR over the same 3-year term. Your new monthly payment drops to approximately $471.29, and your total interest paid over the 36 months would be around $966. This simple calculation shows a monthly saving of about $30.08 and a total interest saving of roughly $83. That’s real money back in your pocket!

| Year | Balance (End of Year, Approx) | Monthly Payment (Refinanced) |

|---|---|---|

| 1 | ~$10,800 | $471.29 |

| 2 | ~$5,500 | $471.29 |

| 3 | $0 | $471.29 |

Monthly Payment Calculator

Potential Drawbacks and Things to Consider

While refinancing offers many benefits, it’s essential to be aware of potential downsides.

- Fees: Some lenders charge application fees, processing fees, or title transfer fees. These can eat into your savings, so factor them into your comparison.

- Extending Loan Term: While a longer term lowers monthly payments, it almost always increases the total interest paid over the life of the loan. You’ll be paying for your car for a longer period.

- Negative Equity: If you owe more on your car than it’s currently worth (negative equity), it might be harder to refinance. Lenders are often reluctant to lend more than the car’s value.

- Impact on Credit Score: A hard inquiry will temporarily ding your credit score. If you’re planning other major credit applications soon (like a mortgage), consider the timing.

Frequently Asked Questions (FAQ) About Vehicle Loan Refinancing

Q1: How often can I refinance my vehicle loan?

There’s no strict limit on how often you can refinance, but it only makes sense if you can secure better terms. Most people refinance once or twice during the life of a loan as their credit improves or rates drop.

Q2: Will refinancing hurt my credit score?

A hard credit inquiry for a new loan application will temporarily lower your credit score by a few points. However, if you get a lower interest rate and make timely payments, the long-term effect is usually positive as it demonstrates responsible credit management.

Q3: Can I refinance if I have bad credit?

It’s more challenging but not impossible. You might not get the lowest rates, but if your credit has improved even slightly since your original loan, you could still qualify for better terms. Consider working with a co-signer or exploring credit unions, which sometimes have more flexible criteria.

Q4: What if my car is old or has high mileage?

Lenders often have restrictions on vehicle age and mileage for refinancing. Typically, cars older than 7-10 years or with more than 100,000-125,000 miles might be harder to refinance, as their resale value decreases. However, specific policies vary by lender.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.