Navigating the world of homeownership can feel overwhelming, especially when considering the financial commitments involved. Exploring your mortgage options begins with a powerful tool: the mortgage loan calculator online. This digital utility empowers prospective homeowners, current mortgage holders, and real estate investors to accurately estimate potential loan payments, understand long-term costs, and make informed decisions. A reliable mortgage loan calculator online allows you to input specific loan details and quickly visualize how different variables impact your monthly budget and overall financial health. It’s an indispensable resource for anyone planning to finance a property, offering clarity and control over one of life’s most significant investments.

What is a Mortgage Loan Calculator and Why is it Essential?

A mortgage loan calculator is an online tool designed to estimate your monthly mortgage payments and the total cost of a loan over its lifetime. By inputting key financial data, you gain immediate insight into your potential financial obligations. This makes it an essential tool for several reasons. Firstly, it helps you budget effectively, allowing you to determine an convenient monthly payment before committing to a loan.

Secondly, a calculator facilitates comparison shopping between different lenders and loan products. You can quickly see how varying interest rates or loan terms affect your payments. Finally, it provides transparency, demystifying the complex calculations behind mortgage amortization and helping you understand how much of your payment goes towards principal versus interest over time.

Key Inputs for an Online Mortgage Calculator

To get accurate results from a mortgage loan calculator online, you’ll need to provide several pieces of information. Each input plays a crucial role in determining your estimated monthly payment and the total cost of the loan. Understanding these factors is the first step towards mastering your mortgage journey.

Loan Amount

This is the total sum of money you intend to borrow for your home purchase. It’s typically the purchase price of the home minus your down payment. A higher loan amount will naturally result in higher monthly payments and potentially more interest paid over the loan’s term.

Interest Rate

The interest rate is the percentage charged by the lender for borrowing the money. It’s one of the most significant factors influencing your monthly payment and the total cost of your mortgage. Even a small difference in the interest rate can lead to substantial savings or additional costs over decades. This rate is usually expressed as an annual percentage.

Loan Term

The loan term refers to the length of time you have to repay the loan, commonly 15, 20, or 30 years for conventional mortgages. A shorter loan term typically means higher monthly payments but less interest paid overall, as you’re paying off the principal faster. Conversely, a longer term offers lower monthly payments but accrues more interest over time.

Down Payment

This is the upfront cash payment you make towards the purchase of a home. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly mortgage payments and the total interest you’ll pay. It can also help you secure a lower interest rate and avoid Private Mortgage Insurance (PMI).

Property Taxes & Homeowner’s Insurance (Escrow)

Most mortgage payments include an escrow component for property taxes and homeowner’s insurance. These are not part of the principal and interest calculation but are crucial for determining your total monthly housing cost. Lenders typically collect these funds monthly and pay them on your behalf when due.

Other Costs (PMI, HOA fees)

Depending on your loan-to-value (LTV) ratio (if your down payment is less than 20%), you might need to pay Private Mortgage Insurance (PMI). Additionally, properties in certain communities or condominiums may require Homeowners Association (HOA) fees. While not always directly included in the lender’s basic calculation, these are vital to factor into your overall housing budget.

Step-by-Step Guide: How to Use a Mortgage Loan Calculator Online

Using an online calculator is straightforward, but knowing what to input and what to look for in the results will help you maximize its benefits. Follow these steps to effectively explore your mortgage options:

- Gather Your Data: Before you start, have a clear idea of your desired loan amount (purchase price minus potential down payment), your estimated interest rate, and the loan term you’re considering. Don’t forget any anticipated property taxes, homeowner’s insurance, or HOA fees.

- Enter the Loan Amount: Input the total amount you plan to borrow. If you haven’t determined your down payment yet, you can experiment with different loan amounts.

- Specify the Interest Rate: Enter the annual interest rate offered by lenders. This rate can fluctuate based on market conditions and your creditworthiness, so use a realistic estimate.

- Select the Loan Term: Choose your preferred repayment period, such as 15 or 30 years. Observe how changing this factor impacts your monthly payment.

- Add Down Payment (Optional but Recommended): If the calculator has a separate field for a down payment, enter it. Otherwise, calculate your loan amount after subtracting the down payment.

- Include Taxes, Insurance, and Other Fees: Many advanced calculators allow you to input estimated annual property taxes, homeowner’s insurance premiums, and even PMI or HOA fees. This provides a more comprehensive monthly payment estimate.

- Calculate and Review Results: Once all data is entered, click the “Calculate” button. The calculator will instantly display your estimated monthly mortgage payment, typically broken down by principal and interest, and often total interest over the loan’s life.

Let’s illustrate with a simple example:

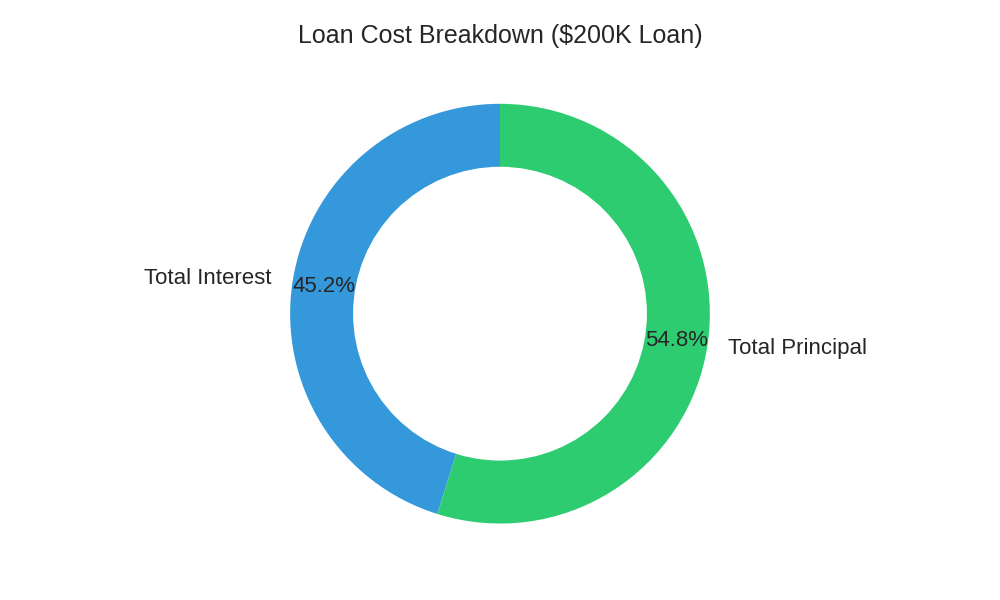

If you borrow $200,000 at a 4.5% annual interest rate over a 30-year term, your estimated monthly payment for principal and interest would be approximately $1,013.37. Over the life of the loan, you would pay significantly more than the initial $200,000 borrowed due to accumulated interest.

| Metric | Value |

|---|---|

| Estimated Monthly Payment (P&I) | $1,013.37 |

| Total Interest Paid Over Loan Term | $164,813.20 |

| Total Amount Repaid (Principal + Interest) | $364,813.20 |

Monthly Payment Calculator

Understanding the Results: What Do the Numbers Mean?

Interpreting the output of a mortgage calculator is crucial for making informed financial decisions. The numbers represent more than just figures; they reflect your long-term financial commitment.

Monthly Principal & Interest Payment

This is the core of your mortgage payment. The principal portion reduces the actual loan balance, while the interest portion is the cost of borrowing money. In the early years of a loan, a larger portion of your payment goes towards interest; as the loan matures, more goes towards principal.

Total Interest Paid

This figure shows the cumulative interest you will pay over the entire loan term. It highlights how much extra you pay beyond the original loan amount. This total can be significantly reduced by finding lower interest rates or making extra payments.

Amortization Schedule

Many calculators provide an amortization schedule, which is a table showing each payment made over the loan’s life, detailing how much goes to principal and interest for each payment, and the remaining balance. This schedule demonstrates how slowly the principal balance decreases in the early years and accelerates later on.

Impact of Down Payment

A larger down payment directly reduces the loan amount, leading to lower monthly payments and less total interest paid. It also signals financial stability to lenders, potentially resulting in more favorable interest rates.

The Power of Extra Payments

Experimenting with adding extra principal to your monthly payment in the calculator can reveal significant savings. Even small additional amounts can shave years off your loan term and save tens of thousands in interest. This strategy helps you build equity faster.

Advanced Strategies and Considerations

Beyond basic calculations, a mortgage loan calculator can help you explore more sophisticated financial strategies related to homeownership.

Fixed-Rate vs. Adjustable-Rate Mortgages

A fixed-rate mortgage offers a consistent interest rate and monthly payment for the entire loan term, providing stability and predictability. An adjustable-rate mortgage (ARM), however, has an interest rate that can change periodically after an initial fixed period, potentially leading to fluctuating monthly payments. Use the calculator to compare potential scenarios under different rate assumptions.

Refinancing Options

If interest rates drop or your financial situation improves, refinancing your mortgage could save you money. A calculator can help you compare your current loan’s terms against potential new terms, showing the savings from a lower rate or a shorter term. Always consider closing costs when evaluating refinancing benefits. Learn more about understanding closing costs from the Consumer Financial Protection Bureau.

Understanding APR vs. Interest Rate

The interest rate is simply the cost of borrowing the principal. The Annual Percentage Rate (APR), however, represents the total cost of the loan, including the interest rate plus certain fees and charges like origination fees or points. When comparing loans, the APR often provides a more comprehensive picture of the true cost. Comparing APRs is crucial for an “apples-to-apples” comparison between different lenders. For more insights on this, consult reputable financial resources.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.