Life can throw unexpected curveballs, leaving you in a financial tight spot. Perhaps an emergency medical bill, urgent car repair, or a sudden home expense has landed on your lap, and you’re looking for a solution. The challenge? Your credit score isn’t where you’d like it to be. You might feel like you’re stuck, wondering if securing a personal loan for bad credit is even possible. You’re not alone in this feeling of frustration or helplessness.

Many people find themselves in a similar situation, navigating the complexities of their financial history while trying to secure necessary funds. The good news is that having a less-than-perfect credit score doesn’t automatically close every door. While it might be more challenging, and the terms might be different, there are legitimate pathways to get a personal loan for bad credit that can help you bridge the gap. This article will guide you through understanding your options, what to look out for, and how to improve your chances, even when your credit isn’t stellar.

Understanding Your Situation: The Bad Credit Hurdle

When lenders assess your application for a personal loan, your credit score is a primary indicator of your financial reliability. A low credit score signals to lenders that you might carry a higher risk of defaulting on payments. This isn’t a judgment on you as a person, but rather a statistical assessment based on your past borrowing behavior. You might feel rejected or disheartened when you see higher interest rates or outright denials from traditional banks.

However, this doesn’t mean you’re out of options. It simply means you need to approach the lending market differently. Understanding why your credit score is low, such as late payments, high credit utilization, or collections, can help you explain your situation to lenders and take steps to improve it moving forward. Remember, every financial journey has its ups and downs, and focusing on solutions is key.

Strategies for Securing a Personal Loan with Bad Credit

Navigating the lending landscape with bad credit requires a strategic approach. You’ll need to be proactive and explore alternatives to conventional bank loans. The goal is to find a lender willing to take on the perceived risk, often in exchange for a higher interest rate or additional security. Here are several effective strategies you can employ.

Explore Bad Credit Personal Loan Lenders

- Online Lenders: Many online platforms specialize in offering personal loans for bad credit. These lenders often have more flexible underwriting criteria than traditional banks. They might look beyond just your credit score, considering factors like your income, employment history, and debt-to-income ratio.

- Credit Unions: If you’re a member of a credit union, or eligible to join one, they can be an excellent resource. Credit unions are member-owned and often more willing to work with individuals who have lower credit scores, offering more favorable rates and terms than for-profit lenders.

- P2P (Peer-to-Peer) Lenders: These platforms connect borrowers directly with individual investors. While still credit-score-sensitive, some investors might be more lenient or willing to take on higher-risk loans with higher interest rates.

Consider a Co-signer

If you have a friend or family member with excellent credit who trusts you implicitly, asking them to co-sign your loan could significantly improve your chances. A co-signer essentially agrees to take responsibility for the loan if you fail to make payments. This reduces the lender’s risk, often leading to better interest rates and approval. However, this is a significant commitment for the co-signer, as their credit will also be impacted if you default.

Offer Collateral (Secured Loans)

Unlike an unsecured personal loan that relies solely on your creditworthiness, a secured personal loan requires you to put up an asset as collateral. This could be a car, savings account, or certificate of deposit (CD). If you fail to repay the loan, the lender can seize the collateral. While this carries a higher risk for you, it dramatically reduces the risk for the lender, making them more likely to approve your application and potentially offer a lower interest rate than an unsecured bad credit personal loan.

Start Small and Build

Sometimes, the best strategy is to start with a smaller loan to prove your reliability. Some lenders offer “credit builder” loans specifically designed to help you improve your credit score. These loans are usually for small amounts and require consistent, on-time payments, which are then reported to credit bureaus, gradually boosting your score over time. You can also explore secured credit cards as another tool for credit building.

What Lenders Look For (Even with Bad Credit)

Even when your credit score isn’t ideal, lenders aren’t just looking at a single number. They assess your overall financial picture to determine your ability to repay the loan. Understanding these factors can help you present a stronger application and highlight your strengths.

- Stable Income and Employment: Lenders want to see consistent income that demonstrates your ability to make regular payments. A steady job history, especially for several years, is a strong positive indicator.

- Debt-to-Income Ratio (DTI): This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to cover new loan payments, making you a less risky borrower.

- Existing Debts: While your credit score reflects existing debts, lenders will also look at the specifics – how many accounts you have open, their balances, and your payment history on them. Demonstrating a downward trend in other debts can be beneficial.

- Saving Habits: If you can show a history of saving money, even small amounts, it suggests financial responsibility and discipline, which can be a favorable sign for lenders.

The Application Process: Navigating the Details

Once you’ve identified potential lenders, the application process for a bad credit personal loan begins. This stage requires careful attention to detail and a commitment to transparency. Being prepared can save you time and increase your chances of approval.

Gather Your Documents

Before applying, collect all necessary documentation. This typically includes government-issued ID, proof of income (pay stubs, tax returns), bank statements, and potentially utility bills to prove residency. Having these ready will streamline the application process and show your readiness.

Be Honest and Transparent

Always provide accurate information on your application. Attempting to hide or misrepresent your financial situation can lead to immediate denial and potentially serious legal repercussions. Lenders appreciate honesty and often have sophisticated ways of verifying information. If there are valid reasons for your bad credit, be prepared to explain them clearly and concisely.

Understand the Loan Terms

Before signing any agreement, meticulously review the loan terms. Pay close attention to the Annual Percentage Rate (APR), which includes the interest rate and any fees, the loan term, and the total cost of the loan. Don’t hesitate to ask questions if anything is unclear. High APRs are common with bad credit loans, so ensure the payments are affordable within your budget.

Avoid Predatory Lenders

Be wary of lenders who guarantee approval, charge exorbitant upfront fees, or pressure you into signing immediately. These can be red flags for predatory lending practices, which can trap you in a cycle of debt. Always research a lender’s reputation and read reviews before committing. For more information on protecting yourself, visit the Consumer Financial Protection Bureau website.

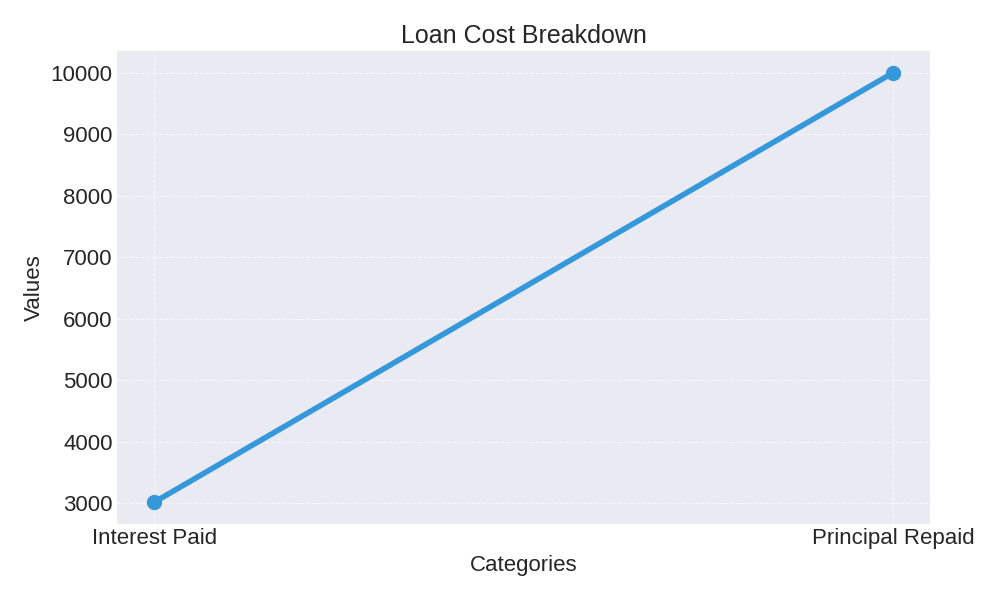

Understanding Loan Costs: A Practical Example

When you take out a personal loan, you’re not just repaying the principal amount you borrowed; you’re also paying interest. The interest is essentially the cost of borrowing money. With bad credit, interest rates are typically higher to compensate lenders for the increased risk. Let’s look at a practical example to understand how this impacts your monthly payment and the total cost of your loan.

Imagine you borrow $10,000 at an Annual Percentage Rate (APR) of 18% over a loan term of 3 years (36 months). If you make consistent, on-time payments, you will pay approximately $361.52 each month. Over the entire 3-year period, your total payments will amount to $13,014.72. This means you will pay $3,014.72 in interest on top of the original $10,000 you borrowed. Understanding these figures upfront is crucial for managing your budget.

| Year | Remaining Principal (End of Year) | Monthly Payment |

|---|---|---|

| 1 | $7,301.69 | $361.52 |

| 2 | $3,989.14 | $361.52 |

| 3 | $0.00 | $361.52 |

Monthly Payment Calculator

Beyond the Loan: Rebuilding Your Financial Health

Securing a personal loan with bad credit isn’t just about getting the money you need; it’s also an opportunity to start rebuilding your financial standing. By demonstrating responsible borrowing behavior, you can gradually improve your credit score, opening up better financial opportunities in the future.

-

- Pay on Time, Every Time: This is arguably the most crucial step. Timely payments on your new loan will be reported to credit bureaus and significantly boost your payment history, the largest factor in your credit score. Set up automatic payments to avoid missing due dates.

- Reduce Other Debts: As you manage your personal loan, also focus on reducing other outstanding debts, such as credit cards or overdue accounts. Lowering your overall debt balance improves your credit utilization ratio, which positively affects your credit score. Create a realistic budget to manage expenses and avoid taking on new unnecessary debt. Monitoring your credit report regularly can help you track progress and identify any errors early. Over time, consistent financial discipline can restore lender confidence and strengthen your long-term financial health.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.