Your home isn’t just a place to live; it’s a significant financial asset that can grow in value over time. As you pay down your mortgage and your property appreciates, you build what is known as home equity. This equity represents the portion of your home that you truly own, free and clear of mortgage debt. Tapping into this potential wealth through a loan from house equity can provide access to funds for various purposes, from home renovations to debt consolidation or even unexpected emergencies.

Understanding how a loan from house equity works, its different forms, and the responsibilities involved is crucial. This comprehensive guide aims to walk you through everything you need to know, helping you make informed financial decisions about leveraging your most valuable asset.

What Exactly is Home Equity?

Home equity is the difference between your home’s current market value and the outstanding balance on your mortgage(s). It’s essentially the stake you have in your property. For example, if your home is valued at $400,000 and you owe $250,000 on your mortgage, you have $150,000 in home equity.

Equity builds in two primary ways. Firstly, each mortgage payment you make contributes to reducing your principal balance, directly increasing your equity. Secondly, if your home’s market value increases due to appreciation, your equity grows without you having to do anything. The more equity you have, the more financial flexibility you may gain.

Types of Loans from House Equity

When considering a loan from house equity, you generally have three main options, each with distinct features:

1. Home Equity Loan (HEL)

A Home Equity Loan, often called a “second mortgage,” provides a lump sum of cash upfront. It functions much like your original mortgage but is separate from it.

- Fixed Interest Rate: The interest rate is typically fixed for the life of the loan, meaning your monthly payments remain consistent.

- Fixed Repayment Term: You repay the loan over a set period, usually 5 to 30 years, with predictable installment payments.

- Best For: Borrowers who need a specific amount of money for a one-time expense and prefer stable, predictable payments.

2. Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit that allows you to borrow money as needed, up to a pre-approved limit. It’s similar to a credit card but secured by your home.

- Variable Interest Rate: HELOCs typically have variable interest rates, which can fluctuate with market conditions, impacting your monthly payments.

- Draw Period: During this initial period (usually 5-10 years), you can borrow and repay funds as often as you like, often making interest-only payments.

- Repayment Period: After the draw period, you enter the repayment period (typically 10-20 years), where you make principal and interest payments on the outstanding balance.

- Best For: Borrowers needing ongoing access to funds for irregular expenses, such as multi-stage renovations or tuition payments.

3. Cash-Out Refinance

A cash-out refinance involves replacing your existing mortgage with a new, larger mortgage. The difference between your old mortgage balance and the new, larger loan is paid to you in cash.

- New Mortgage Terms: You get new interest rates and a new repayment schedule for your entire mortgage.

- Potential Lower Interest Rates: Often offers lower interest rates than HELs or HELOCs because it’s a first mortgage, though this depends on market conditions.

- Best For: Borrowers looking to consolidate debt into a single, potentially lower-interest loan or those who prefer to have one mortgage payment.

How to Qualify for a Loan from House Equity: Step-by-Step Guide

Qualifying for a home equity product involves several factors. Lenders assess your financial health and the equity in your home.

- Assess Your Home Equity:

- Determine your home’s current market value (e.g., via online estimates or a professional appraisal).

- Subtract your outstanding mortgage balance(s).

- Lenders typically allow you to borrow up to 80-90% of your home’s equity, so calculate your usable equity.

- Check Your Credit Score:

- A strong credit score (generally 680 or higher) is crucial for securing favorable interest rates and approval.

- Lenders view higher scores as an indicator of responsible borrowing.

- Evaluate Your Debt-to-Income (DTI) Ratio:

- Your DTI is the percentage of your gross monthly income that goes towards debt payments.

- Lenders usually prefer a DTI ratio below 43%, though some may approve higher. This helps ensure you can handle additional payments.

- Verify Stable Income and Employment:

- You’ll need to demonstrate a consistent income source and stable employment history.

- Lenders want assurance that you can reliably make your loan payments.

- Undergo a Home Appraisal:

- The lender will typically require a professional appraisal to confirm your home’s market value. This is a critical step in determining your available equity.

The Loan Application Process: What to Expect

Once you’ve determined your potential eligibility, the application process for a home equity product generally follows these steps:

- Research and Compare Lenders:

- Shop around with multiple banks, credit unions, and online lenders.

- Compare interest rates, fees, repayment terms, and customer service. Sites like the Consumer Financial Protection Bureau (CFPB) offer resources for comparing financial products.

- Gather Required Documents:

- You’ll typically need proof of income (pay stubs, tax returns), bank statements, identification, and details of your current mortgage.

- Submit Your Application:

- Complete the lender’s application form, providing accurate financial and personal information.

- Underwriting and Appraisal:

- The lender will review your application, order a home appraisal, and verify your financial information. This stage assesses the risk of the loan.

- Loan Approval and Closing:

- If approved, you’ll receive a loan offer with terms and conditions.

- Carefully review all documents, ask questions, and attend the closing to finalize the loan agreement.

Understanding Costs and Repayments

Before committing to a loan from house equity, it’s vital to understand the financial implications beyond the principal amount.

- Interest Rates: These can be fixed (for HELs), offering predictable payments, or variable (for HELOCs), which can change over time. Variable rates are often tied to an index like the Prime Rate, as tracked by resources such as the Federal Reserve.

- Closing Costs: These are fees paid at the time of loan closing, which can include appraisal fees, origination fees, title insurance, and attorney fees. They typically range from 2% to 5% of the loan amount.

- Prepayment Penalties: Some lenders may charge a fee if you pay off your loan early, so always check for this clause.

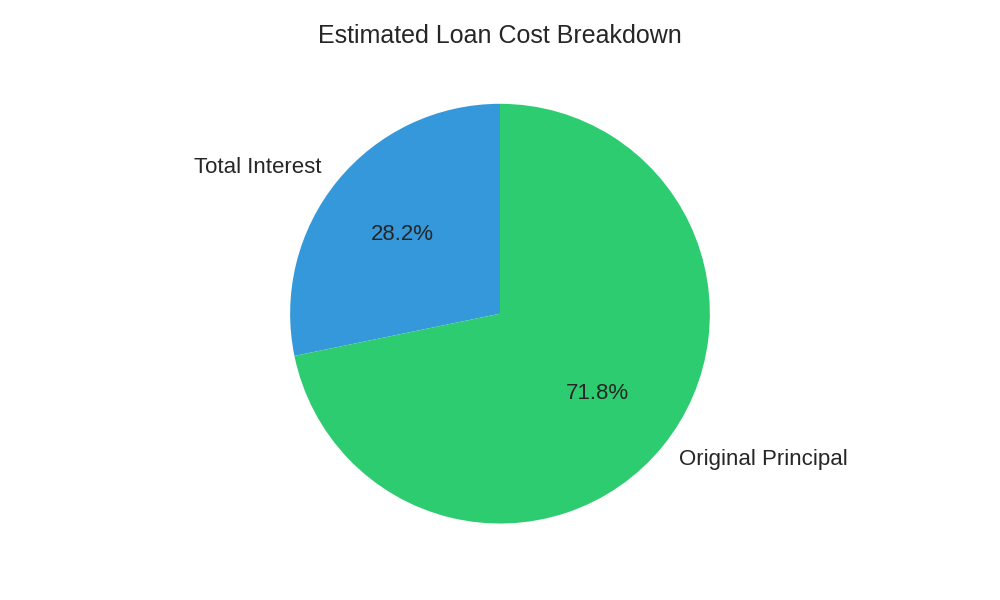

Example Repayment Schedule

To illustrate the repayment structure, let’s consider an example:

If you secure a loan from house equity of $50,000 at a 7% annual interest rate over a 10-year (120-month) term, your estimated monthly payment would be approximately $580.54. Over the life of the loan, you would pay back a total of $69,664.80, which includes $19,664.80 in interest.

| Year | Beginning Principal Balance | Monthly Payment |

|---|---|---|

| 1 | $50,000.00 | $580.54 |

| 2 | $46,536.24 | $580.54 |

| 3 | $42,836.00 | $580.54 |

| 4 | $38,881.01 | $580.54 |

| 5 | $34,652.79 | $580.54 |

| 6 | $30,132.84 | $580.54 |

| 7 | $25,302.50 | $580.54 |

| 8 | $20,142.92 | $580.54 |

| 9 | $14,635.09 | $580.54 |

| 10 | $8,760.72 | $580.54 |

Monthly Payment Calculator

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.