You’ve been there: the gut-wrenching feeling of applying for a credit card, only to be met with a “regrettably, we cannot approve your application” letter. It’s frustrating, demoralizing, and feels like a vicious cycle. How are you supposed to build credit if no one will give you a chance? If this sounds familiar, you’re not alone. Many individuals find themselves in a similar predicament, searching for a credit card for the worst credit. The good news is, options exist, and a path to financial recovery is within reach. This article aims to guide you through understanding these options and offers strategies for moving towards approval, even if your credit history feels like a dead end.

Securing a credit card for the worst credit isn’t about finding a magic bullet; it’s about understanding the tools available and using them strategically. It requires patience, discipline, and a willingness to take measured steps towards rebuilding your financial reputation. We’ll explore practical solutions that can help you turn the tide, moving you from credit despair to credit empowerment.

Understanding Your Credit Situation: Beyond Just a Score

Before diving into solutions, it’s crucial to acknowledge the reality of your credit situation. Your credit score, typically a FICO or VantageScore, is a three-digit number summarizing your creditworthiness. A score below 580 generally falls into the “very poor” or “bad” category. This often means you have a history of missed payments, bankruptcies, collections, or high credit utilization. Lenders view these factors as significant risks.

The pain points are clear:

- Rejection Fatigue: Repeated denials can make you feel hopeless and unwilling to even try.

- High Costs: Even if approved, cards for bad credit often come with higher interest rates and fees.

- Limited Access: Without a credit card, everyday tasks like renting a car or booking a hotel can be challenging.

- Trapped in the Cycle: It’s hard to improve your credit if you can’t get credit in the first place.

But remember, your credit history isn’t a life sentence. It’s a record that can be improved with consistent, positive financial actions.

Your First Step: Check Your Credit Report

You can’t fix what you don’t understand. Your absolute first step should be to obtain and review your credit reports from all three major bureaus (Equifax, Experian, and TransUnion). You are entitled to a free report from each bureau annually. This is vital for identifying any errors and understanding the true scope of your credit challenges. For a reliable source, you can visit AnnualCreditReport.com to get your free reports.

The Best Options for a Credit Card for the Worst Credit

When traditional credit cards are out of reach, specialized products are designed to help you rebuild. These aren’t always glamorous, but they are effective.

1. Secured Credit Cards: Your Most Viable Option

A secured credit card is often the best pathway for someone seeking a credit card for the worst credit. Here’s how it works:

- Security Deposit: You provide a cash deposit to the issuer, which typically becomes your credit limit. For example, a $200 deposit gives you a $200 credit limit. This deposit minimizes the lender’s risk.

- Credit Reporting: The card functions much like a regular credit card. You make purchases, receive a statement, and make payments. Crucially, your payment activity is reported to the major credit bureaus.

- Rebuilding Potential: By consistently making on-time payments and keeping your balance low, you demonstrate responsible credit behavior, which gradually improves your credit score.

- Refundable Deposit: Once your credit improves, you may be able to upgrade to an unsecured card, and your deposit is returned to you.

What to look for in a secured card:

- Reports to all three bureaus: Essential for broad credit improvement.

- Low annual fee: Some secured cards charge fees, others don’t. Aim for a low fee or none at all.

- Clear path to unsecured: Does the issuer offer a review after a certain period (e.g., 7-12 months) to transition to an unsecured card?

- Reasonable APR: While you should aim to pay your balance in full, a lower APR is always better in case you carry a balance.

2. Credit Builder Loans: An Indirect Approach

While not a credit card, a credit builder loan is an excellent tool for demonstrating repayment ability. With this type of loan, the money you “borrow” is held in a savings account or CD, and you make monthly payments. Once the loan is paid off, you receive the money. Like secured cards, your payments are reported to credit bureaus. It’s a forced savings mechanism that simultaneously builds your credit history.

3. Authorized User Status: Riding on Someone Else’s Good Credit

If you have a trusted friend or family member with excellent credit, they might add you as an authorized user on one of their credit cards. This can potentially add their positive payment history to your credit report. However, this relies on their responsible use and their willingness to help. Ensure they understand the implications and that you both have clear communication about usage and payments.

4. Prepaid Cards: Not a Credit Builder, but a Budget Tool

It’s important to distinguish prepaid cards from credit cards. Prepaid cards require you to load money onto them before use; they don’t offer a line of credit and typically do not report to credit bureaus. While useful for budgeting or online shopping, they won’t help you build credit.

Strategizing Your Credit Rebuilding Journey

Getting a credit card is just the beginning. The real work is in how you use it. Here’s a roadmap for success:

- Pay on Time, Every Time: This is the single most important factor in your credit score (35%). Set up automatic payments to avoid missing due dates.

- Keep Utilization Low: Aim to use less than 30% (ideally under 10%) of your available credit limit. For a $200 secured card, that means keeping your balance under $60. High utilization signals risk to lenders.

- Don’t Close Old Accounts (Eventually): Older accounts with good payment history contribute positively to your credit age.

- Monitor Your Reports: Regularly check your credit reports for accuracy and progress. You can learn more about managing your credit at the Consumer Financial Protection Bureau (CFPB).

- Be Patient: Credit building is a marathon, not a sprint. Positive changes take time, often 6-12 months to see significant improvement.

Understanding the Costs: A Repayment Example

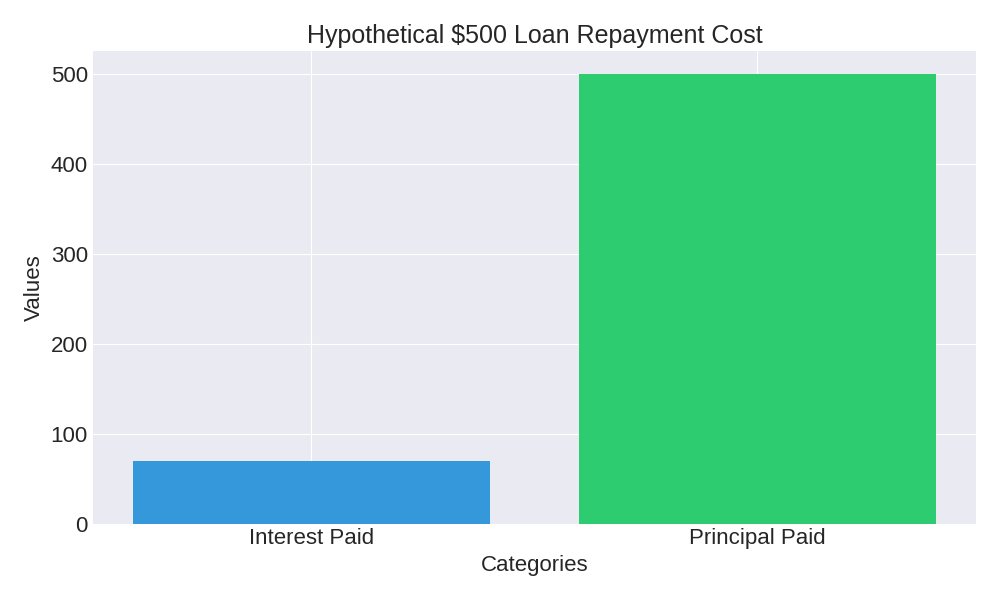

While secured cards are about building credit, it’s crucial to understand the cost if you carry a balance on any credit card. Cards for individuals with poor credit often come with higher Annual Percentage Rates (APRs). Let’s illustrate with a hypothetical scenario:

Imagine you have a small balance of $500 on your credit card and an APR of 25%. If you decide to pay this balance off with a fixed payment over 12 months, here’s how it might look. This example shows that even a small balance can accrue significant interest if not paid off quickly.

If you borrow $500 at 25% interest and make a consistent monthly payment of $47.51, you will pay off the loan in approximately 12 months, incurring around $70.12 in total interest.

| Month | Starting Balance | Monthly Payment |

|---|---|---|

| 1 | $500.00 | $47.51 |

| 2 | $462.91 | $47.51 |

| 3 | $425.04 | $47.51 |

| 4 | $386.36 | $47.51 |

| 5 | $346.86 | $47.51 |

| 6 | $306.51 | $47.51 |

| 7 | $265.30 | $47.51 |

| 8 | $223.21 | $47.51 |

| 9 | $180.22 | $47.51 |

| 10 | $136.31 | $47.51 |

| 11 | $91.46 | $47.51 |

| 12 | $45.65 | $47.51 |

| Total Interest Paid: | $70.12 |

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.