Investing in Certificates of Deposit (CDs) can be a cornerstone of a well-rounded financial strategy, especially for those prioritizing safety and predictable returns. If you’re looking for a low-risk way to grow your savings, understanding whether investing in CDs aligns with your financial aspirations is crucial. This comprehensive guide will break down everything you need to know about CDs, helping you decide if they are the right fit for your money goals.

What Are Certificates of Deposit (CDs)?

A Certificate of Deposit (CD) is a type of savings account that holds a fixed amount of money for a fixed period of time, and in return, the issuing bank pays interest. Unlike a regular savings account, you typically can’t withdraw the money from a CD without penalty until the term ends, also known as the maturity date. This commitment is what allows banks to offer higher interest rates compared to standard savings accounts.

CDs are often considered a conservative investment option due to their stability. They are insured by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000 per depositor, per insured bank, per ownership category. This makes them an extremely secure choice for protecting your principal while earning interest.

Types of CDs: More Than Just Fixed Rates

While the basic premise of a CD is simple, there are several variations designed to meet different financial needs and preferences.

- Standard CDs: These are the most common type, offering a fixed interest rate for a specific term (e.g., 6 months, 1 year, 5 years). You commit your funds for the entire term and earn a guaranteed return.

- Jumbo CDs: These require a significantly larger minimum deposit, often $100,000 or more. In exchange for the higher deposit, they typically offer slightly better interest rates than standard CDs.

- Callable CDs: With callable CDs, the issuing bank has the option to “call” or redeem the CD before its maturity date, usually if interest rates fall. This can introduce some reinvestment risk for the investor.

- Brokered CDs: These CDs are offered by brokerage firms rather than directly by banks. They can provide access to a wider range of CD terms and rates from various banks, potentially offering more flexibility.

- No-Penalty CDs (Liquid CDs): These allow you to withdraw your money before the maturity date without incurring an early withdrawal penalty, though they usually offer slightly lower interest rates than standard CDs.

- Step-Up and Bump-Up CDs: Step-up CDs have interest rates that increase at predetermined intervals during the term. Bump-up CDs give you the option to request a rate increase if the bank’s rates for new CDs go up during your term.

The Benefits of Investing in CDs

For many investors, especially those with a lower risk tolerance or specific short-to-medium-term goals, CDs offer compelling advantages.

- Safety and Security: As mentioned, CDs from FDIC-insured institutions are backed by the full faith and credit of the U.S. government, up to the insurance limits. This means your principal is protected even if the bank fails.

- Predictable Returns: With a fixed interest rate, you know exactly how much interest you will earn over the CD’s term. This makes them excellent for budgeting and planning for future expenses.

- No Market Volatility: Unlike stocks or mutual funds, CDs are not subject to market fluctuations. Their value does not go up or down based on economic news or stock market performance.

- Versatility for Goals: CDs can be ideal for saving for specific financial goals within a defined timeframe, such as a down payment on a house, a child’s college fund, or a future vacation.

- Higher Rates than Savings Accounts: Generally, CDs offer better interest rates than traditional savings accounts because you agree to lock up your money for a set period.

Potential Downsides and Risks

While CDs are safe, they are not without certain limitations that investors should consider.

- Lower Returns Compared to Other Investments: CDs typically offer lower returns than riskier assets like stocks over the long term. They may not keep pace with inflation, especially during periods of high inflation.

- Illiquidity: Your money is generally locked in for the CD’s term. Early withdrawals usually incur a penalty, which could be several months’ worth of interest.

- Reinvestment Risk: When a CD matures, interest rates might be lower than when you first invested. This means you might have to reinvest at a less favorable rate.

- Interest Rate Risk (for Callable CDs): If you have a callable CD and interest rates drop, the bank might call your CD, forcing you to reinvest your funds at a lower rate.

How to Calculate Your CD Earnings

Calculating how much you’ll earn on a CD typically involves simple interest, especially for shorter terms or if interest is not compounded frequently. Most banks calculate interest on a daily basis and compound it monthly, quarterly, or annually. However, for a basic understanding, you can estimate using simple interest over the term.

Here’s how to calculate the simple interest earned on a CD:

- Determine your Principal: This is the initial amount you deposit into the CD.

- Find the Annual Interest Rate: This is the percentage rate the bank offers. Remember to convert it to a decimal for calculation (e.g., 2.5% becomes 0.025).

- Identify the Term Length: This is the duration of your CD in years. If it’s in months, divide by 12 (e.g., 6 months is 0.5 years).

- Multiply to Find Interest: Multiply the Principal by the Annual Interest Rate by the Term Length.

- Add to Principal: Add the calculated interest to your original principal to find your total value at maturity.

For example, if you invest $10,000 in a 1-year CD at a 2.5% annual interest rate:

- Principal = $10,000

- Annual Rate = 0.025

- Term = 1 year

- Interest Earned = $10,000 0.025 1 = $250

- Total Value at Maturity = $10,000 + $250 = $10,250

For CDs that compound interest, the calculation becomes slightly more complex as interest starts earning interest. Most bank calculators will do this for you. For a simple estimate, this method provides a good baseline.

CD Growth Calculator

Building a CD Ladder: A Smart Strategy

A popular strategy for managing the illiquidity and reinvestment risk of CDs is to build a “CD ladder.” This involves dividing your total investment into several CDs with varying maturity dates.

For instance, if you have $15,000 to invest, you could put $5,000 into a 1-year CD, $5,000 into a 3-year CD, and $5,000 into a 5-year CD. As each CD matures, you can then reinvest the funds into a new, longer-term CD (e.g., when the 1-year CD matures, you buy a new 5-year CD).

This strategy offers several benefits:

- Increased Liquidity: A portion of your money becomes available at regular intervals, providing access to cash if needed.

- Mitigates Reinvestment Risk: You’re not putting all your money into a single rate at a single time. If rates rise, you can capture them as CDs mature.

- Potentially Higher Overall Returns: Longer-term CDs typically offer higher interest rates. A ladder allows you to consistently hold some funds in these higher-rate CDs while still having staggered access to your cash.

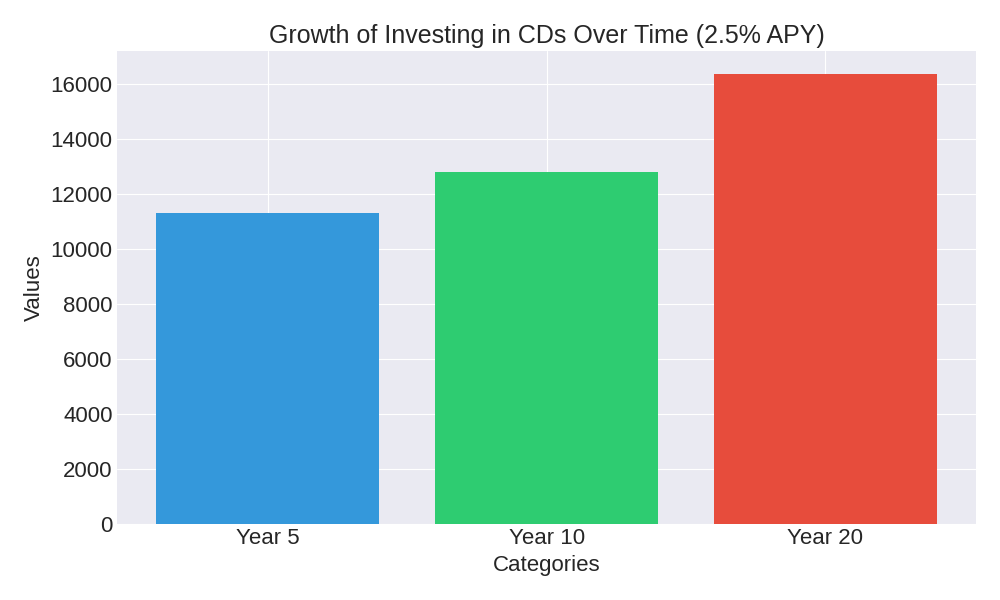

Compound Growth Scenario for CD Investment

To illustrate the growth potential of a CD, even at conservative rates, consider this compound growth scenario for a $10,000 initial investment, assuming a 2.5% annual percentage yield (APY) compounded annually.

This table demonstrates how your investment can grow over time, highlighting the power of compounding interest, where your interest earnings also start to earn interest.

| Time Period | Total Interest Earned | Total Value |

|---|---|---|

| Year 5 | $1,314.08 | $11,314.08 |

| Year 10 | $2,800.85 | $12,800.85 |

| Year 20 | $6,386.16 | $16,386.16 |

Key Considerations Before Investing

Before committing to investing in CDs, ask yourself these questions:

- What is your time horizon? How long can you comfortably lock away your money? Match your CD term to your financial goals.

- What are current interest rates? Compare rates from different banks and credit unions. Consider if current rates are attractive relative to inflation and other investment options.

- Do you need liquidity? If there’s a chance you’ll need the money before maturity, explore no-penalty CDs or a CD ladder strategy.

- What are the early withdrawal penalties? Understand the specific penalties of any CD before opening it. These can significantly reduce your earnings.

FAQ Section

Q: Are CDs truly risk-free?

A: CDs are considered one of the safest investment vehicles for your principal, especially when held in an FDIC-insured institution within the $250,000 limit. The primary “risk” is that their returns might not keep pace with inflation or higher-growth investments.

Q: Can I lose money on a CD?

A: You generally won’t lose your principal if your CD is held at an FDIC-insured institution and within the insurance limits. However, if you withdraw early, the penalty might eat into your earned interest and, in rare cases, a small portion of your principal if the penalty exceeds the interest earned.

Q: How do I choose the best CD?

A: Compare Annual Percentage Yields (APYs) from multiple banks and credit unions. Consider the term length that best suits your needs, the early withdrawal penalties, and whether you need any special features like bump-up or no-penalty options. Online banks often offer competitive rates.

Q: What is the difference between APY and interest rate?

A: The interest rate is the stated annual rate of interest. The Annual Percentage Yield (APY) reflects the actual annual rate of return, taking into account the effect of compounding interest. APY is generally a better measure to compare different CDs.

Q: Can I invest in CDs through a brokerage account?

A: Yes, you can invest in brokered CDs through a brokerage account. This can offer convenience and access to a wider selection of CDs from various banks, all managed in one place. You can learn more about general investment tools and regulations from resources like Investor.gov, a site by the SEC.

Conclusion

Investing in CDs can be an excellent strategy for preserving capital, earning predictable returns, and reaching specific financial goals with minimal risk. While they may not offer the explosive growth of stocks, their stability and FDIC insurance make them an invaluable tool for diversifying your portfolio and safeguarding your savings. By understanding the different types of CDs, their benefits, and potential drawbacks, you can make an informed decision about whether they align with your unique financial objectives.

Ready to Secure Your Savings?

Consider exploring CD options from various financial institutions. Compare rates, terms, and features to find the perfect fit for your savings goals. If you’re unsure, consult a qualified financial advisor to integrate CDs effectively into your broader investment plan.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.