Navigating the world of investments can feel complex, but understanding core principles can empower you to build lasting wealth. One such cornerstone is bond investing, a strategy favored by many for its potential to provide stability and consistent income. Unlike stocks, which represent ownership in a company, bonds are essentially loans you make to governments or corporations. In return, they promise to pay you regular interest payments and return your original investment at a specified future date. This guide will demystify bond investing, offering practical insights to help you integrate it effectively into your financial plan.

What Are Bonds? The Foundation of Fixed Income

At its simplest, a bond is an IOU. When you buy a bond, you are lending money to an issuer – be it a government, a municipality, or a corporation. In exchange for your loan, the issuer agrees to pay you interest over a set period and repay the principal amount (your initial loan) when the bond matures. This makes bonds a core component of fixed-income investing, as they typically provide predictable payments.

Imagine you lend a friend $1,000, and they promise to pay you back in five years, plus $50 in interest each year. That’s essentially how a bond works. Why does this matter in real life? It’s how organizations fund their operations and projects, from building new schools to expanding businesses, and it offers investors a way to earn a return with generally lower volatility than stocks.

Key Bond Characteristics You Need to Know

Understanding these fundamental terms is crucial for effective bond investing:

- Par Value (Face Value): This is the amount the issuer promises to repay you when the bond matures. Most bonds have a par value of $1,000.

- Coupon Rate (Interest Rate): This is the annual interest rate the issuer pays on the bond’s par value. If you have a $1,000 bond with a 3% coupon rate, you’ll receive $30 in interest annually.

- Maturity Date: This is the date when the issuer repays your principal. Bonds can have short-term maturities (under a year), medium-term (1-10 years), or long-term (over 10 years).

- Yield: This represents the actual return you receive on your bond investment, taking into account its purchase price, coupon payments, and time to maturity. It’s often different from the coupon rate.

For example, if you buy a bond with a $1,000 par value, a 5% coupon rate, and a 10-year maturity, you would typically receive $50 in interest annually for 10 years. At the end of the 10 years, you’d get your initial $1,000 back. This structured payment schedule is what attracts many investors to the world of bond investing.

Why Consider Bond Investing? Benefits and Risks

Bonds play a vital role in a diversified portfolio, offering distinct advantages and carrying specific risks. Balancing these is key to making informed investment decisions.

The Benefits of Bonds

- Income Generation: Bonds provide a steady stream of income through regular interest payments. This can be especially appealing for retirees or those seeking predictable cash flow.

- Portfolio Diversification: Bonds often behave differently from stocks. When stocks decline, bonds can sometimes hold their value or even increase, helping to stabilize your overall portfolio. This is known as a negative correlation.

- Capital Preservation: Because bond issuers are obligated to repay the principal, bonds are generally considered less volatile than stocks, offering a degree of protection for your initial investment.

- Lower Volatility: While not risk-free, bonds typically experience smaller price swings compared to equities, making them a calmer component of an investment strategy.

The Risks of Bonds

While generally safer, bonds are not without risk:

- Interest Rate Risk: When prevailing interest rates rise, newly issued bonds offer higher coupon rates, making existing bonds with lower rates less attractive. This can cause the market price of your existing bonds to fall if you need to sell them before maturity.

- Inflation Risk: If inflation (the rate at which prices rise) is higher than your bond’s yield, the purchasing power of your interest payments and principal repayment can erode over time. Imagine your bond pays 3% annually, but inflation runs at 5%; your real return is actually negative.

- Credit Risk (Default Risk): This is the risk that the bond issuer may be unable to make its interest payments or repay your principal. Government bonds from stable countries (like U.S. Treasuries) have very low credit risk, while some corporate bonds carry higher risk.

Types of Bonds: Understanding Your Options

The bond market is vast, offering a variety of choices depending on your risk tolerance and financial goals.

Government Bonds

Issued by national governments, these are generally considered among the safest investments, especially those from economically stable countries.

- U.S. Treasury Bonds, Notes, and Bills: These are debt obligations of the U.S. government, offering varying maturities. Treasury Bills (T-Bills) mature in a year or less, Treasury Notes (T-Notes) in 2-10 years, and Treasury Bonds (T-Bonds) in 20-30 years. They are backed by the “full faith and credit” of the U.S. government. You can learn more about these directly from the U.S. Department of the Treasury at TreasuryDirect.gov.

- Treasury Inflation-Protected Securities (TIPS): These bonds are designed to protect investors from inflation. Their principal value adjusts with the Consumer Price Index (CPI), so both your principal and interest payments rise with inflation.

Corporate Bonds

These are issued by companies to raise capital for various corporate purposes, such as expansion or debt refinancing. They offer higher yields than government bonds because they carry higher credit risk. The yield you receive depends largely on the creditworthiness of the issuing company. For instance, a stable, well-established utility company might issue bonds with a lower yield but higher safety than a new, high-growth technology startup that needs to offer a much higher yield to attract investors.

Municipal Bonds (“Munis”)

Issued by state and local governments, these bonds finance public projects like schools, roads, or hospitals. A significant feature of municipal bonds is that their interest income is often exempt from federal income tax, and sometimes state and local taxes as well, especially if you live in the state where the bond was issued. This tax advantage can make them particularly attractive to high-income earners.

How to Calculate Bond Yield (Plain Language)

Understanding yield helps you compare different bonds and assess your actual return. It’s more than just the coupon rate.

To grasp the basics, let’s look at Current Yield. This is a straightforward measure of the annual income from a bond relative to its current market price.

How to Calculate Current Yield:

1. Find the Annual Interest Payment: This is your bond’s par value multiplied by its coupon rate. For example, a $1,000 par value bond with a 4% coupon pays $40 per year.

2. Find the Bond’s Current Market Price: This is what someone would pay for the bond today. Bonds are traded on a market, so their price fluctuates.

3. Divide Annual Interest by Current Market Price: If your $40/year bond is currently trading at $950, your current yield is $40 / $950 = 0.0421, or 4.21%.

Why does this matter in real life? If a bond’s price has fallen below its par value (trading at a “discount”), its current yield will be higher than its coupon rate. Conversely, if it’s trading above par (at a “premium”), its current yield will be lower. This helps you compare bonds on an apples-to-apples basis when their market prices differ.

Yield to maturity (YTM) is a more comprehensive measure, calculating the total return an investor will receive if they hold the bond until it matures. It considers the current market price, par value, coupon interest rate, and time to maturity. Because it involves present value calculations, it’s generally best understood using a financial calculator or software. However, the key takeaway is that YTM gives you the most accurate picture of your potential total return.

Bond Investment Return Estimator

Annual Coupon Payment: $0.00

Total Interest Income: $0.00

Capital Gain/Loss: $0.00

Total Return on Investment: $0.00

Total Return Percentage: 0.00%

Building Your Bond Portfolio: A Step-by-Step Guide

Creating a bond portfolio requires thoughtful planning, much like any other investment. Here’s a structured approach:

- Define Your Financial Goals: Are you saving for retirement, a down payment, or income generation? Your goals will influence the types and maturities of bonds you choose. An investor in their 60s might prioritize income and capital preservation with shorter-term, high-quality bonds, while a younger investor might consider some longer-term bonds for higher potential yields.

- Assess Your Risk Tolerance: How much risk are you comfortable with? Generally, higher potential returns come with higher risk. U.S. Treasury bonds are very low risk, while corporate junk bonds carry much higher risk.

- Choose Your Bond Types: Based on your goals and risk tolerance, select from government, corporate, or municipal bonds. Consider their tax implications. For example, if you’re in a high tax bracket, municipal bonds might offer better after-tax returns.

- Diversify Your Holdings: Don’t put all your eggs in one basket. Diversify across different issuers, industries, credit ratings, and maturity dates. This helps mitigate risks like credit risk or interest rate risk.

- Consider Bond Funds or ETFs: For many investors, purchasing individual bonds can be complex and require significant capital. Bond mutual funds and Exchange Traded Funds (ETFs) offer instant diversification, professional management, and liquidity. You can learn more about various investment products from reliable sources like the U.S. Securities and Exchange Commission.

- Monitor and Rebalance: Periodically review your bond portfolio to ensure it aligns with your goals. Interest rates, inflation, and your personal circumstances can change, necessitating adjustments to your bond holdings.

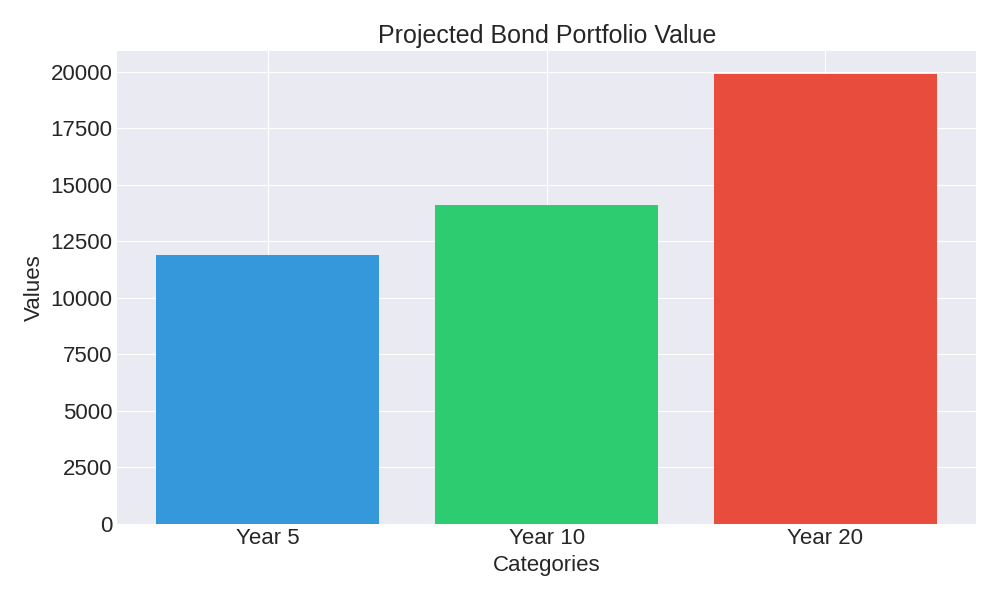

Case Study: Compound Growth Scenario for a Bond Portfolio

Let’s consider a scenario where an investor allocates a portion of their portfolio to bonds, aiming for steady returns. While specific returns vary, we can illustrate the power of compounding.

Imagine an initial investment of $10,000 in a diversified bond portfolio yielding an average annual return.

| Time Horizon | Average Annual Return | Projected Value |

|---|---|---|

| Year 5 | 3.5% | ~$11,870 |

| Year 10 | 3.5% | ~$14,106 |

| Year 20 | 3.5% | ~$19,898 |

Note: This is an illustrative example; actual returns are not guaranteed and will vary based on market conditions and specific bond performance. This table shows how even modest, consistent returns from bonds can lead to significant wealth growth over time.

Frequently Asked Questions (FAQ)

Here are answers to some common questions about bond investing:

- Are bonds always safe? While generally less risky than stocks, bonds are not entirely risk-free. They carry interest rate risk, inflation risk, and credit risk. The “safest” bonds are typically those issued by highly stable governments.

- Should I buy individual bonds or bond funds? For most individual investors, bond funds or ETFs are a more practical choice. They offer diversification, professional management, and liquidity, which can be challenging to achieve with individual bonds unless you have substantial capital.

- What happens to my bonds if interest rates change? If interest rates rise, newly issued bonds offer higher yields, making your existing lower-yielding bonds less attractive to potential buyers, which can cause their market price to fall. Conversely, if rates fall, your bonds become more attractive, and their market price may rise. If you hold a bond to maturity, these price fluctuations usually don’t affect your final principal repayment.

- How do bond ratings work? Credit rating agencies like Moody’s, Standard & Poor’s, and Fitch assess the financial health of bond issuers and assign ratings. Bonds rated “investment grade” (e.g., AAA, AA, A, BBB) are considered less risky than “high-yield” or “junk bonds” (e.g., BB, B, CCC), which offer higher potential returns to compensate for higher risk. For more insights on financial markets, check out Bloomberg.com.

Conclusion

Bond investing offers a valuable pathway to secure wealth growth, providing a balance of income generation, diversification, and capital preservation. By understanding the different types of bonds, their inherent risks and benefits, and how to strategically build a portfolio, you can make informed decisions that align with your financial objectives. Remember, a well-rounded investment strategy often includes a thoughtful allocation to both stocks and bonds.

Your Call to Action: Take the first step towards a more secure financial future. Research different bond options, consider your risk tolerance, and explore how bonds can fit into your unique investment plan. If you’re unsure, consult with a qualified financial advisor to tailor a strategy that best suits your needs.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.