Are you seeking a reliable path to generate passive income with a relatively low risk profile? Then investing in tax lien certificates might be exactly what you’re looking for. This guide will demystify the process, explain the potential benefits, and highlight the crucial steps to embark on a successful journey in this unique investment niche. We aim to provide the most comprehensive and actionable insights available, simplifying complex concepts without sacrificing depth.

In essence, investing in tax lien certificates means you are paying a property owner’s overdue property taxes. In return, the local government grants you a lien certificate. This certificate acts as a claim against the property. When the homeowner eventually pays their taxes (plus penalties and interest), you, the investor, receive your initial investment back, along with a significant rate of return. If they don’t, you could potentially acquire the property. It’s a structured approach to earning interest, backed by real estate.

What Exactly is a Tax Lien?

A tax lien is a legal claim a government entity places on a property when the owner fails to pay their property taxes. It’s a critical mechanism for local governments to fund essential services like schools, police, and infrastructure. Without a way to enforce tax collection, these services would quickly falter.

Why does this matter in real life? Imagine a homeowner, perhaps facing unexpected medical bills or job loss, falls behind on their property taxes. The city or county still needs those funds. Instead of immediately seizing the property, they issue a tax lien, which can then be sold to investors. This process gives the homeowner more time to pay and ensures the municipality receives its revenue.

The Government’s Power to Attach Liens

Local governments have the legal authority to attach liens to real estate. This power ensures the stability of local finances. The lien essentially “follows” the property, meaning it must be satisfied before the property can be sold or transferred free and clear to a new owner. It’s a powerful incentive for property owners to stay current on their obligations.

How Tax Lien Investing Works: A Step-by-Step Guide

Investing in tax lien certificates involves a structured process, primarily through public auctions. These auctions are typically held by county tax collector’s offices or treasurers.

Scenario: Investing in a Tax Lien Auction

Imagine you’re at a county tax lien auction. A property with $3,000 in overdue taxes and penalties is up for bid. The state has set a maximum interest rate of 12% per year. Bidders compete, not on the principal amount, but on the interest rate they are willing to accept. The investor willing to accept the lowest interest rate wins the lien. If you bid 8% and win, you pay the $3,000. If the homeowner redeems it in 6 months, you get your $3,000 back plus 8% prorated annual interest.

Here’s a breakdown of the typical process:

- Step 1: Research and Due Diligence. Before you even consider bidding, identify properties with delinquent taxes. This involves researching property records, assessing property values, and understanding the local market. You need to know what you’re investing in.

- Step 2: Attend a Tax Lien Auction. Counties hold these auctions periodically, often annually. You can attend in person or, increasingly, online. Familiarize yourself with the auction rules, which vary by jurisdiction.

- Step 3: Bid on Tax Lien Certificates. Bidding processes differ. Some states use a premium bid (investors bid up the price of the certificate), while others use an interest rate bid (investors bid down the interest rate they are willing to accept). The goal is to secure a lien with a favorable return.

- Step 4: Receive the Tax Lien Certificate. If you’re the winning bidder, you’ll pay the delinquent tax amount. In exchange, you receive a tax lien certificate. This document is your proof of investment and outlines the terms, including the interest rate you’ll earn.

- Step 5: Wait for Redemption or Foreclose. The property owner typically has a “redemption period” (e.g., one to three years) to pay their back taxes plus the interest and penalties to you. If they redeem, you get your money back with the agreed-upon interest. If they fail to redeem within the specified period, you may have the right to initiate foreclosure proceedings to acquire the property.

Benefits of Tax Lien Investing

For many, investing in tax lien certificates offers an attractive alternative to traditional investments, primarily due to several compelling advantages:

- Potentially High Returns: Interest rates on tax lien certificates can be quite competitive, often ranging from 8% to 18% or more, depending on the state and jurisdiction. This is often higher than what you might find in savings accounts or even some bonds.

- Government Backed: The lien is against the property itself, and the debt is collected by the local government. This provides a strong level of security. Your investment is secured by real estate, a tangible asset.

- Passive Income Potential: Once you purchase a lien, your role is largely passive. You wait for the property owner to redeem the lien. This makes it suitable for investors looking for income without active management.

- Priority Lien Position: Tax liens generally hold a superior position to almost all other liens, including mortgages. This means if the property were to be foreclosed upon, tax liens are typically paid first from the proceeds.

Understanding the Risks and Challenges

While attractive, tax lien investing isn’t without its caveats. Being aware of the risks is crucial for making informed decisions.

- Redemption Delays: Property owners might take the entire redemption period, or even longer if legal challenges arise, to pay their taxes. Your capital could be tied up for an extended period, impacting your liquidity.

- Foreclosure Process: If a property owner doesn’t redeem, you might need to initiate foreclosure. This is a legal process that can be costly, time-consuming, and require legal assistance. It’s not a guaranteed quick property acquisition.

- Lack of Liquidity: A tax lien certificate is not easily convertible to cash. You typically have to wait for the redemption or go through foreclosure. This means your funds are locked in for the duration of the lien.

- Property Value Fluctuations: While the lien is senior, unexpected events (e.g., environmental contamination, natural disasters) could significantly reduce the property’s value. If you end up foreclosing, the property might not be worth what you paid for the lien and associated costs.

- Competition: Popular tax lien auctions, especially those with high interest rates, can attract many bidders, driving down the achievable interest rate.

How to Calculate Potential Returns on a Tax Lien

Calculating the potential return on a tax lien certificate is straightforward, primarily involving the initial investment and the awarded interest rate.

Why does this matter in real life? Understanding this calculation helps you evaluate if a specific tax lien certificate meets your investment goals. It prevents you from overpaying or accepting an inadequate return for your capital.

Here’s a practical way to think about it:

- Start with the Lien Amount: This is the total sum of delinquent taxes, penalties, and fees you paid.

- Identify the Annual Interest Rate: This is the rate you secured at auction (e.g., 10% per year).

- Determine the Redemption Period: How long the property owner has to pay.

Let’s say you invest $5,000 in a tax lien certificate with an annual interest rate of 8%.

To find the interest earned for one year, you would multiply the Lien Amount by the Annual Interest Rate: $5,000 * 0.08 = $400. So, after one year, your total return would be $5,400 if redeemed.

If the lien is redeemed after, say, six months, you would typically earn a prorated portion of that annual interest. So, for six months, it would be half of the annual interest: $400 / 2 = $200. Your total return would then be $5,200.

Tax Lien Investment Return Calculator

Many jurisdictions also add additional penalties or fees upon redemption, which further increase your return. Always review the specific state and local laws for these details. You can often find official rules and regulations on a state’s Department of Revenue or local county government websites, such as those linked from USA.gov.

Key Considerations Before Investing

Before diving into tax lien investing, a few critical aspects demand your attention to ensure a well-informed strategy.

- State and Local Laws: Tax lien laws vary significantly from state to state and even county to county. Research redemption periods, interest rates, notification requirements, and the foreclosure process in your target jurisdiction. Some states, like Florida, are “tax deed” states, meaning you bid on the property itself, not just the lien. Other states are “tax lien” states.

- Due Diligence on Properties: Never invest blindly. Research the property’s value, condition, zoning, and any other existing liens (though tax liens are typically superior). A property that appears abandoned or in poor condition may eventually lead to foreclosure, which means taking on responsibility for it.

- Understand the Foreclosure Process: Be prepared for the possibility of foreclosure. This includes understanding the legal steps, potential costs (attorney fees, court costs), and your responsibilities if you become the property owner.

- Liquidity Needs: As mentioned, tax liens are not liquid investments. Ensure you have adequate funds for other financial obligations while your capital is tied up in a tax lien certificate.

- Seek Professional Advice: Consider consulting with a real estate attorney or a financial advisor experienced in tax lien investing. They can provide tailored advice based on your specific situation and the nuances of local laws.

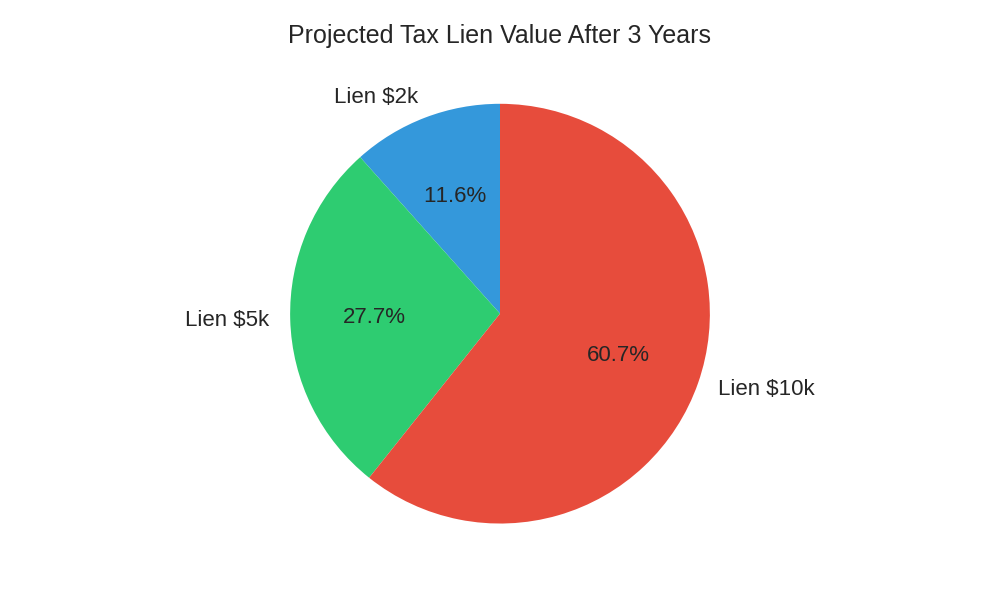

Tax Lien Investment Growth Scenario

To illustrate the potential of tax lien investing, let’s consider a scenario with a consistent annual interest rate. This table shows how your initial investment could grow due to accrued interest over different periods if the lien remains unredeemed and continues to accrue interest (or penalties, depending on local laws) until eventual redemption or foreclosure.

| Initial Lien Value | Annual Interest Rate | Value After 3 Years* |

|---|---|---|

| $2,000 | 10% | $2,600 |

| $5,000 | 8% | $6,200 |

| $10,000 | 12% | $13,600 |

*Note: This simplified table assumes the lien accrues simple interest annually and is unredeemed for the full period. Actual returns can vary based on redemption timing, additional fees, and specific state laws.

Frequently Asked Questions (FAQ)

Q1: Is tax lien investing risky?

A: Like any investment, it carries risks. The primary risks include redemption delays (tying up your capital), the potential need to go through a foreclosure process, and variations in property values. However, it’s generally considered less volatile than stock market investing and is backed by real estate.

Q2: What’s the difference between a tax lien and a tax deed?

A: With a tax lien, you buy the right to collect delinquent taxes plus interest. If the homeowner doesn’t pay, you might eventually get the property through foreclosure. With a tax deed, you are bidding on the property itself (often after a failed tax lien redemption period). If you win a tax deed auction, you typically take immediate ownership of the property.

Q3: How do I find tax lien auctions?

A: Most county tax collector or treasurer offices hold annual or semi-annual tax lien auctions. Many now offer online auctions. Check your local county government website for schedules and registration details. Websites like The National Association of Counties (NACo) can sometimes point to resources.

Q4: Do I need a lot of money to start?

A: Not necessarily. Tax lien certificates can be purchased for amounts ranging from a few hundred dollars to tens of thousands. This accessibility allows investors with varying capital to participate. However, having enough capital to cover potential legal fees if foreclosure becomes necessary is wise.

Q5: What happens if the homeowner never pays?

A: If the homeowner doesn’t redeem the lien within the statutory period, you, as the lienholder, typically gain the right to initiate a foreclosure proceeding. This legal action can ultimately lead to you acquiring ownership of the property. This is a significant consideration and requires careful planning and legal understanding.

Conclusion

Investing in tax lien certificates offers a unique opportunity for passive income, often with attractive, government-backed returns. While the process requires diligent research and an understanding of local laws and potential risks, the rewards can be substantial. It’s a method of putting your capital to work by supporting local government functions while potentially securing a valuable asset or a steady stream of interest income.

Ready to Explore Tax Lien Investing?

Begin your journey by researching your local county’s tax collector website or consulting a financial professional specializing in real estate. Education is your best tool for success in this rewarding investment arena. Start exploring today to see if this path aligns with your financial goals!

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.