Feeling like your home’s growing value is trapped, just sitting there while inflation shrinks your savings or urgent needs demand attention? You’ve built a significant asset, and it’s time to understand how to leverage it intelligently. Many homeowners eye their equity as a golden goose, but extracting that value requires strategy, not just a quick pull. This isn’t about vague financial concepts; it’s about making your home’s potential work for you, safely and effectively.

As your advocate and strategist, I’m here to cut through the noise. We’ll explore how to approach investing in home equity not as a last resort, but as a calculated move to build greater wealth or address critical financial goals. You deserve to maximize your assets without falling into common traps.

Understanding Your Equity Power: More Than Just a Number

Your home equity isn’t just the difference between your home’s value and what you owe. It’s a powerful, tangible asset that can be unlocked. Think of it as a low-cost capital source, often cheaper than personal loans or credit cards, because it’s secured by your home. The critical question isn’t “Do I have equity?” but “How can I make this equity work harder for me?”

Why Your Equity Matters in Real Life

Imagine you purchased your home for $300,000 with a $270,000 mortgage. Years later, your home is now worth $450,000, and you’ve paid down your mortgage to $200,000. Your equity isn’t just $150,000; it’s the potential to access funds that could fuel a major renovation, consolidate high-interest debt, or even provide capital for a new venture. This matters because it gives you options, control, and often, a much lower cost of borrowing than other financing methods.

- Insider Tip: Don’t just look at market value; factor in how much you’ve paid down your principal. Both contribute to your usable equity.

- Common Myth to Avoid: “Equity is just a number until I sell.” This is false. You can access a significant portion of your equity without selling your home, but it must be done wisely.

Strategic Ways to Tap Into Your Equity

There are several primary methods to access your home equity, each with its own structure and implications. Understanding these is the first step to truly investing in home equity successfully.

Cash-Out Refinance: A Fresh Start, Potentially

A cash-out refinance replaces your existing mortgage with a new, larger one. You receive the difference in cash. This can be appealing if current interest rates are lower than your existing mortgage, allowing you to secure a better rate while also accessing funds. However, you’re restarting your loan term, potentially extending the total time you’re paying off your home.

- Scenario: You owe $200,000 at 5% on your original mortgage. Your home is worth $400,000. You could refinance to a new $250,000 mortgage at 4.0% (if rates are favorable), receiving $50,000 cash. Your monthly payments might increase, but you’ve unlocked significant capital at a lower overall interest rate.

- Why this matters: This is best when interest rates are low and you need a lump sum. You’re trading a longer repayment period for potentially lower interest and immediate cash.

Home Equity Line of Credit (HELOC): Flexible Access

A HELOC is a revolving credit line, similar to a credit card, but secured by your home. You can borrow, repay, and re-borrow funds up to an approved limit for a set draw period (e.g., 10 years). Interest rates are typically variable, meaning they can change over time.

- Scenario: You have an emergency fund gap, or you’re planning phased home improvements. A HELOC allows you to draw only what you need, when you need it, avoiding interest on the full amount until you use it. If you need $10,000 for a bathroom renovation now and $15,000 for a kitchen update next year, a HELOC offers that flexibility.

- Why this matters: Flexibility is key here. It’s ideal for ongoing or unpredictable expenses, but you must be disciplined, as variable rates can increase your payments.

Home Equity Loan (HEL): Predictable Payments

A home equity loan is a second mortgage that provides a lump sum of cash upfront. You repay it with fixed monthly payments over a set period (e.g., 5-15 years) at a fixed interest rate. This offers predictability, as your payments won’t change.

- Scenario: You need a specific amount of money for a large, one-time expense, like consolidating high-interest credit card debt or funding a child’s education. A HEL gives you the full amount immediately with a clear repayment schedule and a stable interest rate.

- Why this matters: Fixed rates and predictable payments provide budget stability, making it suitable for large, planned expenses where you want certainty.

Maximizing Your Equity: Where the Smart Money Goes

Simply tapping your equity isn’t enough; the goal is to use it to generate a greater return or solve a high-cost problem. This is the essence of truly investing in home equity.

Home Improvements That Add Real Value

Not all renovations are equal. Using your equity for strategic upgrades can increase your home’s appraisal value, effectively giving you a return on your investment. Focus on high-impact areas.

- Examples: Kitchen and bathroom remodels, adding a deck, replacing old windows for energy efficiency, or finishing a basement. These typically yield the highest return on investment.

- Mini Case Study: Imagine you use $40,000 from a HELOC for a kitchen renovation. A year later, comparable homes with updated kitchens in your area sell for $50,000-$60,000 more than those without. You’ve potentially increased your home’s value by more than your initial investment, a smart financial play.

- Common Myth to Avoid: “Every renovation increases my home’s value dollar-for-dollar.” This is false. Highly personalized or over-the-top renovations might not appeal to future buyers, resulting in a poor return. Focus on broad appeal and essential upgrades. You can research typical ROI for home improvements from reputable sources like Remodeling Magazine’s Cost vs. Value Report.

Debt Consolidation: A Double-Edged Sword

Using home equity to pay off high-interest credit card debt (e.g., 20-25% APR) or personal loans (e.g., 10-15% APR) can save you thousands in interest. You’re trading unsecured, high-rate debt for secured, lower-rate debt.

- Why this matters: It can significantly reduce your monthly payments and free up cash flow. However, if you don’t address the spending habits that led to the debt, you could end up with more debt and risk losing your home. This is a powerful tool, but it demands financial discipline.

Investing in Other Assets: High Risk, High Reward

While less common and higher risk, some use home equity to invest in other income-generating assets, like a down payment on a rental property or a diversified investment portfolio. This should only be considered if you have a strong emergency fund, stable income, and a high tolerance for risk.

- Pro/Con: The potential for significant returns exists, but so does the risk of losing both your investment and your home if the market turns. This strategy requires careful research and often, professional guidance. You can learn more about managing investment risk from the U.S. Securities and Exchange Commission.

Calculating Your Equity Potential and Costs

Understanding the numbers is paramount. Here’s a practical way to assess your situation.

How to Calculate Your Usable Equity

First, get an estimated value of your home. You can use online tools for initial estimates, but an appraisal provides the most accurate figure. Then, find your current mortgage balance. Most lenders allow you to borrow up to 80% or 85% of your home’s value. The formula looks like this:

1. Estimate Your Home’s Value: Let’s say $400,000.

2. Determine Your Current Mortgage Balance: Assume $150,000.

3. Calculate Your Total Equity: $400,000 (Value) – $150,000 (Mortgage) = $250,000.

4. Calculate Your Usable Equity (LTV Limit): If your lender allows borrowing up to 80% Loan-to-Value (LTV):

- 80% of Home Value: $400,000 * 0.80 = $320,000.

- Usable Equity: $320,000 (80% LTV) – $150,000 (Mortgage Balance) = $170,000.

This means you could potentially borrow up to $170,000. This calculation provides a realistic estimate of the funds you could access.

Calculate the potential net profit from leveraging your home equity for an investment.

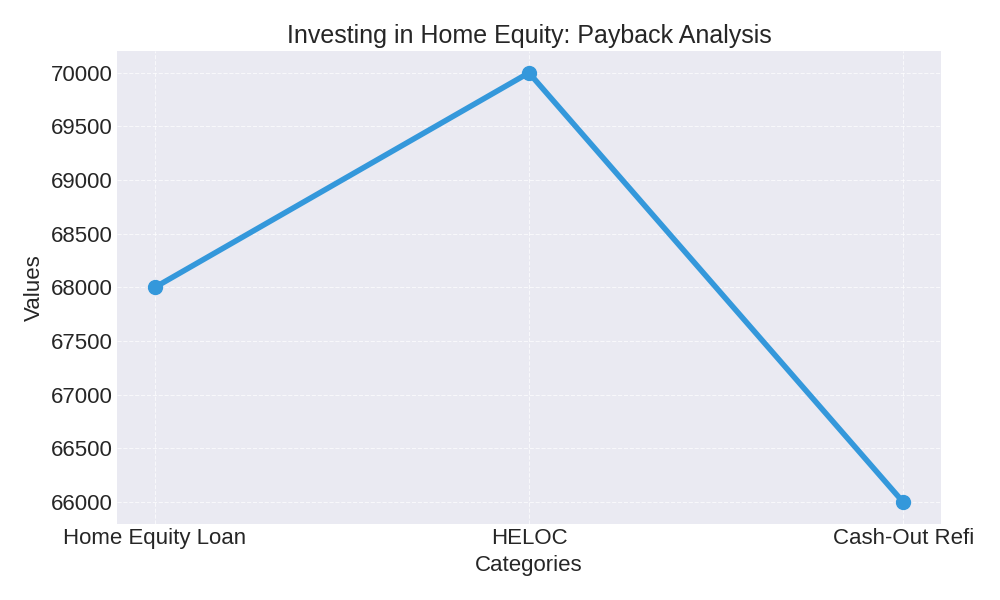

Now, let’s look at the long-term impact of different financing options:

| Financing Method | Typical APR Range | Estimated Total Payback (10-Year Term for a $50,000 Loan) |

|---|---|---|

| Home Equity Loan | 6.5% – 9.0% | $68,000 – $75,000 |

| HELOC (Average Rate) | 7.0% – 10.0% | $70,000 – $80,000 (assuming steady draws & average rates) |

| Cash-Out Refinance | 6.0% – 8.5% | $66,000 – $72,000 (this is the cost of the $50k portion, part of a larger mortgage) |

*These are illustrative ranges for a $50,000 loan over 10 years and do not include closing costs or fees, which can vary significantly. Actual rates depend on credit score, lender, and market conditions.

Risks and How to Mitigate Them

Leveraging your home equity isn’t without risk. You are taking on additional debt, secured by your primary asset. Understanding these risks is crucial for making informed decisions.

- Market Downturns: If home values decline, you could end up owing more than your home is worth (being “underwater”). This makes it difficult to sell or refinance.

- Over-Leveraging: Taking out too much equity can leave you with little financial cushion. An unexpected job loss or medical emergency could make payments unmanageable.

- Repayment Struggles: If you can’t make your payments, your lender could foreclose on your home. This is the ultimate risk of using your home as collateral.

- Insider Tip: Always have an emergency fund covering 3-6 months of living expenses separate from your equity. Before taking out a loan, “stress test” your budget by adding the new payment and seeing if you could comfortably afford it even if your income dipped slightly. You can find robust financial planning tools on sites like Fidelity or Charles Schwab.

- Common Myth to Avoid: “Home values always go up.” While historically true over long periods, real estate markets have cycles. Relying solely on continuous appreciation is risky.

Conclusion: Empowering Your Home Equity Decisions

Accessing your home equity isn’t a decision to take lightly, but when approached strategically, it can be a powerful financial tool. Whether you’re enhancing your home’s value, consolidating high-interest debt, or carefully investing, the key is understanding the options, calculating the costs, and mitigating the risks. You now have the knowledge to move forward with a clear, informed strategy.

Ready to Make Your Home Work Harder?

Armed with this expert insight, take the next step. Calculate your specific usable equity, research current rates from multiple lenders, and consider consulting a qualified financial advisor. They can help you tailor a plan that aligns with your unique financial goals and risk tolerance. Your home is a cornerstone of your wealth—manage it like one.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.