Building a secure financial future often feels like a complex puzzle. Many people wonder how to make their money grow without becoming a full-time stock market guru. The simple answer for many is investing in funds. These powerful financial tools offer diversification and professional management, making them accessible even for beginners. This guide will demystify the process, providing you with a clear roadmap for how to confidently start investing in funds to build your wealth over time.

What Are Investment Funds? Understanding the Basics

At its core, an investment fund is a pool of money from many investors. This collective money is then used by a professional fund manager to buy a diversified portfolio of stocks, bonds, or other securities. Think of it like a community garden. Instead of each person buying a single plant, everyone contributes money, and a gardener buys and manages a variety of plants for the entire community. Everyone shares in the harvest.

This pooling mechanism allows individual investors to gain exposure to a broad range of assets that would be difficult or expensive to buy on their own. Why does this matter in real life? It means you can own a tiny piece of many different companies or bonds without needing vast amounts of capital or research time. It’s a way to achieve instant diversification.

The Power of Diversification: Spreading Your Risk

Diversification is key to managing risk in investing. By spreading your investments across various assets, you reduce the impact of any single asset performing poorly. For instance, if you invest all your money in one company and it struggles, your entire investment is at risk. A fund, however, might hold shares in hundreds of companies across different industries. If one company falters, the impact on your overall fund performance is minimal.

This strategy helps smooth out returns over the long term. It minimizes the roller-coaster effect that can come from owning just a few individual stocks. As the U.S. Securities and Exchange Commission (SEC) often emphasizes, diversification is a fundamental principle for sound investing. You can learn more about investor education from SEC.gov.

Types of Funds: Diversification at Your Fingertips

There are several types of investment funds, each with unique characteristics. Understanding these will help you choose the right fit for your financial goals and risk tolerance.

- Mutual Funds: These are professionally managed portfolios that can invest in stocks, bonds, or other assets. They are actively managed, meaning a fund manager makes buy and sell decisions in an attempt to outperform the market.

- Exchange-Traded Funds (ETFs): ETFs typically track an index, like the S&P 500, or a specific sector. They trade on stock exchanges throughout the day, much like individual stocks. They often have lower fees than actively managed mutual funds because they aren’t trying to beat the market, just match it.

- Index Funds: A specific type of mutual fund or ETF designed to track a market index. They offer broad market exposure with minimal management fees due to their passive strategy.

- Bond Funds: These funds invest primarily in a portfolio of bonds. They are generally considered less volatile than stock funds and can be a good option for investors seeking income or looking to reduce overall portfolio risk.

Imagine you are a new investor with $5,000. Instead of trying to pick individual winning stocks, you could put that entire amount into an S&P 500 index fund. This instantly gives you exposure to the performance of 500 of the largest U.S. companies. Why does this matter? You’re not relying on the success of just one or two companies; your investment is tied to the broader U.S. economy, historically a strong performer over the long run.

Why Invest in Funds? The Practical Benefits

Investing in funds offers numerous advantages that make them appealing to both novice and experienced investors alike.

- Professional Management: Your money is managed by experts who conduct research and make investment decisions. This saves you significant time and effort.

- Diversification: Funds hold a variety of securities, spreading your risk more effectively than owning a few individual assets. This helps protect your portfolio from sharp declines if one particular asset performs poorly.

- Accessibility: You can start investing in funds with relatively small amounts, often with minimum investments as low as $50 or $100 for some ETFs.

- Liquidity: Most funds allow you to buy and sell shares easily, converting your investment back to cash when needed.

- Cost-Effective: While funds have fees, the cost of gaining broad diversification through a fund is often much lower than trying to build a similar portfolio by purchasing individual stocks and bonds.

Getting Started: Your Fund Investment Journey

Embarking on your investment journey is simpler than you might think. Here’s a step-by-step approach to begin investing in funds:

Understanding Fund Costs and Fees

While convenient, funds do come with costs. These fees can eat into your returns over time, so it’s crucial to understand them. The main types of fees include:

- Expense Ratio: This is an annual fee charged as a percentage of your total investment. It covers management fees, administrative costs, and other operating expenses. For example, a 0.50% expense ratio means you pay $5 annually for every $1,000 invested.

- Sales Loads (Commissions): Some mutual funds charge a sales load when you buy (front-end load) or sell (back-end load) shares. ETFs typically do not have sales loads, though you might pay a trading commission similar to buying a stock.

- Trading Fees: If the fund frequently buys and sells securities within its portfolio, these transaction costs are passed on to investors, indirectly affecting returns.

Why does this matter? Even a small difference in expense ratios can have a huge impact over decades. Imagine two funds, both returning 7% annually before fees. Fund A has a 1.0% expense ratio, and Fund B has a 0.2% expense ratio. Over 20 years, an initial $10,000 investment would be significantly larger in Fund B due to compounding returns being less eroded by fees. Always compare the expense ratio when choosing a fund.

How to Calculate Your Potential Fund Growth

Understanding how your investments might grow over time is crucial. The magic behind long-term investing is compound growth – earning returns not only on your initial investment but also on the accumulated returns from previous periods. You don’t need complex math. Just think of it as your money making more money, which then makes even more money.

Imagine you invest $1,000 today and it grows by 7% in the first year. You’d have $1,070. In the second year, you’d earn 7% not just on your initial $1,000, but on the full $1,070, resulting in more growth. This snowball effect accelerates over time. To get a rough idea, you can use the “Rule of 72” which states that dividing 72 by your annual rate of return (e.g., 7%) gives you the approximate number of years it will take for your investment to double. So, at 7%, your money would double in about 10 years (72/7 ≈ 10.3).

Your Fund Growth Projection

While it’s impossible to predict exact returns, understanding this principle helps visualize long-term potential. Consistent contributions greatly amplify this effect.

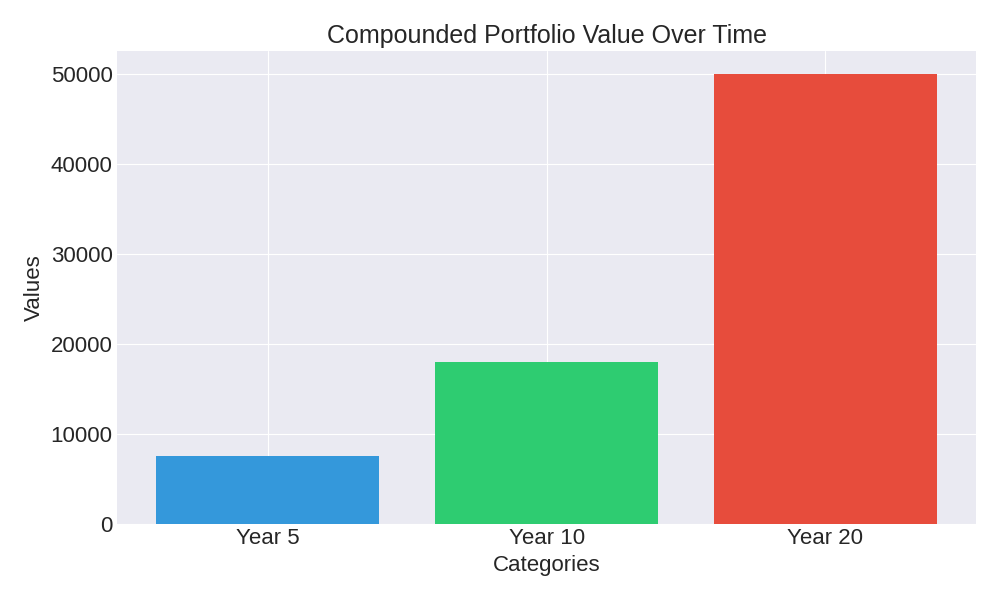

Compound Growth Scenario: Visualizing Long-Term Value

This table illustrates the power of compounding with regular contributions. Let’s assume an initial investment of $1,000 and an additional $100 contributed monthly (total $1,200 annually), earning a hypothetical annual return of 7% before taxes and fees.

| Investment Horizon | Total Contributions | Estimated Portfolio Value |

|---|---|---|

| Year 5 | ~$6,000 – $7,000 | ~$7,500 – $8,500 |

| Year 10 | ~$12,000 – $13,000 | ~$18,000 – $20,000 |

| Year 20 | ~$24,000 – $25,000 | ~$50,000 – $55,000 |

*These numbers are purely illustrative and do not guarantee actual returns. Returns can vary significantly based on market conditions, fees, and actual investment performance.

Common Questions About Investing in Funds (FAQ)

Q1: How much money do I need to start investing in funds?

A: You can start with relatively small amounts. Some ETFs allow you to buy a single share, which could be around $50-$200. Many mutual funds have minimum initial investments ranging from $500 to $3,000, but some offer lower minimums for automatic monthly contributions. Many brokerage accounts now offer fractional shares of ETFs, making it even more accessible.

Q2: Are funds safe? What are the risks?

A: Funds, like all investments, carry risk. The value of your investment can go up or down. Key risks include market risk (the overall market declines), interest rate risk (for bond funds), and specific company risk (though diversified funds mitigate this). Funds are generally considered safer than investing in individual stocks because of their built-in diversification. However, there is no guarantee of returns, and you could lose money. It’s important to understand that “safe” doesn’t mean “risk-free” in investing.

Q3: Should I choose an actively managed fund or an index fund/ETF?

A: This depends on your philosophy. Actively managed funds aim to beat the market but come with higher fees. Index funds and ETFs aim to match market performance at a lower cost. Historically, many actively managed funds struggle to consistently beat their benchmarks after fees. For many investors, low-cost index funds or ETFs are an excellent, simple choice for long-term growth. To understand current market trends and different investment options, resources like Bloomberg.com can be helpful.

Q4: How often should I check my fund investments?

A: For long-term investors, frequent checking can lead to emotional decisions. A good practice is to review your portfolio quarterly or annually to ensure it still aligns with your financial goals and risk tolerance. Avoid reacting to daily market fluctuations. The goal is long-term growth, not short-term trading.

Conclusion and Call to Action

Investing in funds is a powerful and accessible strategy for building wealth and securing your financial future. By pooling resources, benefiting from professional management, and leveraging diversification, funds offer a robust way to grow your money without needing to become a market expert. Understanding the different types of funds, their associated costs, and the power of compound growth will empower you to make informed decisions.

Don’t let the perceived complexity of investing deter you. Take the first step today: define your financial goals, assess your risk tolerance, and explore the vast world of investment funds. Start small, be consistent, and let time and compounding work their magic. Your future self will thank you for taking control of your financial journey now.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.