Are you tired of seeing pesky fees eat away at your hard-earned money? Imagine a world where your bank account doesn’t cost you a dime just for existing. This comprehensive guide will show you how to find and utilize free checking banking options, helping you understand the ins and outs of securing a truly free checking account. We’ll empower you to unlock the benefits of free checking banking and keep more of your money where it belongs: in your pocket. Yes, completely free checking accounts are not just a myth; they are a tangible reality that can significantly boost your financial health.

What Exactly is Free Checking Banking?

Free checking banking refers to a checking account that charges no monthly maintenance fees, no minimum balance fees, and often, no fees for standard transactions like debit card purchases or online bill pay. It’s a bank account designed to handle your everyday financial needs without chipping away at your balance through charges.

Why does this matter in real life? Imagine you are a student or someone just starting their career, perhaps earning between $1,500 and $3,000 per month. If your bank charges a typical $10-$15 monthly maintenance fee, that’s $120-$180 per year. For someone on a tight budget, this money could instead cover a utility bill, a grocery run, or contribute to savings. A truly free checking account removes this hidden drain on your finances.

Why Fees Exist: Understanding the Banking Business Model

Banks are businesses, and like any business, they need to generate revenue. Many traditional banks generate income from various fees. These can include overdraft fees, ATM fees, wire transfer fees, and the common monthly maintenance fees.

Think of it this way: a bank offers services like secure storage for your money, payment processing, and access to a network of ATMs. While some of these services are subsidized by other banking products (like loans or credit cards), many are directly paid for by customers through fees. The existence of fees often depends on a bank’s size, its operational costs, and its target customer base. Understanding this helps you see why some accounts are free and others are not.

How to Identify a Truly Free Checking Account

Finding a checking account without hidden costs requires a keen eye and diligent research. Not all “free” accounts are created equal. Here are the key steps to ensure you’re getting a genuinely no-fee experience:

- Scrutinize the Monthly Maintenance Fee: This is the most common fee. A truly free account will state “No Monthly Maintenance Fee” without conditions.

- Check for Minimum Balance Requirements: Some accounts waive fees only if you maintain a certain daily or monthly balance (e.g., $500 or $1,000). If you might dip below this, it’s not truly free for you.

- Examine Direct Deposit Requirements: Some banks offer fee waivers if you set up a direct deposit of a certain amount each month. While easy for many, it’s still a condition to be aware of.

- Look at Transaction Fees: Confirm there are no fees for standard debit card transactions, online bill pay, or electronic transfers.

- Understand ATM Policies: While most free accounts offer access to a network of free ATMs, using out-of-network ATMs often incurs a fee from both your bank and the ATM owner. Some free accounts offer ATM fee reimbursements up to a certain limit.

- Read the Fine Print: Always review the account disclosures and fee schedules carefully. These documents legally outline all potential charges.

Why this matters: Knowing these conditions prevents unexpected charges. If you only use ATMs outside your bank’s network, an account that charges $3 per out-of-network withdrawal might cost you $15 a month if you make five such transactions.

Common “Free” Checking Account Traps to Avoid

Banks are clever with their marketing. What sounds “free” might have strings attached. Here are some common pitfalls:

- “Free with e-statements” vs. “Free with paper statements”: Some banks charge for paper statements. If you prefer physical records, this could cost you.

- “Free for students” until graduation: Student accounts often become standard accounts with fees after a certain age or upon graduation. Always know the transition terms.

- “Free if you use your debit card X times”: This might lead to unnecessary spending just to meet a transaction quota.

- High Overdraft Fees: Even if there’s no monthly fee, many banks still charge hefty fees (e.g., $30-$35 per transaction) for overdrawing your account. Opt-out of overdraft protection if you’re concerned about this, or choose a bank with no overdraft fees or a grace period.

Why avoiding these traps matters: They can turn a seemingly free account into an expensive one. A single overdraft fee could wipe out months of savings from not paying a monthly maintenance fee.

The Benefits of Zero-Fee Banking

Choosing a zero-fee checking account offers several compelling advantages:

- More Money in Your Pocket: The most obvious benefit is saving money on monthly fees, which can add up significantly over time.

- Reduced Financial Stress: Without worrying about minimum balances or monthly fees, managing your money becomes simpler and less stressful.

- Better Budgeting: Predictable banking costs (or lack thereof) make it easier to stick to your budget.

- Access to Essential Services: You still get all the core functionalities of a checking account, such as direct deposit, debit card access, online bill pay, and mobile banking, without the recurring cost.

This translates to real financial empowerment. For instance, if you save $15 a month on fees, over a year that’s $180. Over five years, that’s $900. This is money you can invest, save for a down payment, or use for an emergency fund.

Practical Steps to Switch to a Free Checking Account

Making the switch doesn’t have to be complicated. Follow these steps for a smooth transition:

- Research and Compare: Look for banks and credit unions offering truly free checking. Consider online-only banks, which often have lower overheads and thus fewer fees. Check out resources like the Consumer Financial Protection Bureau (CFPB) for general guidance on banking.

- Open Your New Account: Once you’ve chosen, open the new free checking account. Many banks allow you to do this online in minutes.

- Update Direct Deposits: Change your paycheck, benefits, or any other recurring income to be deposited into your new account.

- Update Automatic Payments: Switch all recurring bill payments (utilities, subscriptions, loans, rent) from your old account to your new one. Make a list of all your recurring payments so nothing is missed.

- Monitor Both Accounts: Keep both accounts open for a few weeks, monitoring transactions to ensure all recurring deposits and payments have successfully switched.

- Close Your Old Account: Once you’re certain everything has transitioned and all checks have cleared, close your old account. Confirm in writing that the account is closed and there are no outstanding fees.

By following these steps, you minimize the risk of missed payments or late fees during the transition, ensuring a seamless move to a better banking solution.

How to Calculate Your Potential Savings

Understanding the financial impact of free checking is straightforward. It’s about totaling the fees you currently pay and realizing that money could be yours.

Here’s a simple way to estimate your savings:

- First, identify all the fees you currently pay on your existing checking account. This might include a monthly maintenance fee, out-of-network ATM fees, or fees for specific services.

- Add up these individual fees for a typical month.

- Multiply that monthly total by 12 to get your annual fee cost.

- This annual cost represents your potential savings.

For example, if you pay a $12 monthly maintenance fee and typically incur $5 in out-of-network ATM fees each month, your total monthly cost is $17. Over a year, this amounts to $204. By switching to a free checking account, you save that entire $204. This is money you can redirect to your savings, debt repayment, or investments. Many financial institutions, including the Federal Reserve, emphasize transparency in banking, making fee schedules easier to find.

Unlock Your Fee-Free Savings

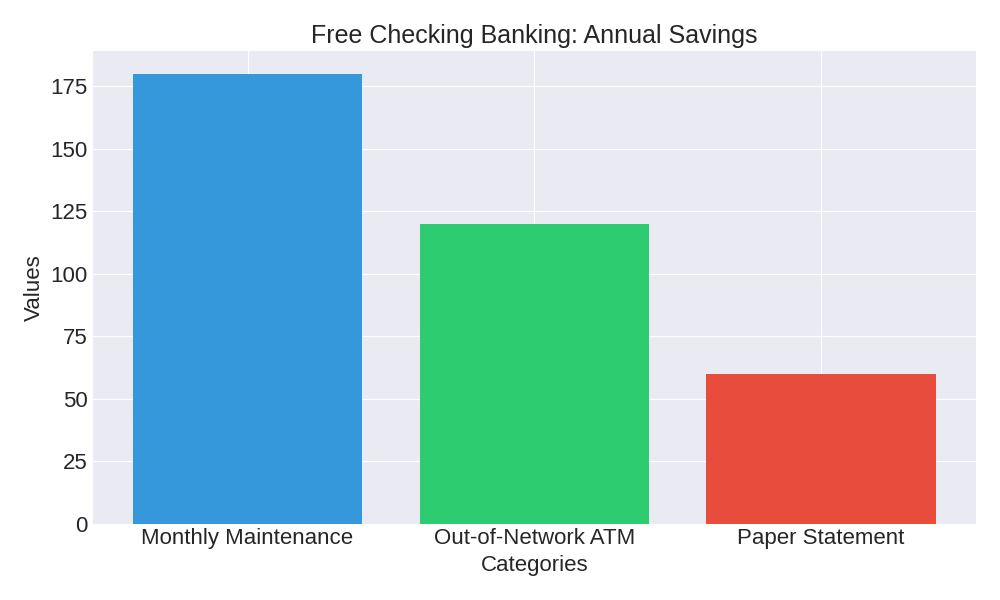

Potential Savings from Fee Elimination: A Scenario

Let’s look at how much you could save by avoiding common banking fees over time.

| Fee Type | Typical Monthly Cost | Annual Savings |

|---|---|---|

| Monthly Maintenance Fee | $10 – $15 | $120 – $180 |

| Out-of-Network ATM Fees | $5 – $10 | $60 – $120 |

| Paper Statement Fees | $3 – $5 | $36 – $60 |

| Total Potential Annual Savings | $216 – $360 |

This table illustrates how easily fees can add up. By eliminating them, you’re looking at a significant amount of money saved each year, which can be reinvested into your financial future. This kind of detailed analysis is often highlighted by financial experts, such as those covered by Reuters, discussing personal finance strategies.

Frequently Asked Questions (FAQ) About Free Checking

Q1: Are online-only banks generally better for free checking?

A1: Often, yes. Online banks typically have lower overhead costs than traditional brick-and-mortar banks, allowing them to offer more genuinely free checking accounts with fewer conditions. They also frequently provide competitive interest rates on savings.

Q2: Do credit unions offer free checking?

A2: Absolutely. Credit unions are member-owned, not-for-profit institutions, and they often offer very competitive terms, including free checking accounts with minimal or no conditions. They are a great alternative to traditional banks.

Q3: What if I accidentally overdraw a “free” checking account?

A3: Even free checking accounts can charge overdraft fees if you spend more money than you have in your account. You can often opt out of overdraft protection, which means your card will simply be declined if you try to spend money you don’t have, preventing a fee. Always understand your bank’s overdraft policy.

Q4: Will a free checking account hurt my credit score?

A4: No, a checking account itself does not directly impact your credit score. Credit scores are primarily influenced by borrowing activities like credit cards, loans, and mortgages. However, poor management, like repeated overdrafts leading to collection efforts, could indirectly affect your banking relationships.

Conclusion

Securing a free checking banking account is a smart financial move that puts more money back into your hands. By understanding how banks operate, carefully scrutinizing account terms, and being aware of potential traps, you can navigate the banking landscape to your advantage. The savings from avoiding fees can significantly contribute to your financial goals, whether it’s building an emergency fund, saving for a down payment, or simply having more disposable income.

Take Action Now: Don’t let unnecessary fees erode your hard-earned money. Start researching free checking options today. Compare offers from online banks and credit unions, read the fine print, and make the switch. Your wallet will thank you!

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.