Choosing the best banks for online banking is a pivotal financial decision in today’s digital age. It’s not just about convenience; it’s about finding a financial partner that aligns with your specific needs, offers superior technology, and provides competitive benefits. This guide, crafted by an expert financial analyst and educator, will cut through the noise, explaining complex concepts simply while maintaining depth. Our goal is to equip you with the knowledge to confidently pick your ideal online banking solution.

In summary: The best online banks offer a compelling blend of low (or no) fees, high-interest rates on savings, robust mobile apps, and top-tier security. Your ideal fit depends on your banking habits, whether you need frequent ATM access, direct deposit flexibility, or advanced budgeting tools. Prioritize institutions with FDIC insurance and responsive customer support for peace of mind.

Why Choose Online Banking? The Core Advantages

Many people wonder if ditching traditional brick-and-mortar banks for online-only options is worth it. The answer for many is a resounding yes, primarily due to inherent structural advantages that online banks possess.

Convenience & Accessibility

Online banks operate 24/7 from anywhere with an internet connection. This means you can manage your finances on your schedule, not the bank’s. Imagine you’re traveling overseas and need to transfer funds urgently; with online banking, you can do it from your hotel room at midnight without worrying about time zones or bank holidays. This flexibility is a game-changer for busy individuals or those who travel frequently.

Why this matters in real life: You save significant time and effort by eliminating trips to a physical branch, making financial management less of a chore and more integrated into your daily life.

Lower Fees & Better Rates

Without the overhead costs of maintaining numerous physical branches, online banks can pass those savings on to their customers. This often translates into lower fees, such as no monthly maintenance fees, no foreign transaction fees, or fewer ATM fees. Crucially, they typically offer significantly higher interest rates on savings accounts compared to traditional banks.

Scenario: Consider two individuals, both with $10,000 in a savings account. One uses a traditional bank offering 0.05% APY, while the other uses an online bank offering 1.50% APY. After a year, the traditional bank saver earns $5, while the online bank saver earns $150. Over time, this difference, especially with compounding, becomes substantial. This is why comparing the best banks for online banking often highlights their superior earning potential.

Key Features to Look for in the Best Online Banks

When evaluating potential online banks, don’t just look at interest rates. A holistic view of their features will ensure a smooth and secure banking experience.

Strong Mobile App & User Experience

A bank’s mobile app is its primary interface. It should be intuitive, fast, and offer comprehensive functionality. This includes easy access to account balances, mobile check deposit, bill pay, funds transfers, and even budgeting tools. A clunky app can quickly make online banking frustrating.

Real-life example: You’re splitting a dinner bill with friends. A great banking app allows you to instantly send your share to another person via Zelle or Venmo (if integrated), or easily transfer funds to their account, all within a few taps. A poor app might require logging into a separate website or making multiple clicks, adding unnecessary friction.

Security & FDIC Insurance

Security should be paramount. Ensure your chosen online bank utilizes robust encryption, multi-factor authentication, and fraud monitoring. Critically, verify that the bank is FDIC insured. This means your deposits are protected up to at least $250,000 per depositor, per insured bank, for each account ownership category. This federal guarantee ensures your money is safe, even if the bank were to fail. For more details on this vital protection, visit the official FDIC website.

Why this matters: FDIC insurance isn’t just a regulatory checkbox; it’s a shield that protects your hard-earned money from unforeseen economic events or bank failures, offering peace of mind.

Customer Service

Even in a digital world, you might need human assistance. Look for banks offering 24/7 customer support via phone, chat, or email. Some even offer video calls. Test their responsiveness before fully committing.

ATM Access & Deposit Options

While online, you’ll still need to access cash or deposit physical checks/cash occasionally. Many online banks partner with large ATM networks (like Allpoint or MoneyPass) or offer ATM fee reimbursements. For cash deposits, options might include depositing at partner retail locations, using money orders, or making an electronic transfer from another bank.

How to Choose Your Ideal Online Bank: A Step-by-Step Guide

Picking the right online bank doesn’t have to be overwhelming. Follow these steps to narrow down your choices and find a perfect match.

- Assess Your Needs: Start by understanding your banking habits. Do you primarily use direct deposit and debit card transactions? Do you need a high-yield savings account? How often do you need to deposit cash or withdraw from an ATM?

- Compare Fees and Rates: Look for banks with no monthly maintenance fees. Compare the Annual Percentage Yield (APY) on savings and checking accounts. Even small differences can add up over time.

- Evaluate Technology: Download and explore the bank’s mobile app. Read user reviews on app stores. A user-friendly interface for transfers, bill pay, and mobile deposits is crucial for a smooth experience.

- Check Security & Support: Confirm FDIC insurance. Review their security features. Understand their customer support options and hours. Are they available when you might need them?

Mini Case Study: Sarah, a freelancer earning between $4,000-$6,000 monthly, prioritizes high-yield savings for her emergency fund and easy invoicing payments. She rarely uses cash. She opted for an online bank with a top-rated mobile app, 1.75% APY on savings, and robust integration with payment platforms. John, a small business owner, needs frequent cash deposits. He chose an online bank with a strong ATM network that allows cash deposits at partner retailers and offers business checking accounts. Their distinct needs led them to different ideal choices among the best banks for online banking.

Understanding Interest: A “How to Calculate” Guide

Interest is the cost of borrowing money or the reward for lending (saving) it. For savings accounts, it’s the money the bank pays you for keeping your funds with them. Understanding how it works helps you maximize your earnings.

To calculate simple interest on your savings for a short period, you multiply your initial deposit by the interest rate, and then by the amount of time your money is in the account (usually expressed as a fraction of a year). For example, if you have $1,000 in an account with a 1% annual interest rate, you would earn $10 over a full year ($1,000 * 0.01 = $10). If it’s only for half a year, you’d earn $5.

However, most savings accounts offer compound interest, meaning you earn interest not just on your initial deposit, but also on the accumulated interest from previous periods. This is a powerful concept for growing your wealth over time. The bank calculates interest periodically (daily, monthly, or quarterly) and adds it to your principal, then the next period’s interest is calculated on that new, larger sum. This process makes your money grow faster.

Why compound interest matters in real life: It’s often called the “eighth wonder of the world” because it allows your money to grow exponentially. Small, consistent savings, combined with a good interest rate, can lead to substantial wealth accumulation over decades. It’s the engine behind long-term investing and why starting to save early is so beneficial.

The Best Banks for Online Banking: Savings & Growth Calculator

Long-Term Impact: Compound Growth Scenario

To illustrate the power of compound interest, let’s look at a hypothetical scenario where you deposit a fixed amount monthly into a savings account with a competitive interest rate. This table shows how your money could grow over time, assuming an average monthly contribution of $200 and an average annual interest rate of 1.5% (compounded monthly). Please note, these are illustrative example numbers only and not factual guarantees.

| Time Horizon | Total Deposits (Illustrative) | Total Interest Earned (Illustrative) | Total Account Value (Illustrative) |

|---|---|---|---|

| After 5 Years | ~$12,000 | ~$450 – $550 | ~$12,450 – $12,550 |

| After 10 Years | ~$24,000 | ~$2,000 – $2,500 | ~$26,000 – $26,500 |

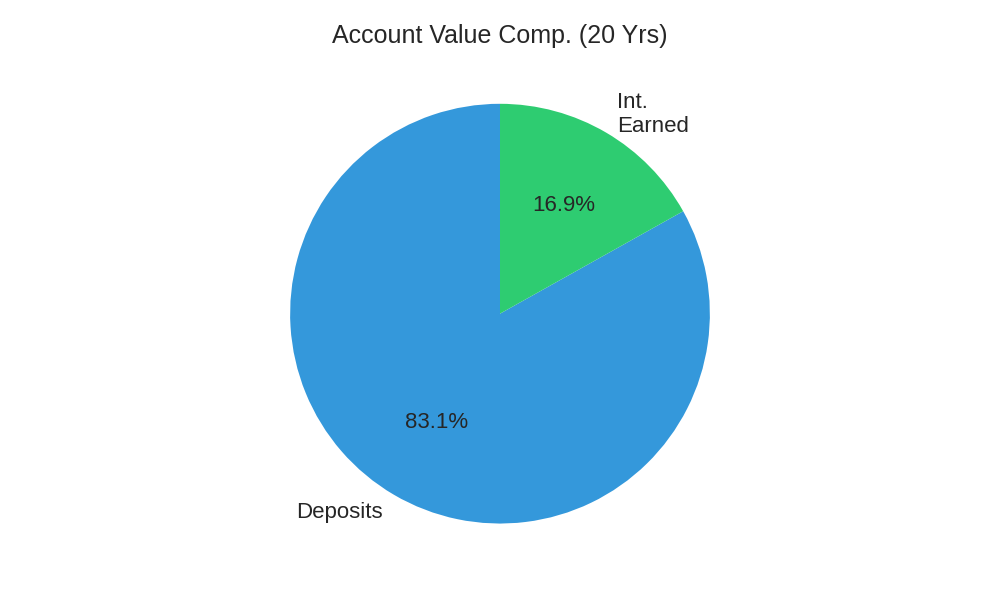

| After 20 Years | ~$48,000 | ~$9,000 – $10,500 | ~$57,000 – $58,500 |

This table clearly demonstrates how the interest earned grows significantly over time, becoming a larger portion of your total account value as the years pass. This is the magic of compounding in action.

Frequently Asked Questions (FAQ)

Are online banks safe?

- Yes, absolutely. Reputable online banks are just as safe as traditional banks, often employing advanced digital security measures. The critical factor is ensuring they are FDIC insured, which protects your deposits up to $250,000 per depositor. Always check for this.

Can I deposit cash with an online bank?

- Cash deposits can be trickier with online-only banks. Some offer solutions like depositing cash at partner retail locations (e.g., specific grocery stores or pharmacies) or converting cash to a money order and depositing it via mobile check deposit. It’s an important consideration if you frequently handle cash.

What if I need in-person help?

- This is a trade-off for the benefits of online banking. Online banks do not have physical branches. However, their customer service is typically robust, offering 24/7 phone, chat, or email support. For complex issues, some even offer video calls.

Are the interest rates really better with online banks?

- Generally, yes. Due to lower operating costs (no physical branches), online banks can afford to offer more competitive interest rates on savings accounts and certificates of deposit (CDs) compared to many traditional banks. This can lead to significantly more earnings over time.

Conclusion

Choosing among the best banks for online banking means prioritizing convenience, lower fees, and potentially higher returns on your savings. By carefully evaluating your personal financial needs, scrutinizing mobile app functionality, confirming FDIC insurance, and understanding customer support options, you can find an online bank that perfectly complements your lifestyle.

The digital banking landscape offers incredible flexibility and advantages. Take the time to research, compare, and select a financial institution that will empower your financial journey. Don’t settle for less when it comes to your money.

Call to Action: Start exploring online banking options today! Visit the websites of highly-rated online banks, compare their offerings against your needs, and take the first step towards a more efficient and rewarding banking experience.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.