Imagine this nightmare scenario: You’ve just financed a new car, excited about the open road. A few months later, disaster strikes – your car is totaled in an accident that wasn’t your fault. You expect your auto insurance to cover it, but then the shock hits: The insurance company pays out far less than you still owe on your loan. This isn’t just a hypothetical; it’s a common, financially devastating reality for many drivers. This is precisely where gap insurance steps in, acting as your financial shield.

You’re left with no car, and worse, a significant debt you still have to pay, even though the vehicle is gone. This “gap” between what your car is worth and what you owe can easily amount to thousands of dollars. As a financial strategist and consumer advocate, I’m here to tell you that ignoring this risk is a critical mistake. Understanding gap insurance isn’t just smart; it’s essential for protecting your financial stability when you finance a vehicle.

The Financial Trap: When Your Car Is Worth Less Than You Owe

Many new car buyers get caught in a vicious financial cycle without even realizing it. The moment you drive a new car off the lot, it begins to lose value – a process known as depreciation. This depreciation often happens much faster than you pay down your car loan, especially in the first few years. In a typical scenario, a brand-new car can lose between 20% to 30% of its value in the first year alone. This rapid depreciation creates a significant “gap.”

Why does this matter in real life? Imagine you finance a $30,000 car with a small down payment, say $1,000. Your loan balance starts at $29,000. Six months later, if that car is totaled, your standard auto insurance policy (collision and comprehensive) will only pay out its actual cash value (ACV) at the time of the loss. Due to depreciation, its ACV might now be only $22,000. If you still owe $28,000 on the loan, you’re suddenly on the hook for the remaining $6,000 out of pocket. This isn’t just an inconvenience; it’s a direct hit to your savings or worse, it forces you into new debt.

How Gap Insurance Works: Closing the Critical Payment Gap

Gap insurance, or Guaranteed Asset Protection insurance, is designed specifically to cover this financial shortfall. It’s an optional add-on to your standard auto policy that pays the difference between your car’s actual cash value (ACV) and the remaining balance on your auto loan or lease, in the event your vehicle is declared a total loss due to accident or theft. It essentially ensures you don’t owe money on a car you no longer own.

Think of it as peace of mind for your car loan. When your primary insurer settles your claim for the ACV, gap insurance kicks in to cover the rest of what you owe to the lender. This can include your deductible in some cases, further alleviating your financial burden. It’s a vital safety net, especially with today’s longer loan terms and higher vehicle prices. For more general information on auto insurance, you can visit a reputable consumer resource like The Federal Trade Commission.

Calculating Your Potential Gap (No Complex Math)

Understanding your potential gap doesn’t require complex formulas, just a basic awareness of your car’s value and loan balance. You can estimate this simply:

- Step 1: Determine Your Estimated Loan Payoff. Contact your lender for your exact current payoff amount.

- Step 2: Estimate Your Car’s Current Actual Cash Value (ACV). Use online valuation tools like Kelley Blue Book (KBB.com) or NADAguides to get an approximate trade-in or private party value for your specific make, model, year, mileage, and condition.

- Step 3: Subtract ACV from Loan Payoff. If your loan payoff is higher than the ACV, that difference is your potential gap.

For example, if your loan payoff is $25,000 and your car’s ACV is $20,000, your potential gap is $5,000. This is the amount gap insurance would cover. Remember, this is an estimate, but it gives you a clear picture of the risk.

How Much Could Gap Insurance Save You?

Who Truly Needs Gap Insurance? Spotting the Red Flags

While gap insurance is beneficial for many, it’s not universally necessary. You likely need gap insurance if any of these situations apply to you:

- You made a small down payment (less than 20%). A smaller down payment means you’re financing more of the car’s initial cost, increasing the likelihood of owing more than it’s worth early on.

- You chose a long loan term (60 months or more). Longer terms mean slower equity build-up, leaving you “upside down” for a longer period.

- You leased your vehicle. Most lease agreements require gap insurance, and it’s often rolled into the lease payment.

- Your car depreciates quickly. Some car models lose value faster than others. Research your specific vehicle’s depreciation rate.

- You rolled negative equity from a previous car into your new loan. This immediately puts you in a significant “upside down” position.

Common Myths to Avoid

- “My regular insurance will cover everything.” No, standard collision and comprehensive only cover ACV, not your loan balance. This is the biggest misconception.

- “I’m a good driver, so I won’t need it.” Accidents happen, and cars get stolen. Your driving skill doesn’t protect you from external risks.

- “Gap insurance is always expensive.” The cost is typically a small percentage of your overall premium, often between $20-$60 per year from an insurer, or a one-time fee of a few hundred dollars from a dealer.

Where to Buy Gap Insurance and What to Watch Out For

You have a few options when it comes to purchasing gap insurance, and your choice can significantly impact the cost and terms:

- Your Auto Insurance Company: Often the most affordable option, adding gap coverage to your existing policy. It typically costs less this way, sometimes just a few dollars a month.

- Car Dealership: Dealers will offer gap insurance when you finalize your financing. While convenient, it’s often significantly more expensive, sometimes marked up by hundreds or even thousands of dollars, and rolled into your loan, meaning you pay interest on it.

- Your Bank or Credit Union: Many financial institutions that offer auto loans also provide gap coverage. This can sometimes be a competitive option.

Insider Tip: Always get quotes from your current auto insurer first before considering a dealer’s offer. The difference in price can be substantial. Also, be wary of aggressive sales tactics at the dealership that push gap insurance as a mandatory add-on; in most cases, it is not.

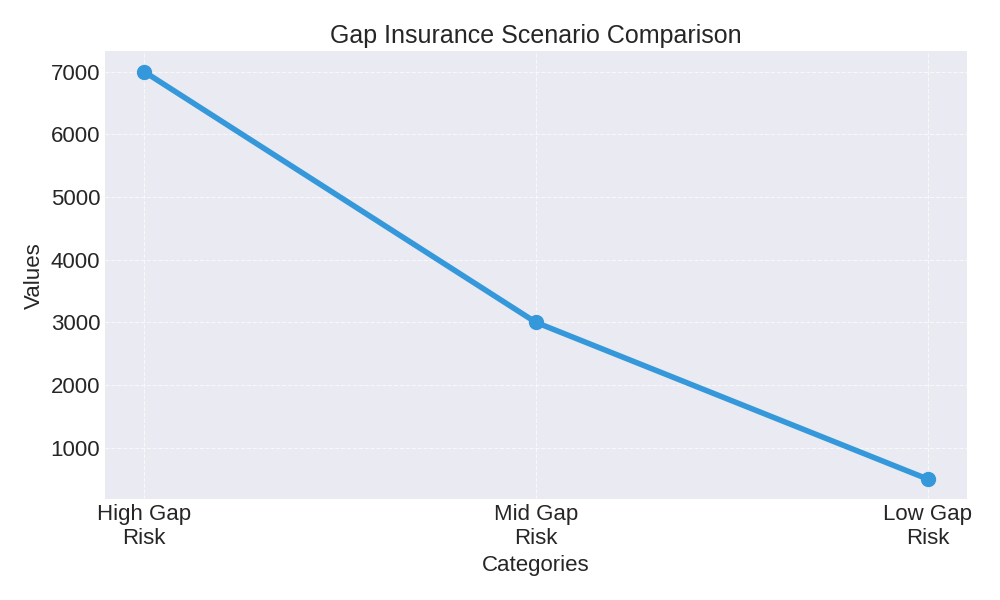

Here’s a comparison of typical gap insurance scenarios:

| Scenario Detail | Original Loan Amount | Loan Balance After 1 Year | Car ACV After 1 Year (Totaled) | Insurance Payout (ACV) | Remaining Loan Balance | Gap Insurance Pays | Out-of-Pocket Cost (Without Gap) |

|---|---|---|---|---|---|---|---|

| High Depreciation, Low Down Payment | $30,000 | $27,000 | $20,000 | $20,000 | $7,000 | $7,000 | $7,000 |

| Moderate Depreciation, Medium Down Payment | $25,000 | $22,000 | $19,000 | $19,000 | $3,000 | $3,000 | $3,000 |

| Low Depreciation, High Down Payment | $20,000 | $17,000 | $16,500 | $16,500 | $500 | $500 | $500 |

This table clearly illustrates how gap insurance protects you from substantial out-of-pocket expenses when your car is totaled and its value falls below your loan balance. For more insights on car buying strategies, you might find valuable resources from financial authorities like Investor.gov.

Smart Strategies: How to Potentially Avoid Gap Insurance

While gap insurance is a valuable safety net, there are ways to structure your auto purchase and financing to potentially avoid needing it altogether:

- Make a Larger Down Payment: Aim for 20% or more. This immediately reduces your loan principal and helps you build equity faster, reducing the risk of being upside down.

- Choose a Shorter Loan Term: A 36-month or 48-month loan term means higher monthly payments but you’ll pay off the car faster and reduce the period during which you’re at risk.

- Buy a Used Car: Used cars have already gone through their steepest depreciation curve. While they still lose value, the rate is often much slower than new vehicles, minimizing the gap risk.

- Don’t Roll Over Negative Equity: If you owe money on your trade-in, pay it off before purchasing a new car, or at least ensure you make a substantial down payment on the new vehicle to cover that negative equity.

- Accelerate Loan Payments: If you can afford it, pay a little extra each month towards your principal. This helps you build equity faster and reduces your loan balance more quickly.

Conclusion: Protect Your Financial Future Today

The thought of losing your car and still owing thousands of dollars is a daunting one. Gap insurance is a relatively inexpensive product that offers profound financial protection, ensuring that an unforeseen accident doesn’t leave you in a devastating financial hole. As a consumer advocate, I urge you to proactively assess your risk when financing a vehicle.

Don’t wait for a crisis to understand your coverage. Review your current auto loan and insurance policy. If you’ve got a low down payment, a long loan term, or negative equity, exploring gap insurance is not just an option—it’s a critical financial move. Take control of your financial future and make an informed decision today to secure your investment.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.