Dreaming of owning a home but dreading the complex mortgage process? You’re not alone. Navigating the world of home financing can feel overwhelming, but modern solutions like an online mortgage bank are transforming the experience. This comprehensive guide will demystify the process, helping you achieve stress-free home financing.

An online mortgage bank streamlines the entire home loan journey, from application to closing, leveraging digital technology. This approach often translates to greater efficiency, competitive rates, and a user-friendly experience compared to traditional brick-and-mortar lenders. We’ll explore how these digital platforms work, their unique advantages, and how you can confidently secure your next home loan.

What is an Online Mortgage Bank and Why Consider One?

An online mortgage bank is a financial institution that originates and services home loans entirely through digital channels. Unlike traditional banks with physical branches, these lenders operate primarily online, offering a convenient, accessible, and often more cost-effective way to secure a mortgage.

Why does this matter in real life? Imagine you’re a busy professional with limited time during standard banking hours. An online mortgage bank allows you to apply, upload documents, and communicate with loan officers on your schedule, 24/7. This flexibility means you can manage your application from the comfort of your home, after work, or even during a weekend, fitting it seamlessly into your life.

The Digital Advantage: Accessibility and Efficiency

The core appeal of an online mortgage bank lies in its ability to offer a highly efficient and often more competitive service. Their lower operational overhead, without the costs of physical branches, can translate into better interest rates and fewer fees for borrowers.

For example, if you’re comparing two loan offers for a $300,000 mortgage, an online lender might offer an interest rate that is 0.125% to 0.250% lower. Over a 30-year term, this seemingly small difference can save you tens of thousands of dollars in interest, making your home ownership more affordable. It’s about maximizing your savings through a streamlined process.

The Benefits of Choosing an Online Mortgage Bank

Opting for an online lender offers several distinct advantages that can significantly enhance your home financing experience. These benefits go beyond just convenience, impacting your bottom line and overall satisfaction.

- Competitive Interest Rates: Due to reduced overhead, online lenders can often pass savings onto consumers through lower interest rates and fees. This makes your mortgage more affordable over its lifespan.

- Streamlined Application Process: Digital platforms allow for quick form completion, secure document uploads, and efficient communication. This drastically cuts down on paperwork and processing time.

- 24/7 Accessibility: You can apply and manage your loan application at any time, from anywhere, fitting it around your personal and professional commitments. This flexibility is a huge advantage for many homeowners.

- Transparency and Tools: Many online platforms offer powerful tools for comparing loan options, estimating payments, and tracking application progress in real-time. This empowers you to make informed decisions.

Consider a scenario where a first-time homebuyer is comparing offers. They receive a quote from a traditional bank requiring multiple in-person meetings and physical document submissions, and another from an online mortgage bank. The online option provides an instant rate quote, a clear breakdown of closing costs, and a dedicated portal to track everything. The efficiency and transparency of the online option often win out.

Navigating the Online Mortgage Application Process

While the process is digital, the fundamental steps to securing a mortgage remain similar. Understanding these stages will help you prepare and move through your application with confidence.

- Pre-qualification vs. Pre-approval: Start with pre-qualification for an estimate of what you might afford, then aim for pre-approval. Pre-approval involves a more thorough financial review, including a credit check, and gives you a conditional commitment for a loan amount. This makes your offer more attractive to sellers.

- Gathering Your Documents: Online lenders will require various documents, typically including pay stubs, W-2s, tax returns, bank statements, and investment account statements. Having these ready digitally will significantly speed up your application.

- Choosing Your Loan Product: Research different mortgage types such as fixed-rate (predictable monthly payments) or adjustable-rate mortgages (ARMs) (payments can change over time), and decide what fits your financial plan best.

- Application Submission: Complete the online application form, carefully inputting all required information. Be thorough and accurate to avoid delays.

- Underwriting and Closing: Once submitted, your application goes through underwriting, where your financial information is verified. After approval, you’ll proceed to closing, where all legal documents are signed, and the home officially becomes yours.

Why does this matter in real life? Being pre-approved strengthens your bargaining position. Imagine you find your dream home. With pre-approval, you can submit an offer confidently, knowing you have financing lined up, often giving you an edge over other buyers who are not yet approved.

Key Factors to Consider When Selecting an Online Mortgage Bank

Not all online lenders are created equal. Due diligence is crucial to ensure you choose a reputable and suitable partner for your home financing.

- Interest Rates and Annual Percentage Rate (APR): Look beyond just the interest rate. The APR (Annual Percentage Rate) includes interest and certain fees, giving you a more accurate picture of the total cost of borrowing. Compare APRs across multiple lenders.

- Fees and Closing Costs: Scrutinize all potential fees, including origination fees, appraisal fees, and credit report fees. These can add up significantly to your total closing costs.

- Customer Service and Support: While online, you’ll still interact with people. Check reviews for responsiveness, helpfulness, and expertise of their loan officers. A good experience means a less stressful process.

- Loan Products Offered: Ensure the online bank offers the specific type of mortgage you need (e.g., FHA, VA, USDA, Jumbo, conventional). Not all lenders offer the full spectrum of products.

- Reputation and Reviews: Check independent review sites and the Better Business Bureau. A lender with a strong, positive reputation indicates reliability and trustworthiness.

For example, if an online lender offers a slightly lower interest rate but has higher origination fees, its overall APR might be comparable or even higher than another lender. It’s crucial to compare the full financial picture, not just one number. This ensures you’re making a truly informed decision about your loan’s true cost.

Understanding Mortgage Costs: Beyond the Interest Rate

The monthly principal and interest payment is just one piece of the puzzle. Several other costs contribute to the overall expense of homeownership.

Closing Costs

These are fees paid at the closing of a real estate transaction. They typically range from 2% to 5% of the loan amount and include items like title insurance, attorney fees, appraisal fees, and recording fees. Closing costs are a significant upfront expense to budget for.

Escrow Accounts

Many mortgages require an escrow account to hold funds for property taxes and homeowner’s insurance. A portion of your monthly payment goes into this account, ensuring these critical expenses are paid on time. This simplifies budgeting for recurring costs.

Private Mortgage Insurance (PMI)

If your down payment is less than 20% of the home’s purchase price, most lenders will require Private Mortgage Insurance (PMI). This protects the lender if you default on the loan. PMI adds to your monthly payment, but can often be removed once you build sufficient equity.

How to Calculate Your Total Mortgage Cost (Plain Language)

Calculating the total cost of your mortgage helps you understand the long-term financial commitment. Here’s a simplified way to think about it:

First, figure out your monthly principal and interest payment. Many online calculators can do this if you input your loan amount, interest rate, and loan term (e.g., 30 years).

Next, add estimates for your monthly property taxes, homeowner’s insurance, and if applicable, Private Mortgage Insurance (PMI). These will vary based on your home’s value and location.

Then, multiply your total estimated monthly payment by the number of months in your loan term (e.g., 360 months for a 30-year loan). This gives you a good estimate of the total amount you will pay over the life of the loan, not including upfront closing costs.

Finally, remember to factor in the closing costs you pay upfront. These are typically a percentage of your loan amount, paid when you finalize the home purchase. Adding these upfront costs to your total estimated payback gives you a comprehensive picture.

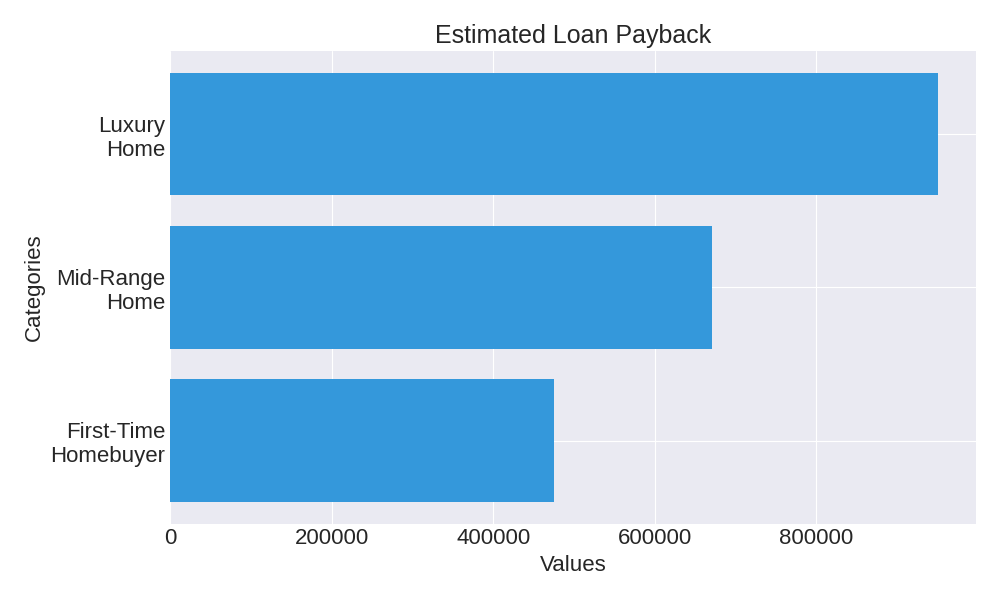

Online Mortgage Bank Stress-Free Home Financing: Interest Cost Estimator

| Loan Scenario | Estimated Loan Amount | Approximate Interest Paid (30-yr term) | Estimated Total Payback (P&I Only) |

|---|---|---|---|

| First-Time Homebuyer (Avg. 5% down) | $250,000 – $350,000 | $225,000 – $375,000 | $475,000 – $725,000 |

| Mid-Range Home (Avg. 10% down) | $350,000 – $500,000 | $320,000 – $550,000 | $670,000 – $1,050,000 |

| Luxury Home (Avg. 20% down) | $500,000 – $750,000 | $450,000 – $825,000 | $950,000 – $1,575,000 |

*Example figures are illustrative and do not include property taxes, insurance, or closing costs. Actual figures will vary significantly based on interest rate, loan term, and individual financial circumstances.

FAQ: Common Questions About Online Mortgage Banks

Q1: Are online mortgage banks safe and secure?

Yes, reputable online mortgage banks use advanced encryption and security protocols to protect your personal and financial information. They are regulated just like traditional banks. Always look for secure website connections (HTTPS) and read reviews.

Q2: Can I get personalized advice from an online lender?

Absolutely. Most online lenders provide dedicated loan officers or financial advisors who can guide you through the process, answer questions, and help you choose the best loan product for your needs. Communication often happens via phone, email, or video calls.

Q3: What if I prefer to talk to someone in person?

While the process is online, you’re not entirely isolated. Online lenders have teams of customer service representatives and loan officers available remotely. If you strongly prefer face-to-face interaction for all stages, a traditional bank might be a better fit, but consider the convenience trade-off.

Q4: Do online lenders offer the same range of products as traditional banks?

Many online lenders offer a comprehensive suite of loan products, including conventional, FHA, VA, and jumbo loans. However, it’s always wise to check their specific offerings to ensure they meet your particular needs.

Conclusion: Your Path to Stress-Free Home Financing

The landscape of home financing has evolved, and the online mortgage bank stands out as a powerful, efficient, and often more affordable option for homebuyers. By understanding the benefits, navigating the digital application process, and carefully considering all costs, you can unlock a truly stress-free path to owning your dream home.

Ready to explore your options? Research reputable online mortgage banks, compare their offerings, and take the first step towards securing your home loan with confidence. Your financial future awaits.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.