Let’s be blunt: You need a car, but your credit score feels like a brick wall. You’ve probably faced rejection, heard vague apologies about “lender criteria,” or been offered interest rates that make your jaw drop. It’s frustrating, and it feels like the system is rigged against you.

But here’s the unvarnished truth: getting a car loan on bad credit is absolutely possible. You just need a smarter strategy, a bit of grit, and the right insider knowledge. Don’t let past financial missteps define your present transportation needs or your future potential. This isn’t about magic; it’s about making informed, strategic moves.

Many people believe that a poor credit score automatically disqualifies them from responsible lending. That’s a myth. Lenders are in the business of lending, and while they assess risk, many specialize in helping individuals just like you secure a car loan on bad credit. The goal isn’t just to get a car; it’s to get one on terms you can manage, and ideally, that helps rebuild your financial standing.

Why Your Credit Score Feels Like a Roadblock (And Why It Isn’t Always)

You’re right, your credit score plays a huge role. A lower score typically means higher interest rates and fewer loan options. Lenders see you as a higher risk, so they charge more to offset that risk. This can make a seemingly affordable car suddenly appear out of reach.

Imagine you’ve landed a new job that requires a reliable commute, but your credit score is in the 550 range. Many traditional banks might decline your application outright. It feels like a catch-22: you need the job to make money, but you need a car to get to the job, and your credit is standing in the way.

Insider Tip: Your credit score isn’t a permanent tattoo. It’s a snapshot in time. Lenders who specialize in bad credit car loans often look beyond just the number. They consider your current income, employment stability, and your ability to make a down payment. This holistic view is crucial for your success.

Why this matters in real life: Understanding that lenders have different criteria means you shouldn’t waste time applying to lenders who only approve “prime” borrowers. Instead, you can focus your energy on those who are equipped and willing to work with your credit profile.

Strategic Steps to Secure Your Car Loan (Even With Bad Credit)

Step 1: Know Your Score and Your Report

Before you even think about looking at cars, pull your credit report. You have a right to a free report from each of the three major credit bureaus annually. Visit AnnualCreditReport.com to get yours.

Pro Tip: Check for errors. Mistakes on your credit report are surprisingly common and can drag your score down unfairly. Dispute any inaccuracies immediately. Even a small improvement in your score can lead to better loan terms.

Why this matters in real life: Knowing what lenders see puts you in a position of power. You can address issues or explain legitimate concerns upfront, rather than being surprised by a rejection.

Step 2: Set a Realistic Budget (Beyond the Monthly Payment)

This is where many people with bad credit make a critical mistake. They focus solely on the monthly payment. While important, it doesn’t tell the whole story of a car’s true cost.

Common Myth to Avoid: Thinking a low monthly payment over a very long term (like 72 or 84 months) is always the best deal. Often, this means you’ll pay significantly more in total interest.

A realistic budget includes the car’s purchase price, interest, taxes, insurance, registration, and ongoing maintenance. Imagine you’re approved for a $15,000 loan. A 15% interest rate over 60 months will cost you far more in total than a 10% rate over 48 months, even if the monthly payments seem similar initially.

Why this matters in real life: Overextending yourself on a car loan can lead to financial strain, making it harder to make timely payments and rebuild your credit. Your goal is sustainable transportation, not just a temporary fix.

Step 3: Explore Financing Options for Bad Credit

Not all lenders are created equal, especially when it comes to bad credit. You have options, and knowing them is key.

- Dealership Financing (Subprime Departments or “Buy Here, Pay Here”): Many dealerships have relationships with multiple lenders, including those who specialize in subprime (bad credit) loans. “Buy Here, Pay Here” (BHPH) lots are direct lenders, meaning the dealership is the lender.

- Online Lenders & Aggregators: Companies like LendingTree or specialized bad credit auto loan providers can connect you with multiple lenders who might approve your application.

- Credit Unions: Often more willing to work with members, even those with less-than-perfect credit, and can sometimes offer better rates than traditional banks.

Pro/Con Analysis:

- Buy Here, Pay Here (BHPH):

- Pros: Easiest approval, quick turnaround.

- Cons: Very high interest rates (often the maximum allowed by law), limited vehicle selection, may not report payments to all credit bureaus (which defeats the credit-building purpose).

- Credit Unions/Online Lenders/Dealership Subprime:

- Pros: Potentially better rates than BHPH, more transparency, wider vehicle selection, consistent reporting to credit bureaus (crucial for rebuilding credit).

- Cons: Stricter approval requirements than BHPH, may still have higher rates than prime loans.

Why this matters in real life: Shopping around means you’re more likely to find a competitive rate and terms that suit your budget, rather than being stuck with the first (and potentially most expensive) offer you receive.

Step 4: The Power of a Down Payment and Co-Signer

Even with bad credit, these two elements can significantly improve your chances and your loan terms.

- Down Payment: Putting money down reduces the amount you need to borrow. This lowers the lender’s risk, making them more likely to approve you and potentially offer a better interest rate. A larger down payment also reduces your monthly payments and the total interest you’ll pay over the life of the loan.

- Co-Signer: If you have a trusted friend or family member with good credit willing to co-sign, it can dramatically boost your approval odds and secure a lower interest rate. Their good credit effectively “backs” your loan.

Mini Case Study: Imagine you need a $15,000 car. With bad credit and no down payment, you might be offered 20% APR. If you can put $3,000 down, reducing the loan to $12,000, and perhaps secure a co-signer, you might get an offer for 12% APR. This difference can save you thousands of dollars over the loan term.

Why this matters in real life: These aren’t just arbitrary suggestions; they are concrete actions that directly translate into lower costs and higher approval rates for your car loan on bad credit.

Calculating the True Cost of Your Bad Credit Car Loan

Understanding the actual total cost of your car loan, especially with higher interest rates, is essential. Don’t just look at the monthly payment; calculate the full price you’ll pay.

Here’s a practical way to think about it: Start with the amount you need to borrow. Multiply that by your interest rate over the number of years you’ll be paying. The longer the loan term, the more interest you’re likely to pay in total, even if each monthly payment is smaller. For example, a $10,000 loan at 18% interest over 5 years will cost you significantly more in total than the same loan at 12% interest over 3 years.

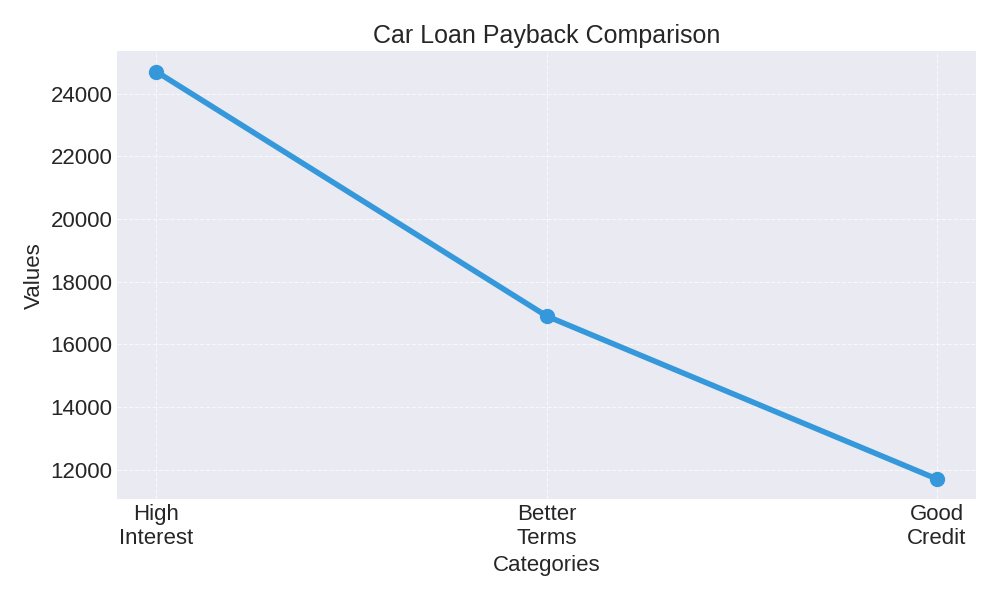

| Loan Scenario | Loan Amount | Interest Rate (APR) | Loan Term (Months) | Estimated Interest Paid | Estimated Total Payback |

|---|---|---|---|---|---|

| Bad Credit (High Interest, Long Term) | $15,000 | 18% | 72 | ~$9,700 | ~$24,700 |

| Bad Credit (Better Terms w/ Down Payment) | $12,000 | 15% | 60 | ~$4,900 | ~$16,900 |

| Improved Credit (Lower Interest, Shorter Term) | $10,000 | 8% | 48 | ~$1,700 | ~$11,700 |

Why this matters in real life: This table clearly shows that even small changes in your loan amount, interest rate, or term can lead to thousands of dollars in savings. Understanding these numbers empowers you to negotiate and make smarter choices, even with bad credit.

Yes, You Can Get a Car Loan on Bad Credit

Insider Tips & Common Myths to Avoid When Getting a Car Loan on Bad Credit

- Myth 1: You have to accept the first offer.

Insider Tip: Never settle for the first loan offer. Get pre-approved by a few lenders before you even visit a dealership. This gives you leverage and a benchmark. Shopping for a car loan within a short window (typically 14-45 days) counts as a single inquiry on your credit report, so don’t be afraid to compare.

- Myth 2: Any car will do as long as it gets me a loan.

Insider Tip: Don’t buy more car than you need or can truly afford. A reliable, affordable used car is often a much wiser choice than an expensive new one when you’re working with bad credit. Remember, you’re also paying for insurance, fuel, and maintenance.

- Myth 3: Bad credit means you can’t negotiate.

Insider Tip: Always negotiate the car’s purchase price separately from the financing terms. Don’t let a dealer roll them together into one confusing monthly payment. Negotiate the best price for the vehicle first, then discuss your financing options.

- Pro Tip: If possible, consider a slightly shorter loan term, even if it means a marginally higher monthly payment. You’ll save a substantial amount on interest over the long run, and you’ll pay off the car faster, reducing the risk of being “underwater” (owing more than the car is worth).

Your Car Loan as a Credit-Building Tool

Here’s the silver lining: A successfully managed car loan on bad credit isn’t just about transportation. It’s a powerful opportunity to rebuild your credit history. Each on-time payment you make demonstrates financial responsibility to credit bureaus.

Imagine this: You secure a reasonable $12,000 loan with an affordable payment. For the next three to five years, you make every single payment on time, without fail. Your credit score could see a significant jump, potentially moving you from “bad” to “fair” or even “good” credit. This opens doors to better interest rates on future loans, credit cards, and even housing.

This is your chance to turn a perceived disadvantage into an advantage for your future. For more tips on building credit, check out resources from institutions like the Consumer Financial Protection Bureau.

You are not defined by your past credit challenges. Getting a car loan on bad credit is not just a dream; it’s a reality achievable through smart, strategic action. By understanding your credit, budgeting wisely, exploring the right lenders, and leveraging tools like down payments or co-signers, you can secure the transportation you need and even improve your financial future.

Don’t delay. Take control of your situation today. Start by pulling your credit report and exploring your loan options. The road to reliable transportation and better credit begins with that first informed step.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.