Are you tired of feeling like your car insurance bill is a never-ending drain on your budget? You’re not alone. Many budget-conscious drivers feel trapped, paying seemingly high premiums year after year, desperate to find truly cheap car insurance without sacrificing essential protection. The truth is, the insurance market isn’t designed to make saving easy, but with the right strategy, you absolutely can cut down your costs significantly. It’s time to stop overpaying and start driving smarter.

As your financial strategist and advocate, I’m here to tell you that finding genuinely affordable car insurance is not just possible; it’s your right. This isn’t about cutting corners; it’s about being an informed consumer, understanding the levers you can pull, and avoiding common pitfalls that keep your premiums unnecessarily high. Let’s dig into how you can secure cheap car insurance and keep more money in your pocket.

Stop Overpaying: The Real Cost Drivers You Control

Your car insurance premium isn’t some arbitrary number. It’s a calculation based on risks, many of which you directly influence. Understanding these factors is your first step to unlocking savings.

Your Driving Record: The Ultimate Impact

This is probably the most straightforward factor. Accidents and speeding tickets directly flag you as a higher risk to insurers, leading to higher rates. Imagine you just got a minor speeding ticket; your premium could jump by 10-20% at renewal. Why does this matter in real life? A clean driving record is your most powerful tool for securing the lowest rates. Every ticket-free year often translates to better discounts.

Your Vehicle Choice: Not All Cars Are Created Equal

The type of car you drive significantly impacts your premium. A flashy sports car or a luxury sedan typically costs more to insure than a practical, safe family car. This is because repair costs, theft rates, and even the likelihood of high-speed accidents are factored in. For example, insuring a performance vehicle might cost you an extra $30-$50 per month compared to a standard sedan, simply due to its higher risk profile.

Your Coverage Levels and Deductibles

This is where many drivers get lost. Higher coverage limits provide more protection but come with a higher premium. Your deductible – the amount you pay out-of-pocket before insurance kicks in for a claim – also plays a huge role. A higher deductible means a lower premium, but a larger upfront cost if you have an accident. Why this matters in real life? Finding the right balance means you’re protected without paying for more than you truly need or can afford to self-insure.

- Insider Tip: Don’t automatically choose minimum state coverage without understanding the potential financial catastrophe if you’re at fault in a major accident. Your assets could be at risk.

Strategic Shopping: How to Really Get Cheap Car Insurance

The biggest mistake budget-conscious drivers make is sticking with their current insurer out of habit or perceived loyalty. The market is competitive, and companies are constantly vying for your business.

Myth to Avoid: Your Loyalty Pays Off Automatically

Many people believe staying with the same company for years guarantees the best rate. This is a common myth. Insurers often offer their most competitive rates to new customers to entice them away from competitors. Your long-term loyalty rarely gets rewarded with the rock-bottom prices you could get elsewhere.

Pro Tip: Always Get Multiple Quotes

This is non-negotiable. You should be shopping for new quotes at least once a year, or whenever you have a major life change (new car, new address, marriage). For example, I’ve seen clients save anywhere from $300 to over $1,000 annually simply by comparing quotes from three to five different companies. Tools are available online to help you with this comparison, helping you find truly cheap car insurance quickly. You can explore independent reviews and ratings to help guide your choice. ConsumerReports.org offers valuable insights into insurance company performance.

Bundling Policies for Deeper Discounts

If you own a home or rent an apartment, consider bundling your car insurance with your homeowner’s or renter’s policy from the same provider. This typically unlocks significant multi-policy discounts. Imagine you just bought your first home; bundling could save you 10-20% on both policies, totaling hundreds of dollars a year.

Leveraging Every Discount Possible

Don’t just assume you’re getting all discounts. Ask your agent directly about every discount you might qualify for. These add up quickly:

- Good Student Discount: For young drivers with strong academic records.

- Defensive Driving Course: Completing an approved course can reduce your premium.

- Anti-Theft Devices: Alarms or tracking systems can qualify you for savings.

- Low Mileage Discount: If you don’t drive much, you’re less of a risk.

- Multi-Car Discount: Insuring multiple vehicles with the same company.

- Paperless Billing/Automatic Payments: Small savings that add up.

The “How to Calculate Your Potential Savings” (Simplified)

Calculating your potential savings is less about complex math and more about smart comparison. Here’s a simple way to approach it:

1. Get at least three competitive quotes from different insurance providers for the EXACT same coverage (same liability limits, same deductibles, same additional coverages).

2. Note down your current annual premium and each new quote’s annual premium.

3. Subtract the lowest new quote from your current premium. This difference is your immediate annual saving.

4. Divide that by 12 to see your monthly savings. For example, if your current premium is $1800/year and a new quote is $1200/year, your potential saving is $600/year, or $50/month.

Why this matters? It provides a clear, actionable number that motivates you to switch. It’s a direct impact on your monthly budget.

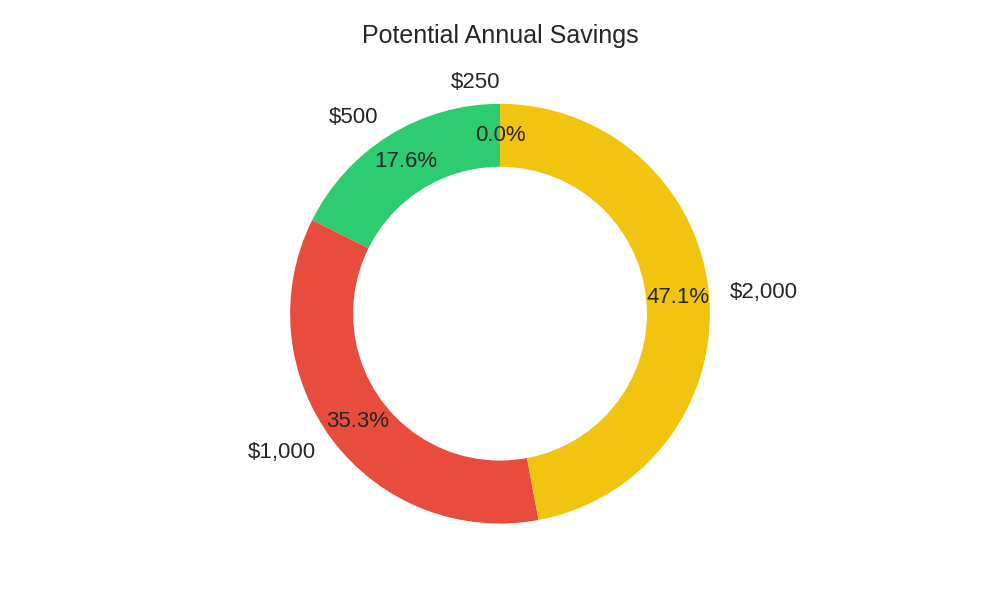

Car Insurance Savings Potential

Beyond the Basics: Advanced Tactics for Maximum Savings

Once you’ve tackled the fundamentals, consider these more advanced strategies for even deeper cuts.

Usage-Based Insurance Programs

Many insurers offer programs that track your driving habits (speed, braking, mileage) via a mobile app or a device plugged into your car. If you’re a safe, low-mileage driver, these can lead to significant discounts. For example, a driver in a telematics program might see a 5-15% discount after a few months, with potential for even more at renewal. This is a game-changer for responsible drivers.

Raising Your Deductible: Weighing the Risk

Increasing your deductible from, say, $250 to $1,000 can significantly lower your premium. Here’s a quick Pro/Con:

- Pro: Lower monthly premiums, immediate savings.

- Con: You’ll pay more out-of-pocket if you make a claim. Only do this if you have an emergency fund set aside to cover the higher deductible.

Dropping Unnecessary Coverage

For older cars that are paid off and have low market value, you might consider dropping comprehensive and collision coverage. Why this matters? If your car is only worth $3,000, and your deductible is $1,000, paying hundreds a year for these coverages might not make financial sense. If the car is totaled, your payout might not be much more than what you’ve paid in premiums over time. It’s a calculated risk best applied to vehicles whose replacement cost wouldn’t cripple your finances.

- Common Myth: All “cheap” insurance is bad insurance. The truth is, many reputable companies offer competitive rates; it’s about finding the right fit for your profile, not just the lowest name brand.

Here’s a look at how different deductible levels can influence your potential savings:

| Deductible Level | Typical Monthly Premium Range | Potential Annual Savings (vs. $250) | Out-of-Pocket Risk in Claim |

|---|---|---|---|

| $250 | $150 – $180 | $0 (Baseline) | Lower |

| $500 | $120 – $150 | $360 – $480 | Medium |

| $1,000 | $90 – $120 | $720 – $1,080 | Higher |

| $2,000 | $70 – $100 | $960 – $1,320 | Very High |

Navigating the Renewal Trap & Staying Protected

Even after finding a great rate, the work isn’t over. Your insurance needs and the market are constantly changing. Understanding insurance terms can help you make better decisions. Investopedia.com is a great resource for this.

Insider Tip: Your Loyalty Rarely Pays Off Automatically

I cannot stress this enough: your insurer won’t always give you their best rate just because you’ve been a customer for five years. They rely on inertia. Always, always check new quotes before your renewal. This keeps them honest and keeps more money in your wallet. Additionally, understanding state-specific regulations can help you advocate for yourself. The National Association of Insurance Commissioners (NAIC) provides valuable consumer resources.

Review Your Policy Annually

Your life circumstances change: you might move, get a new job (affecting commute mileage), add a driver, or pay off your car. Each of these changes can impact your premium. Don’t wait for a crisis; proactively review your policy once a year to ensure it still fits your needs and budget.

Don’t Compromise on Liability Coverage

While cutting back on comprehensive or collision for an older car might be savvy, reducing your liability coverage to bare minimums is almost always a bad idea. This coverage protects your assets (savings, home, future earnings) if you’re at fault in an accident. Skimping here could expose you to devastating financial ruin. Protect yourself first.

You have the power to control your insurance costs. Don’t let the fear of complexity or the allure of inertia cost you hundreds, or even thousands, of dollars each year. Being proactive and informed is the key to truly affordable car insurance.

Conclusion: Take Control of Your Car Insurance Today!

You now have the playbook to stop overpaying for car insurance. It’s not about magic; it’s about smart financial strategy and consistent action. Remember, your financial health is paramount, and reducing unnecessary expenses like inflated insurance premiums is a vital step. Don’t put it off. Start getting quotes, reviewing your policy, and asking the right questions today. Your wallet will thank you.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.