You’ve worked hard for your home, possibly the biggest asset you own. It’s your sanctuary, your investment, and the place where memories are made. But here’s the unsettling truth: many homeowners believe their home insurance policy offers comprehensive protection, only to find out after a disaster that they’re dangerously underinsured. You might be paying premiums every month, thinking you’re covered, but a closer look at your current home insurance could reveal critical gaps that leave your finances exposed. Are you truly prepared for the unexpected, or are you operating under a false sense of security?

The Hidden Dangers in Your Current Policy

It’s easy to assume all home insurance policies are similar, but this couldn’t be further from the truth. Many standard policies offer basic coverage that might not reflect the true cost of rebuilding your home or replacing your belongings today. This isn’t just about rising material costs; it’s about specific perils that are becoming more common and often excluded or limited in basic plans.

Insider Tip: Don’t just look at the dwelling coverage amount. Ask yourself: “If my home burned to the ground tomorrow, could I rebuild it exactly as it is now with that payout?” Often, the answer is no, especially with inflation and labor shortages driving construction costs sky-high. Your policy might only cover the depreciated value of certain items, not their replacement cost.

Common Myths to Avoid:

- Myth 1: My market value equals my rebuild cost. Your home’s market value includes land, location, and other factors. Rebuilding only covers the structure, but often costs significantly more per square foot than you think.

- Myth 2: All natural disasters are covered. Standard policies usually exclude floods and earthquakes. Even windstorms or hail might have separate, higher deductibles. Imagine a scenario where a category 3 hurricane devastates your area. Your neighbor with a basic policy might be facing a $50,000 repair bill with only $10,000 covered due to a specific wind deductible, while you, with proper endorsements, could be far better protected.

- Myth 3: My belongings are fully covered. Expensive jewelry, art, or specialized equipment often have low sub-limits, meaning you’ll only get a fraction of their value without specific endorsements or a separate “floater” policy.

Understanding Key Coverage Gaps and Your True Needs

Your goal isn’t just to have home insurance; it’s to have the right home insurance. This means understanding the different types of coverage and where your current policy might fall short. It’s not enough to simply have a policy; you need to know what it actually covers and, more importantly, what it doesn’t.

Decoding Replacement Cost vs. Actual Cash Value

This is a critical distinction that can cost you tens of thousands after a loss. Replacement Cost Value (RCV) pays to replace your damaged property with new items of similar kind and quality, without deduction for depreciation. Actual Cash Value (ACV) pays to replace your property minus depreciation. Why does this matter in real life? Imagine a 10-year-old roof is destroyed in a hail storm. With ACV, you’d only get the depreciated value of that old roof, leaving you to pay a significant portion of the cost for a new one out-of-pocket. With RCV, your policy would cover the cost of a brand-new roof.

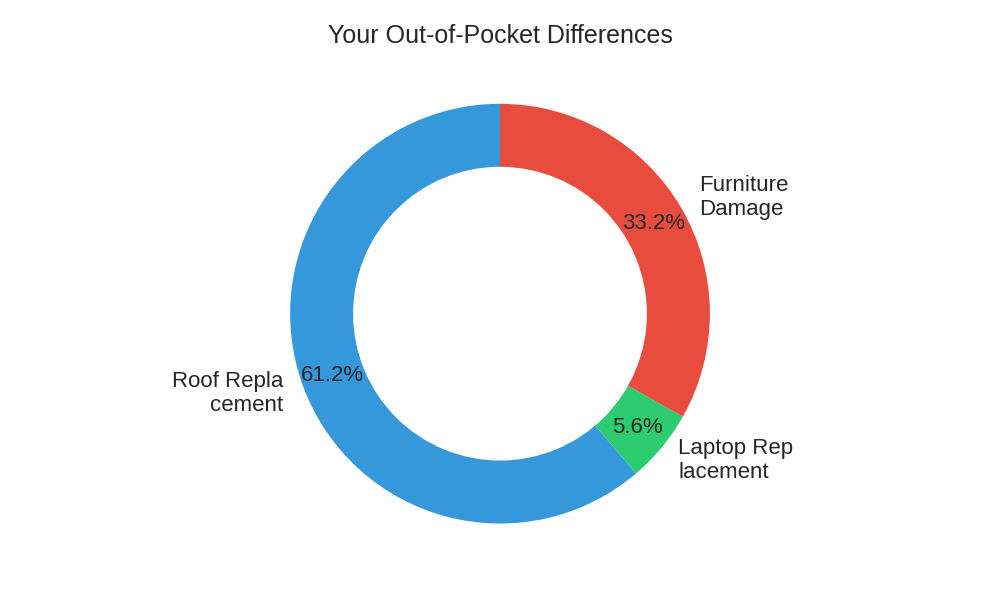

| Scenario | Basic ACV Policy Payout (Example) | Recommended RCV Policy Payout (Example) | Your Out-of-Pocket Difference |

|---|---|---|---|

| 10-Year-Old Roof Replacement ($20,000 New) | $8,000 (Depreciated Value) | $20,000 (New Replacement Cost) | $12,000 |

| Lost 5-Year-Old Laptop ($1,500 New) | $400 (Depreciated Value) | $1,500 (New Replacement Cost) | $1,100 |

| Smoke Damage to 7-Year-Old Furniture ($10,000 New) | $3,500 (Depreciated Value) | $10,000 (New Replacement Cost) | $6,500 |

This table clearly shows how choosing an ACV policy can leave you with substantial unexpected costs, underscoring the importance of understanding your coverage.

How to Calculate Your True Replacement Cost

Calculating your home’s true replacement cost isn’t about its market value. It’s about how much it would cost to rebuild it from the ground up, including debris removal, materials, and labor. This can vary widely by region. You need to consider:

- Square Footage: The size of your home.

- Construction Materials: Brick, wood, custom finishes, etc.

- Local Construction Costs: Labor rates and material availability in your area.

- Special Features: High-end kitchens, unique architectural elements, smart home systems.

A good rule of thumb is to estimate the per-square-foot rebuilding cost in your area and multiply it by your home’s square footage. For example, if rebuilding costs $150-$250 per square foot in your town, and your home is 2,000 sq ft, you’d need coverage between $300,000 and $500,000 just for the dwelling. Don’t forget to factor in demolition and debris removal, which can add another 10-15%.

Is Your Home Insurance Truly Protecting Your Asset?

This is a critical number for ensuring your dwelling coverage is adequate, preventing a huge financial burden should the worst occur.

Critical Riders and Endorsements You Might Need

Your standard home insurance policy is just the starting point. To truly protect your asset, you need to consider adding specific riders or endorsements that address your unique risks and possessions. These are often the elements generic articles overlook, but they are crucial for robust protection.

- Extended Replacement Cost or Guaranteed Replacement Cost: This is a powerful endorsement. It provides an additional percentage of coverage (e.g., 20-25% or even 50%) beyond your dwelling coverage limit, protecting you against unexpected spikes in rebuilding costs after a widespread disaster. Imagine a wildfire causing a regional shortage of contractors and materials, driving prices up. This rider could be your saving grace.

- Water Backup and Sump Pump Overflow: Many standard policies exclude damage from sewer backups or sump pump failures. If your basement has ever flooded due to a clogged drain or heavy rain, you know the devastating cost of water damage. This rider is essential if you have a basement or live in an area prone to heavy rainfall.

- Scheduled Personal Property (Floater): For your high-value items like jewelry, furs, art, or even expensive sporting equipment, a floater provides broader coverage, often without a deductible, and covers perils like accidental loss or mysterious disappearance, which standard policies usually exclude.

- Identity Theft Protection: While not directly property-related, the financial aftermath of identity theft can be severe. This rider often covers expenses like legal fees, credit monitoring, and lost wages due to identity restoration efforts.

- Increased Building Ordinance or Law Coverage: After a major loss, local building codes might require you to rebuild your home to higher, more expensive standards than it was originally built. This coverage helps pay for those increased costs.

You can learn more about specific types of coverage and what they entail by reviewing resources from organizations like the Insurance Information Institute, a highly respected source for consumer insurance knowledge.

The Smart Way to Shop and Save Without Sacrificing Protection

You don’t have to overpay for comprehensive coverage. Smart shopping involves diligence, asking the right questions, and leveraging professional advice. Your goal is to optimize your home insurance, not just minimize your premium.

Pro/Con of Raising Your Deductible:

- Pro: Lower Premiums. A higher deductible (e.g., $2,500 instead of $500) will significantly reduce your annual premium, putting money back in your pocket.

- Con: Higher Out-of-Pocket Expense. You must be financially prepared to pay that higher deductible if you make a claim. This is where a robust emergency fund comes into play. If you don’t have enough saved to cover a $2,500 or $5,000 deductible, then a lower deductible might be safer for your financial health.

Actionable Advice: Review your policy annually. Your home’s value, contents, and local rebuilding costs change. Major home improvements (a new kitchen, a finished basement) absolutely require a policy update. Talk to your agent about potential discounts for home security systems, smart home devices, being claims-free, or bundling your home and auto insurance.

Don’t be afraid to shop around. Get quotes from multiple carriers. Use online comparison tools, but always follow up with a knowledgeable independent insurance agent. They can often compare several providers and help you tailor a policy that genuinely meets your needs and budget, giving you the best of both worlds. For more state-specific consumer guidance on home insurance, you can often find valuable resources on the National Association of Insurance Commissioners (NAIC) website.

Conclusion: Take Control of Your Home’s Protection

Your home is more than just a building; it’s a significant financial and emotional investment. Relying on a basic, unexamined home insurance policy is a gamble you simply cannot afford to take. The difference between adequate coverage and dangerous gaps often amounts to thousands, even hundreds of thousands, of dollars in your pocket versus out of your pocket after a disaster.

Your immediate next step is clear: Pull out your current policy today. Don’t wait for a crisis to expose your vulnerabilities. Contact a trusted, independent insurance agent and schedule a thorough review. Discuss your dwelling’s true replacement cost, your valuable possessions, and the specific risks in your area (e.g., flood, earthquake, wildfire). Ask about those critical endorsements we discussed. Be proactive, be informed, and ensure your home insurance truly stands as a solid shield around your most valuable asset.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.