Imagine that dream vacation you’ve planned for months – the flights booked, hotels reserved, tours paid for. Now, picture it suddenly derailed. A lost passport, a sudden illness, or a canceled flight can turn your exciting journey into a nightmare of stress and unexpected expenses. This is precisely why savvy travelers consider travel insurance not an optional extra, but a vital part of their planning.

It’s the financial safety net that ensures your adventure, even when things go wrong, doesn’t become a financial catastrophe. Protecting your investment in your trip with the right travel insurance policy is a non-negotiable step for any responsible traveler. You’ve worked hard for this trip; let’s make sure nothing truly ruins it.

The Hidden Costs of “Saving” on Protection

You might think, “I’m careful, nothing will happen to me.” That’s a common, and often costly, mistake. The reality is, life happens, and when it does on the road, it often comes with a hefty price tag. For example, imagine you are on a hiking trip in Patagonia and twist your ankle, requiring emergency medical evacuation. Without travel insurance, you could be looking at a bill ranging from $25,000 to $100,000 for a medical airlift and hospital stay.

Why does this matter in real life? Because these are not just abstract numbers; they are real financial burdens that can wipe out your savings, force you into debt, or leave you stranded. Even smaller incidents, like lost luggage, can cost you hundreds of dollars in essential replacements if your airline’s liability limits aren’t enough.

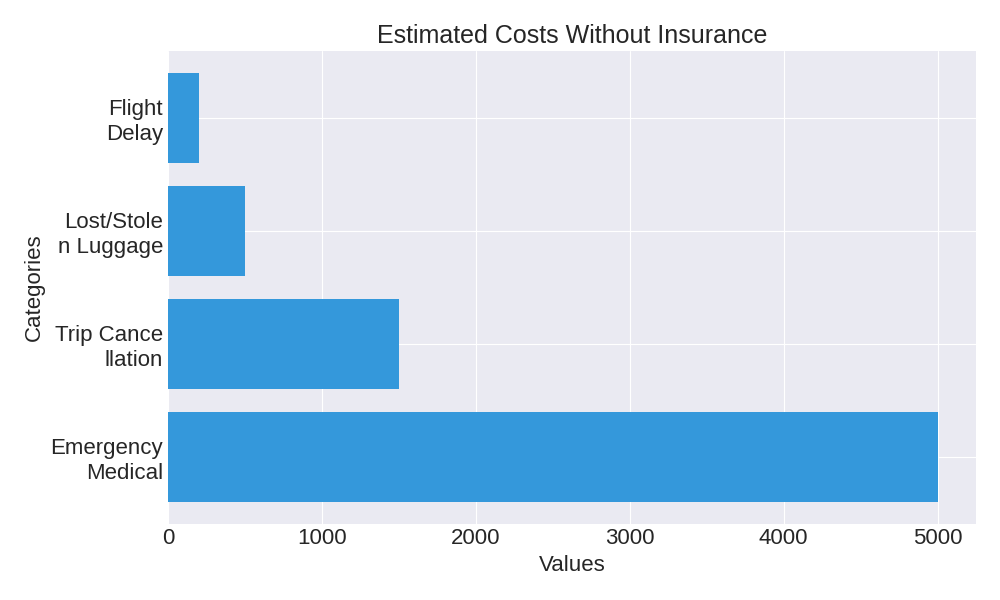

Here’s a snapshot of how easily costs can escalate:

| Mishap Scenario | Estimated Out-of-Pocket Cost (No Insurance) | Insurance Reimbursement Potential | Your Net Loss/Gain (Approx.) |

|---|---|---|---|

| Emergency Medical Care Abroad (Minor) | $5,000 – $15,000 | $4,500 – $14,000 | $500 – $1,000 (Deductible/Co-pay) |

| Trip Cancellation (Non-refundable flight/hotel) | $1,500 – $5,000 | $1,350 – $4,500 | $150 – $500 (Loss) |

| Lost/Stolen Luggage & Contents | $500 – $2,000 | $400 – $1,800 | $100 – $200 (Loss) |

| Flight Delay (Unexpected overnight stay) | $200 – $800 | $150 – $700 | $50 – $100 (Loss) |

This table illustrates a critical point: while you might still pay a small deductible, the vast majority of the financial risk is transferred away from you. This allows you to focus on resolving the issue, not panicking about the bill.

Decoding Your Travel Insurance Options

Not all policies are created equal, and understanding the differences is key to getting the right protection. You’ll typically encounter two main categories: comprehensive policies and single-benefit plans. Don’t be fooled by budget options that only cover a fraction of what you actually need.

Comprehensive Coverage: Your Peace of Mind

A comprehensive policy is your best bet for true protection. It bundles together various coverages, acting as a robust shield against multiple potential issues. These policies often include:

- Trip Cancellation & Interruption: Reimburses non-refundable expenses if your trip is canceled or cut short due to covered reasons (illness, death, natural disaster).

- Emergency Medical & Dental: Covers medical treatments, hospital stays, and emergency dental work while abroad, often a gap in your regular health insurance.

- Medical Evacuation: Arguably one of the most critical coverages, paying for transportation to a suitable medical facility, sometimes even back to your home country.

- Baggage Delay & Loss: Reimburses you for essential purchases if your luggage is delayed, and for the value of lost or stolen items.

- Travel Delay: Covers unexpected accommodation and meal costs if your trip is delayed for a specified period due to covered reasons.

Common Myth to Avoid: “My Credit Card Covers Everything”

While some premium credit cards offer limited travel benefits, relying solely on them is a significant risk. These benefits are often secondary, meaning they kick in only after your other insurance (like home or health) has paid out. They also typically have very low limits, numerous exclusions, and only cover certain types of incidents.

Insider Tip: Always read your credit card’s benefits guide thoroughly. You’ll likely find that their coverage is insufficient for major medical emergencies or high-value trip cancellations. Think of credit card benefits as a small bonus, not your primary safety net. For a deeper dive into the nuances of various policies, you can consult resources like ConsumerReports.org.

How to Calculate Your Travel Insurance Needs

Calculating your specific needs involves assessing the value of your trip, your health, and the risks associated with your destination. It’s not about complex formulas, but thoughtful consideration of what you stand to lose.

First, tally up all your non-refundable prepaid expenses. This includes flights, hotels, cruises, tours, and any other activities you’ve paid for in advance that you won’t get back if you cancel. This total gives you a baseline for your trip cancellation coverage.

Next, consider your health. If you have any existing medical conditions, you’ll need to look for policies that offer specific coverage for those. Research your destination’s medical costs and access to care. This informs your emergency medical and evacuation coverage limits.

You also need to factor in your personal items. Estimate the value of your luggage and its contents to ensure adequate baggage coverage. Remember, your policy’s deductible will also play a role in your out-of-pocket costs.

For example, if your non-refundable trip costs total between $3,000 and $7,000, you’ll want a policy that covers at least that amount for trip cancellation. If you’re traveling to a remote location, a higher medical evacuation limit (e.g., $100,000 or more) is prudent. It’s about matching the policy to your unique travel profile.

Don't let mishaps ruin your trip, get travel insurance

Enter your estimated trip costs and potential expenses:

Non-Refundable Trip Expenses ($):

Estimated Medical Emergency Cost Abroad ($):

Value of Lost/Stolen Luggage & Personal Items ($):

Insider Tips for Smart Travel Insurance Buying

Navigating the options can feel overwhelming, but a few key strategies will help you make an informed decision and avoid common pitfalls.

- Read the Fine Print, Seriously: This is where the devils (and angels) of coverage reside. Pay close attention to exclusions, definitions of “covered reasons,” and deductible amounts. Don’t assume anything is covered; verify it.

- Understand Pre-Existing Conditions: If you have a pre-existing medical condition, you must declare it. Many policies offer waivers if you purchase the insurance shortly after your initial trip deposit, but deadlines apply. Neglecting this could void your medical coverage.

- Annual vs. Single-Trip Policies: If you travel multiple times a year, an annual multi-trip policy can be more cost-effective and convenient than buying a new policy for each journey. Compare the cumulative cost and coverage.

- Know Your Destination’s Risks: Traveling to areas with political instability, high crime rates, or unique health risks (like certain tropical diseases) requires careful consideration of policy specifics. Check government travel advisories from sources like the CDC for health information or the State Department for travel warnings.

- Compare, Don’t Just Buy: Use comparison websites to get quotes from multiple providers. Look beyond the lowest price; ensure the coverage limits and terms meet your specific needs. Reputable financial news outlets, such as Forbes, often publish guides on how to compare travel insurance effectively.

Common Myth to Avoid: “I’m young and healthy, nothing will happen.” While you might be less prone to certain medical issues, accidents, lost luggage, flight delays, and trip cancellations can affect anyone, regardless of age or health. Age doesn’t protect you from a broken leg on a ski trip or a hurricane disrupting your beach vacation.

Conclusion: Invest in Peace of Mind

Your travel plans are an investment, both financially and emotionally. Don’t let unexpected events turn your dream trip into a financial burden or a stressful nightmare. By choosing the right travel insurance, you’re not just buying a piece of paper; you’re buying peace of mind, allowing you to truly relax and enjoy your adventure.

Take Action Now: Don’t wait until the last minute. Research and purchase your travel insurance policy as soon as you’ve made your initial trip deposit. Protect your investment and ensure your next journey is memorable for all the right reasons.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.