Navigating homeowners insurance quotes can seem daunting, but it’s one of the most crucial financial steps for any homeowner. The right policy protects your most valuable asset from unforeseen events like fires, storms, theft, or liability claims. Understanding how to effectively compare homeowners insurance quotes is not just about finding the cheapest option; it’s about securing comprehensive coverage that offers real peace of mind without overpaying. By understanding the nuances of homeowners insurance quotes, you can save hundreds instantly.

The Fundamentals of Homeowners Insurance

Before diving into quotes, it’s essential to grasp the core components of a homeowners insurance policy. This knowledge empowers you to compare policies effectively and ensure you’re getting adequate protection. Policies generally cover your dwelling, personal belongings, liability, and additional living expenses.

Key Coverage Types Explained

Each part of your policy plays a vital role in protecting your home and finances. Knowing what each covers helps you tailor your insurance to your specific needs. This prevents you from being underinsured or paying for coverage you don’t need.

- Dwelling Coverage: This protects the physical structure of your home, including attached garages and permanent fixtures. Its purpose is to rebuild or repair your house after covered damage.

- Personal Property Coverage: This insures your belongings, such as furniture, electronics, clothing, and other personal items. Imagine a fire destroys your home; this coverage helps replace all your possessions.

- Liability Coverage: This protects you financially if someone is injured on your property or if you accidentally damage someone else’s property. For example, if a guest slips on your icy sidewalk, your liability coverage would help with their medical bills and legal costs.

- Additional Living Expenses (ALE): Also known as Loss of Use coverage, ALE pays for temporary housing, food, and other costs if your home becomes uninhabitable due to a covered peril. If a storm forces you out for repairs, this coverage ensures you don’t have extra financial stress.

Understanding Cost Factors: What Drives Your Premium?

Many variables influence the price of your homeowners insurance quotes. Understanding these factors can help you identify areas where you might save money. Insurance companies assess your risk based on a variety of criteria, leading to different premium amounts.

- Location: Where your home is situated significantly impacts premiums. Proximity to fire stations, local crime rates, and susceptibility to natural disasters (e.g., hurricanes, wildfires, earthquakes) all play a role. A home in a flood-prone area, for instance, will likely have higher premiums or require separate flood insurance.

- Home’s Characteristics: The age, construction materials, roof condition, and size of your home affect its rebuilding cost and vulnerability. Newer homes with updated systems often receive lower rates.

- Deductible: This is the amount you pay out-of-pocket before your insurance kicks in. A higher deductible generally leads to lower monthly premiums. Why does this matter? If you choose a $2,000 deductible instead of $500, your annual premium could drop significantly, saving you money if you don’t file frequent small claims.

- Credit Score: In many states, your credit-based insurance score can influence your premium. Insurers use this as a predictor of how likely you are to file claims. A strong credit history often translates to lower rates.

- Claims History: Frequent past claims can signal higher risk to insurers, leading to increased premiums. It’s often wise to only file claims for significant losses.

How to Calculate Potential Savings: A Practical Approach

Determining your actual insurance needs and understanding potential discounts is crucial for maximizing savings. It’s not about complex math, but rather smart choices and clear comparisons.

Step-by-Step Guide to Saving on Homeowners Insurance

- Assess Your Coverage Needs: Don’t just pick standard amounts. Get an accurate estimate of your home’s replacement cost (not its market value). Consider the value of your personal belongings. An online home appraisal tool or professional assessment can help. Why does this matter? Over-insuring is a waste of money, while under-insuring leaves you vulnerable.

- Gather Multiple Homeowners Insurance Quotes: Contact at least 3-5 different insurers. Each company uses its own risk models, so prices can vary widely for identical coverage. Use online comparison tools or work with an independent agent.

- Review Deductible Options: As discussed, a higher deductible lowers your premium. For example, moving from a $500 deductible to a $1,000 deductible could reduce your annual premium by $100-$300. In a typical scenario, if your premium is $1,200 with a $500 deductible, it might drop to $950 with a $1,000 deductible, saving you $250 annually.

- Explore Discounts: Many insurers offer discounts for various reasons. Common ones include:

- Bundling: Combining your home and auto insurance with the same provider can save you 10-20% on both policies.

- Home Safety Features: Discounts for smoke detectors, burglar alarms, deadbolt locks, fire extinguishers, and sprinkler systems.

- New Home/Renovations: Newer homes or those with recent updates (plumbing, electrical, roof) often qualify for lower rates.

- Loyalty: Staying with the same insurer for several years might earn you a discount.

- No Claims History: Some insurers reward policyholders who haven’t filed claims for a certain period.

- Improve Your Credit Score: A better credit score can lead to lower insurance rates in many states. Pay bills on time and manage debt responsibly.

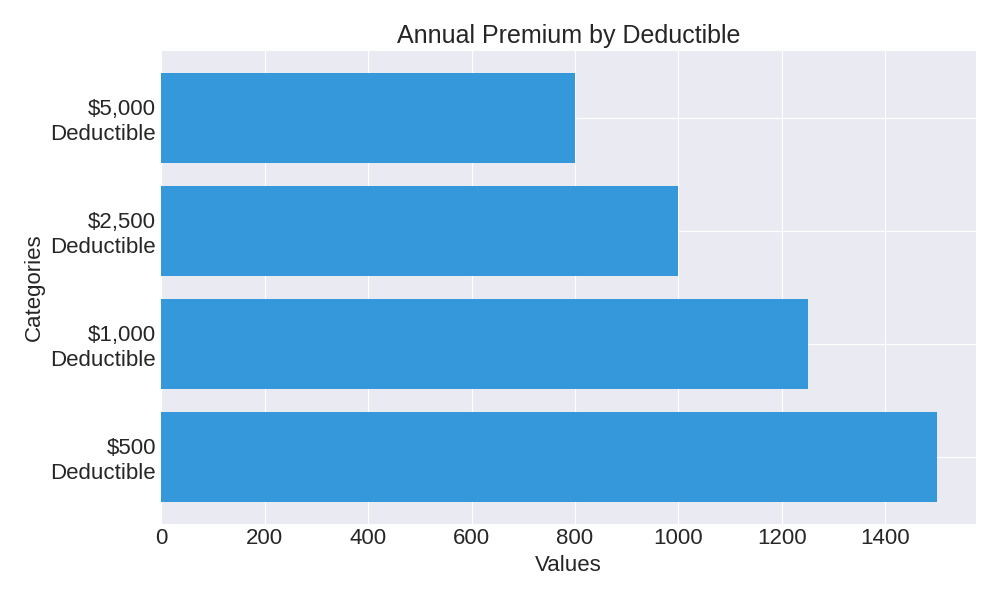

Here’s a simplified look at how different deductible choices can impact your annual premium:

| Deductible Amount | Estimated Annual Premium | Potential Annual Savings (vs. $500) |

|---|---|---|

| $500 | $1,500 – $1,800 | N/A |

| $1,000 | $1,250 – $1,500 | $250 – $300 |

| $2,500 | $1,000 – $1,200 | $500 – $600 |

| $5,000 | $800 – $1,000 | $700 – $800 |

The Power of Comparing Homeowners Insurance Quotes

Comparing homeowners insurance quotes is more than just price shopping. It’s about finding the right balance of coverage and cost. A seemingly cheaper policy might have a much higher deductible or exclude critical protections, leaving you exposed. Always compare policies side-by-side, looking at coverage limits, deductibles, and any exclusions.

For more consumer information on insurance, you can visit the National Association of Insurance Commissioners (NAIC) website.

The actual calculation of your premium is complex, involving many factors as discussed above. However, the savings come from your proactive choices.

To estimate your savings:

1. Get multiple quotes with your current coverage settings.

2. Then, get new quotes by adjusting variables, such as increasing your deductible or inquiring about bundling options.

3. The difference in the annual premium is your potential saving.

For example, if Quote A is $1500/year and Quote B is $1200/year for comparable coverage after applying discounts, your annual saving is $300.

Homeowners Insurance Quotes Save Hundreds Instantly

FAQ: Common Doubts About Homeowners Insurance Quotes

Q1: Should I always choose the lowest quote?

A: Not necessarily. The lowest quote might come with lower coverage limits, a higher deductible, or more exclusions. Always compare the coverage details, not just the price. Ensure the policy adequately protects your home and assets.

Q2: How often should I compare homeowners insurance quotes?

A: It’s wise to compare quotes annually or whenever you have a significant life change. This includes buying a new home, completing major renovations, or experiencing a change in your financial situation. Even without changes, market rates fluctuate, so checking regularly can reveal savings.

Q3: What’s the difference between replacement cost and actual cash value?

A: Replacement cost coverage pays to rebuild or repair your home and replace belongings at today’s prices, without deducting for depreciation. Actual cash value (ACV) coverage pays the depreciated value of your property. Replacement cost offers more comprehensive protection and is generally recommended, even if it has a slightly higher premium. To learn more about consumer protections, visit consumerfinance.gov.

Q4: Does my credit score affect my homeowners insurance rates?

A: Yes, in most states, insurers use a credit-based insurance score as part of their risk assessment. A higher score typically indicates a lower risk to insurers, which can lead to lower premiums. Maintaining good credit habits is beneficial for many financial aspects, including insurance.

Q5: Can I get coverage for specific risks like floods or earthquakes?

A: Standard homeowners insurance policies typically exclude damage from floods and earthquakes. You usually need to purchase separate policies or endorsements for these specific perils. If you live in a high-risk area, these specialized coverages are crucial for full protection. The U.S. government provides more information on flood insurance through FEMA’s National Flood Insurance Program on USA.gov.

Conclusion: Empower Yourself to Save

Securing the right homeowners insurance doesn’t have to break the bank. By understanding the components of your policy, the factors that influence your premiums, and actively comparing homeowners insurance quotes, you gain control over your coverage and costs. Remember that saving money shouldn’t come at the expense of adequate protection for your most valuable asset.

Actionable CTA: Start today by reviewing your current policy and gathering new quotes from multiple providers. Visit their websites or contact an independent agent to see how much you can save instantly while maintaining comprehensive coverage.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.