Navigating the world of insurance can often feel overwhelming, but finding the right protection for your assets and loved ones is a critical component of sound financial planning. This guide will equip you with the knowledge and actionable steps to find top insurance agencies near you, ensuring you make informed decisions that safeguard your future. We’ll demystify complex concepts and provide a clear roadmap to selecting a reliable partner, emphasizing why a thorough search for quality insurance agencies is one of the best financial moves you can make. The goal is to find an agency that truly understands your needs and offers the best value.

Why Partnering with the Right Insurance Agency Matters

Choosing an insurance agency isn’t just about finding the cheapest premium; it’s about securing comprehensive protection and peace of mind. A good agency acts as your advocate, helping you understand complex policy language and ensuring you have adequate coverage without overpaying. They translate industry jargon into plain language, making sure you know exactly what you’re buying.

Why does this matter in real life? Imagine you’re a new homeowner in a region prone to severe weather. A skilled insurance agency will not just quote standard homeowner’s insurance but will also highlight the importance of flood insurance, earthquake coverage, or extended coverage for specific perils, even if not legally mandated. They anticipate potential risks you might overlook, helping you avoid devastating financial losses down the line. This expert guidance is invaluable, potentially saving you tens of thousands of dollars in an unforeseen event.

Types of Insurance Agencies: Understanding Your Options

Not all insurance agencies operate the same way. Understanding the differences is key to choosing the right fit for your unique situation. Each type offers distinct advantages.

- Independent Agencies: These agencies work with multiple insurance companies. They can shop around on your behalf, comparing policies and prices from various carriers to find the best fit for you. This often leads to more tailored options and competitive rates.

- Captive Agencies: A captive agent works exclusively for one insurance company (e.g., State Farm, Allstate). While they have deep expertise in their company’s products, their offerings are limited to that single carrier. They can be excellent for those who value brand loyalty or prefer a specific insurer’s reputation.

- Direct Writers/Online Platforms: These are companies that sell insurance directly to consumers, often online or over the phone, without a traditional agent. While they can offer convenience and sometimes lower initial costs, the personalized advice and advocacy of an agent might be less prominent.

Imagine you need specialized coverage for a vintage car collection in addition to standard home and auto insurance. An independent agency would likely be your best bet, as they could find niche insurers offering specific policies for collectibles, which a single-carrier captive agent might not have access to. Conversely, if you’re comfortable with a well-known brand and prefer a simplified process, a captive agent might provide a seamless experience. The key is to match the agency type to your complexity of needs and preference for personalized service.

Key Factors to Consider When Choosing an Agency

Selecting the right insurance agency requires diligent research beyond just the quoted price. Focus on these critical elements to ensure a trustworthy partnership.

- Reputation and Reviews: Check online reviews on platforms like Google, Yelp, or industry-specific sites. Look for consistent feedback regarding customer service, responsiveness, and claims handling. A pattern of positive experiences indicates reliability.

- Licenses and Certifications: Ensure the agency and its agents are properly licensed in your state. You can verify this through your state’s Department of Insurance website. This ensures they meet professional standards and regulations. The National Association of Insurance Commissioners (NAIC) offers valuable consumer resources to understand state regulations and verify licenses. You can learn more at NAIC.org.

- Range of Products Offered: Does the agency offer all the types of insurance you need (auto, home, life, business, etc.)? A single agency handling multiple policies can simplify your financial management and may even offer multi-policy discounts.

- Customer Service and Claims Support: How accessible are they? Are they responsive to inquiries? A good agency provides clear communication and robust support, especially when you need to file a claim. You want an agency that will guide you through potentially stressful situations.

- Financial Strength of Carriers: While the agency is your point of contact, the underlying insurance companies’ financial stability is paramount. Agencies often partner with carriers rated highly by organizations like A.M. Best or Standard & Poor’s, indicating their ability to pay claims.

Why does this matter in real life? Consider a scenario where a local business owner, Ms. Chen, selected an agency based solely on the lowest premium. When a fire damaged her shop, she found the agency’s communication poor, and the underlying insurer had a slow, complex claims process due to solvency issues. This delay caused significant business interruption and stress. Had she prioritized reputation, carrier financial strength, and responsive customer service, her recovery process would have been much smoother. Always prioritize value and reliability over just the lowest upfront cost.

How to Calculate Your Insurance Needs (and Why It’s Crucial)

Determining how much insurance you need isn’t guesswork; it’s a careful assessment of your potential financial risks. For instance, with life insurance, you’re looking to replace your income for your dependents. A common rule of thumb is to aim for 10-12 times your annual salary. However, a more personalized calculation involves summing your outstanding debts (mortgage, loans), future expenses (college tuition, retirement for spouse), and subtracting existing assets. The result indicates your necessary coverage.

For property insurance, calculate the replacement cost of your home and its contents, not its market value. Market value includes land, but insurance only covers the structure and belongings. An agency can help with this, but having an inventory and understanding local construction costs is a good starting point. This prevents you from being underinsured after a disaster.

Why does this matter in real life? If someone earning, say, $60,000 annually has dependents but only secures a $100,000 life insurance policy, it would only cover less than two years of their income. This could leave their family in a significant financial bind. Adequately calculating your needs ensures that your insurance serves its purpose: providing a true financial safety net when it’s most needed.

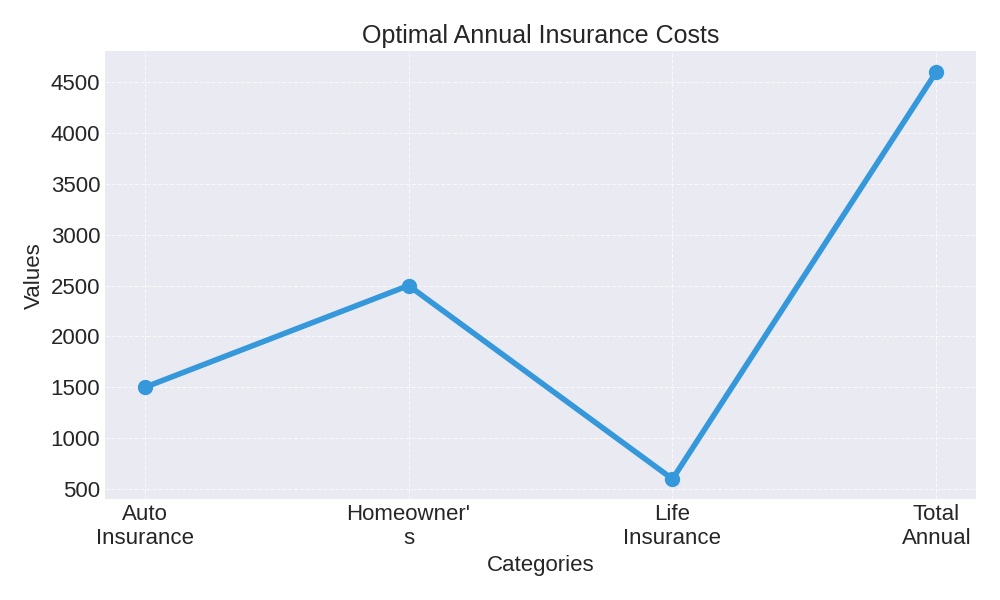

Potential Annual Insurance Savings

| Coverage Type | Scenario: Basic Coverage (Annual Cost) | Scenario: Optimal Coverage (Annual Cost) | Potential Long-Term Savings/Protection (Over 5 Years) |

|---|---|---|---|

| Auto Insurance (Full Coverage) | $1,200 | $1,500 | Protect against $5,000 – $15,000 accident costs |

| Homeowner’s Insurance (Standard) | $1,800 | $2,500 (incl. specific peril rider) | Avoid $20,000 – $50,000 in un-covered damages |

| Life Insurance ($500k term) | $400 | $600 (higher benefit/longer term) | Secure $200,000 – $500,000 for dependents |

| Total Annual Cost Range | $3,400 – $3,500 | $4,600 – $4,700 | Significant financial peace of mind |

Note: All figures are illustrative ranges and vary based on individual circumstances, location, and specific policy details. The “Potential Long-Term Savings/Protection” highlights the financial impact of having adequate coverage when a claim occurs, rather than direct cost savings.

Step-by-Step: Finding Top Insurance Agencies Near You

Finding the right insurance partner can be a straightforward process if you follow these steps. Be systematic in your approach to ensure you’re making the best choice.

- Assess Your Needs: Before contacting any agency, list all the types of insurance you require (e.g., auto, home, renter’s, life, health, business). Estimate the coverage amounts based on your assets and liabilities. This preparation saves time and ensures you get relevant quotes.

- Gather Referrals: Ask friends, family, and colleagues for recommendations. Personal experiences can provide valuable insights into an agency’s customer service and reliability. Local community groups or online forums can also be good sources.

- Utilize Online Search Tools: Search for “insurance agencies near me” or “best independent insurance agents [your city/state]”. Websites like the Independent Insurance Agents & Brokers of America (IIABA) or your state’s insurance department can provide lists of licensed professionals. You can find more financial guidance and news at Bloomberg.com.

- Check State Licensing and Complaint Records: Always verify an agency’s license through your state’s Department of Insurance website. This public record often includes any consumer complaints or disciplinary actions, offering transparency. Many states, like California, provide a convenient online search for licensees. Refer to your state’s official government website (e.g., USA.gov and navigate to your state’s specific insurance department) for this information.

- Request Multiple Quotes: Contact at least three different agencies. Provide them with the same information to ensure you’re comparing apples to apples. Don’t just look at the bottom-line premium; compare coverage limits, deductibles, and policy exclusions.

- Interview Potential Agents: Ask questions about their experience, the carriers they represent, their claims process, and how they handle customer inquiries. A good agent will take the time to explain everything clearly and answer all your questions without rushing you.

- Review Policy Documents Carefully: Before signing anything, read the policy documents thoroughly. Understand what is covered, what is excluded, and your responsibilities. Ask the agent to clarify any terms you don’t understand.

FAQ: Common Doubts About Insurance Agencies

Q: Is it better to use an independent agent or go directly to an insurance company?

- A: It depends on your preference. An independent agent can compare policies from multiple companies to find you the best rates and coverage. Going directly to a company might be simpler if you know exactly what you want from a specific brand, but you won’t get comparative quotes from other carriers.

Q: How often should I review my insurance policies?

- A: It’s recommended to review your policies annually or whenever you experience a significant life event. This includes moving, getting married, having a child, buying a new car, or making major home renovations. These changes can impact your coverage needs.

Q: Can an insurance agency help me file a claim?

- A: Absolutely. A good insurance agency will guide you through the claims process, explaining what information you need, helping you fill out forms, and acting as an intermediary with the insurance company. They should be your first point of contact after a loss.

Q: What if I’m unhappy with my current insurance agency?

- A: You have the right to switch agencies or carriers at any time. Review your current policy for any cancellation fees (rare for auto/home, more common for life). Follow the steps outlined above to find a new agency, then notify your old agency of your decision.

Conclusion

Finding top insurance agencies near you is a foundational step in building a secure financial future. By understanding the different types of agencies, knowing what factors to prioritize, and following a structured search process, you can select a partner that provides optimal protection and exceptional service. Don’t rush this decision; the right agency can be a lifelong ally in managing risks and protecting your wealth.

Take the first step today. Start researching and comparing your options to find an insurance agency that truly aligns with your needs and offers the best value and peace of mind.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.