Navigating the world of health insurance can feel like a complex puzzle, but securing affordable health insurance doesn’t have to be overwhelming. This guide is designed to empower you with the knowledge and steps needed to find coverage that protects both your health and your wallet. We’ll break down the key concepts, explore your options, and show you how to find the best value for your needs, ensuring you can get covered and pay less.

The core of finding affordable health insurance lies in understanding the available subsidies and plan types. Many people qualify for significant financial assistance that can dramatically reduce their monthly premiums and out-of-pocket costs. By knowing where to look and what factors influence pricing, you can make informed decisions and ensure you have crucial protection.

Understanding Your Options for Affordable Health Insurance

There are several primary pathways to obtaining health insurance, each with distinct eligibility criteria and benefits. Understanding these options is the first step toward finding a plan that fits your budget and lifestyle. It’s crucial to explore all avenues to ensure you don’t miss out on potential savings.

The Health Insurance Marketplace (ACA)

The Affordable Care Act (ACA), also known as Obamacare, created Health Insurance Marketplaces (or Exchanges) where individuals and families can compare and enroll in private health plans. This is often the best place to find affordable health insurance if you don’t get coverage through an employer or government program. The Marketplace offers various plan types, categorized by metal levels.

Why this matters in real life: The Marketplace is unique because it provides financial assistance in the form of premium tax credits and cost-sharing reductions. These subsidies can significantly lower your monthly payments and even reduce what you pay when you seek care. For example, if you are a single person earning between $30,000 and $50,000 annually, you might qualify for substantial tax credits that cover a large portion of your premium.

Medicaid and CHIP

Medicaid is a joint federal and state program that provides health coverage to millions of low-income Americans. Eligibility is primarily based on income relative to the Federal Poverty Level (FPL). The Children’s Health Insurance Program (CHIP) offers low-cost health coverage for children in families who earn too much to qualify for Medicaid but cannot afford private insurance.

Why this matters in real life: These programs provide comprehensive, often free or very low-cost, health care to vulnerable populations. Imagine you are a single parent working part-time, earning $25,000 a year with two children. In many states, your family would likely qualify for Medicaid or CHIP, ensuring access to doctors, prescriptions, and hospital care without burdensome costs.

You can check specific eligibility requirements for your state at Healthcare.gov, the official website for the ACA Marketplace.

Employer-Sponsored Plans

Many Americans receive health insurance through their employers. These plans are typically cost-shared, with your employer covering a portion of the premium. Employer plans often offer comprehensive benefits and can be a cost-effective option if available to you.

Why this matters in real life: While generally good, employer plans aren’t always the cheapest option for everyone, especially if you have a family. In a typical scenario, an individual might pay $100-$200 per month for their employer plan, but a family plan could range from $500-$1000 or more. It’s wise to compare your employer’s family plan cost against options on the Marketplace, as you might find more affordable health insurance there if you qualify for subsidies.

Key Factors Influencing Your Health Insurance Costs

Understanding the terminology of health insurance is essential for making informed decisions. Your total cost isn’t just the monthly premium; it includes several components that come into play when you use your plan. Neglecting these can lead to unexpected expenses.

Premiums, Deductibles, and Co-pays

- Premiums: This is the fixed amount you pay monthly to keep your insurance coverage active.

- Deductible: This is the amount of money you must pay out of pocket for covered medical services before your insurance company begins to pay. For example, if your deductible is $2,000, you pay the first $2,000 in covered medical expenses yourself.

- Co-payment (Co-pay): A fixed amount you pay for a covered health care service after you’ve paid your deductible. For instance, a $30 co-pay for a doctor’s visit.

Coinsurance and Out-of-Pocket Maximum

- Coinsurance: Your share of the costs of a covered health care service, calculated as a percentage (e.g., 20%) of the allowed amount for the service. This applies after you’ve met your deductible.

- Out-of-Pocket Maximum: This is the most you have to pay for covered services in a plan year. Once you reach this amount, your insurance plan pays 100% of the cost of covered benefits. It’s your ultimate financial protection against catastrophic medical bills.

Why these matter in real life: Consider two scenarios. A young, healthy individual might opt for a plan with a lower premium but a higher deductible, expecting minimal medical needs. Conversely, a family with a chronic condition or expected medical procedures might prefer a higher premium plan with a lower deductible and co-pays, knowing they’ll meet the deductible quickly and want costs to be predictable.

How to Calculate Your Potential Savings on Health Insurance

Estimating your potential savings is crucial for finding truly affordable health insurance. The primary way to save is through federal financial assistance, primarily premium tax credits and cost-sharing reductions, available via the Health Insurance Marketplace.

Estimating Premium Tax Credits

Premium tax credits (subsidies) lower your monthly premium. The amount you qualify for depends on your household income, household size, and the cost of health plans in your area. Generally, the lower your income relative to the Federal Poverty Level, the larger your tax credit will be. These credits can be applied directly to your monthly premium, reducing what you pay out of pocket each month.

Estimating Cost-Sharing Reductions (CSRs)

Cost-sharing reductions are another form of financial help that lowers the amount you have to pay for deductibles, co-pays, and coinsurance. You can only get CSRs if you enroll in a Silver plan on the Marketplace and your income is below a certain level. They can significantly reduce your out-of-pocket expenses when you use medical services, making your care much more affordable.

You don’t need complex formulas to estimate these. Your best approach is to use the official tools. When you visit Healthcare.gov and enter your basic information, the system will automatically calculate any subsidies you may qualify for. It shows you the net premium you’d pay after the tax credits are applied. For example, if a plan costs $500/month and you qualify for a $300/month tax credit, you’d only pay $200. The calculator guides you through the process.

The key is to accurately report your income and household size. Even small differences can impact your eligibility for subsidies. Don’t guess; use your estimated annual income for the coming year.

Affordable Health Insurance: Premium Savings Calculator

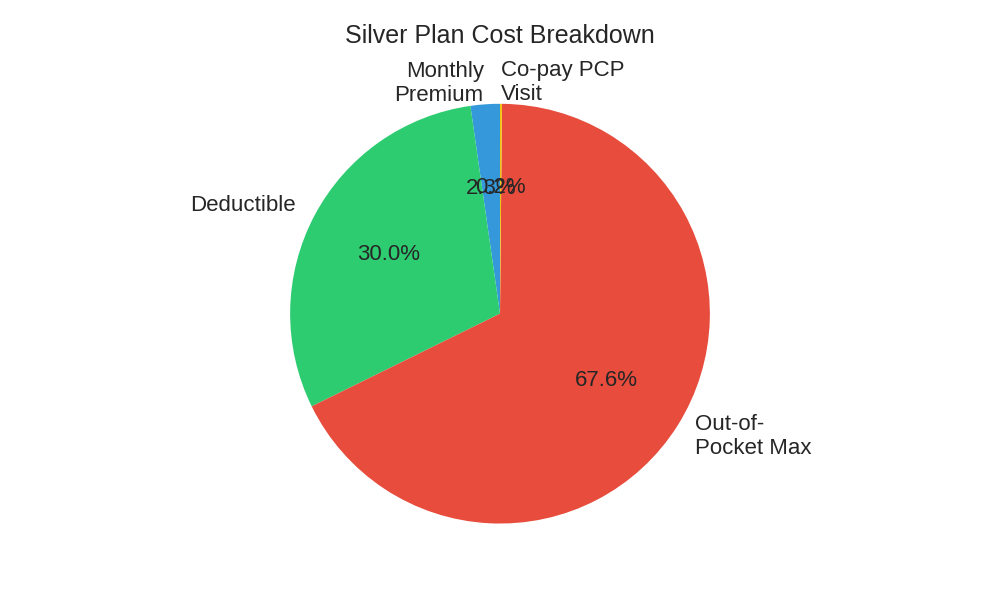

Understanding Plan Value: A Comparison Scenario

Choosing a plan isn’t just about the premium. It’s about the total potential cost. Let’s compare two hypothetical plans for a family of three, assuming they qualify for a premium tax credit of $400/month. This table illustrates how different plan types impact overall financial exposure.

| Feature | Bronze Plan Example | Silver Plan Example (with CSRs) |

|---|---|---|

| Monthly Premium (Before Subsidy) | $650 | $700 |

| Monthly Premium (After $400 Subsidy) | $250 | $300 |

| Deductible (Family) | $12,000 | $4,000 |

| Co-pay (PCP Visit) | $60 (after deductible) | $20 (before deductible) |

| Out-of-Pocket Maximum (Family) | $18,000 | $9,000 |

| Why it matters: | Lower monthly cost, but higher risk for medical bills if you get sick or injured. Best for very healthy individuals/families. | Slightly higher monthly cost, but much lower deductible and out-of-pocket maximum. Significant savings if you need regular care. |

This table highlights that a slightly higher premium for a Silver plan, especially with cost-sharing reductions, can offer far greater protection against high medical bills throughout the year. The total cost of care, not just the premium, is what defines truly affordable health insurance.

Steps to Finding Affordable Health Insurance

Follow these practical steps to navigate your options and secure the best health plan for your situation.

- Gather Your Information: You’ll need estimated household income for the coming year, household size, and current health insurance details (if any). Having these ready speeds up the process.

- Explore the Health Insurance Marketplace: Visit Healthcare.gov. Enter your zip code and household details to see plans available in your area. This is where you’ll find out if you qualify for subsidies.

- Check Medicaid/CHIP Eligibility: When you apply through the Marketplace, it will automatically assess your eligibility for Medicaid or CHIP. If you qualify, you’ll be directed to your state’s Medicaid agency.

- Compare Employer Plans (if applicable): If you have an employer-sponsored plan, get the full details, including premiums, deductibles, and out-of-pocket maximums for both individual and family coverage. Compare these costs against Marketplace plans, especially if you qualify for tax credits.

- Understand Plan Metal Levels:

- Bronze: Low premiums, high deductibles. Best if you rarely see a doctor.

- Silver: Moderate premiums, moderate deductibles. The only plans that qualify for cost-sharing reductions. A good balance for many.

- Gold/Platinum: High premiums, low deductibles/co-pays. Best if you expect to use a lot of medical services.

- Review Doctor Networks and Prescription Coverage: Before enrolling, ensure your preferred doctors are in the plan’s network and that your essential prescriptions are covered. Out-of-network care can be very expensive.

- Enroll During Open Enrollment: Generally, you can only enroll or change plans during the annual Open Enrollment Period (usually November 1st to December 15th). However, a Qualifying Life Event (QLE) like marriage, birth of a child, or losing other coverage can trigger a Special Enrollment Period (SEP).

Frequently Asked Questions (FAQ)

Q: What is the “Open Enrollment Period”?

A: The Open Enrollment Period is a specific time each year when you can sign up for, change, or re-enroll in a health insurance plan through the Marketplace. Outside of this period, you generally need a “Qualifying Life Event” to enroll.

Q: Can I get affordable health insurance if I have a pre-existing condition?

A: Yes, absolutely. Under the Affordable Care Act, insurance companies cannot refuse to cover you or charge you more because of a pre-existing condition. All plans sold on the Marketplace must cover essential health benefits.

Q: What if my income changes during the year?

A: It’s critical to report any income changes to the Marketplace as soon as possible. Your subsidies are based on your estimated annual income, and changes can affect your eligibility. Adjustments prevent you from owing money back at tax time or missing out on additional assistance.

Q: Are short-term health plans a good option for affordable health insurance?

A: Short-term plans can have lower premiums, but they often offer less comprehensive coverage. They may not cover pre-existing conditions and are not required to cover essential health benefits. They are generally not considered affordable health insurance in the comprehensive sense and are meant for temporary gaps in coverage.

Q: Where can I get personalized help?

A: You can find free, local help from trained assisters, navigators, or agents through the Marketplace website. These professionals can guide you through the enrollment process and help you compare plans. You can also consult a financial advisor for broader planning, as suggested by resources like Fidelity for comprehensive financial guidance.

Conclusion

Finding affordable health insurance is a critical component of personal financial planning and overall well-being. By understanding your options, leveraging available subsidies, and carefully comparing plans, you can secure comprehensive coverage that fits your budget. Don’t let the complexity deter you; the resources and steps outlined here are designed to make the process clear and actionable.

Call to Action: Take the first step today! Visit Healthcare.gov to explore your options, estimate your subsidies, and find an affordable health insurance plan that provides the protection you deserve. Your health and financial security are worth the effort.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.