Navigating the world of auto financing can be daunting, but choosing the right lender can save you thousands. If you’re looking for a smart way to finance your next vehicle, considering an auto loan from a credit union is often your best bet. Credit unions consistently offer competitive rates and a member-centric approach that traditional banks often can’t match. This comprehensive guide will explain everything you need to know about securing an auto loan from a credit union, ensuring you unlock lower rates and better terms for your new ride.

Summary: Unlock Lower Rates and Personalized Service

Credit unions are non-profit financial cooperatives owned by their members. This structure means they typically offer lower interest rates, fewer fees, and more flexible loan terms compared to for-profit banks. When you secure an auto loan from a credit union, you’re not just a customer; you’re an owner, which often translates to a more favorable borrowing experience and significant savings over the life of your loan. For anyone seeking an auto loan from a credit union, the process is straightforward and can lead to substantial financial benefits.

What Makes Credit Unions Different?

Credit unions operate on a “people helping people” philosophy. Unlike commercial banks that focus on shareholder profits, credit unions return their earnings to members in the form of lower interest rates on loans, higher yields on savings accounts, and fewer fees. This fundamental difference directly impacts the cost of your auto loan.

Why this matters in real life: Imagine you’re comparing two loan offers for a $25,000 car. A traditional bank might offer you an Annual Percentage Rate (APR) of 6.5%, while a credit union might offer 4.5%. Over a five-year loan term, that 2% difference could save you well over $1,000 in interest alone. This is a direct benefit of the credit union’s member-owned structure.

Why Choose a Credit Union for Your Auto Loan?

The advantages of getting an auto loan from a credit union extend beyond just lower rates. They encompass a holistic approach to your financial well-being.

- Lower Interest Rates: As non-profits, credit unions often have lower operating costs and pass these savings directly to their members. This means a more affordable loan.

- Flexible Loan Terms: Credit unions are often more willing to work with members to tailor loan terms that fit individual budgets and needs. You might find more options for loan duration or payment schedules.

- Personalized Service: Being a member means you often receive more attentive and personalized service. Loan officers typically have more discretion to consider your unique financial situation.

- Fewer Fees: You’ll generally encounter fewer and lower fees for things like loan origination, late payments, or early payoff penalties. This further reduces the overall cost of your financing.

Mini Case Study with Numbers: Let’s say you’re buying a $30,000 car.

Scenario A (Big Bank): 6.0% APR over 60 months. Your estimated total interest paid could be around $4,700-$5,000.

Scenario B (Credit Union): 4.0% APR over 60 months. Your estimated total interest paid could be around $3,000-$3,300.

In this typical example, the credit union could save you roughly $1,500-$2,000. This significant difference can free up your budget for other important expenses.

How to Qualify for a Credit Union Auto Loan

Qualifying for a credit union auto loan is similar to qualifying for a bank loan, but with an added step: membership. Here’s what you’ll typically need:

- Credit Union Membership: You must be a member of the credit union to get a loan. Eligibility usually depends on where you live, work, or specific affiliations. Joining often requires a small deposit (e.g., $5-$25) into a savings account.

- Good Credit Score: While credit unions may be more flexible, a strong credit score (generally 670 or higher) will qualify you for the best rates. A higher score signals less risk to the lender.

- Stable Income and Employment: Lenders want to see that you have a consistent source of income to repay the loan. You’ll typically need to provide proof of employment and income.

- Low Debt-to-Income (DTI) Ratio: Your Debt-to-Income (DTI) Ratio is the percentage of your gross monthly income that goes towards debt payments. Lenders prefer a DTI below 43%, ensuring you can comfortably manage new payments.

Scenario: Imagine you earn $4,000 a month before taxes, and your current monthly debt payments (credit cards, student loans, mortgage/rent) total $1,500. Your DTI would be 37.5% ($1,500/$4,000), which is generally considered healthy. If your DTI were 55%, a lender might be hesitant, as adding an auto loan could strain your finances.

Step-by-Step Guide: Applying for Your Auto Loan

Securing an auto loan from a credit union is a straightforward process:

- Find a Credit Union: Use resources like the National Credit Union Administration (NCUA) website to locate credit unions you’re eligible to join.

- Become a Member: Once you’ve chosen a credit union, complete the membership application and make the required small deposit. This is your gateway to their services.

- Get Pre-Approved: Apply for a pre-approval before you start car shopping. This tells you how much you can borrow and at what interest rate, giving you significant negotiating power at the dealership.

- Compare Loan Offers: Don’t just settle for the first offer. Check rates from a few different credit unions and even banks to ensure you’re getting the best deal.

- Shop for Your Car: With your pre-approval in hand, you can focus on finding the right vehicle within your budget. You’ll know exactly what you can afford.

- Finalize the Loan: Once you’ve chosen your car, return to your credit union to complete the loan paperwork. They’ll typically work directly with the dealership to facilitate the purchase.

Understanding Your Loan: Key Terms & Concepts

Knowing these terms will empower you during the loan process:

- Annual Percentage Rate (APR): This is the total cost of borrowing money for one year, expressed as a percentage. It includes the interest rate plus certain fees. Why it matters: A lower APR means a cheaper loan overall.

- Loan Term: The length of time you have to repay the loan, usually expressed in months (e.g., 60 months, 72 months). Why it matters: A shorter loan term means higher monthly payments but less interest paid over time. A longer term means lower monthly payments but more total interest.

- Down Payment: An initial payment you make towards the purchase of the car, reducing the amount you need to borrow. Why it matters: A larger down payment reduces your loan amount, lowering your monthly payments and the total interest you’ll pay. It also builds immediate equity in the vehicle.

- Secured Loan: An auto loan is a secured loan, meaning the car itself acts as collateral. If you fail to make payments, the lender can repossess the vehicle. Why it matters: This reduces the risk for the lender, allowing them to offer lower interest rates than unsecured loans (like personal loans).

Calculating Your Potential Loan Costs

Understanding how your loan amount, interest rate, and term affect your monthly payment and total cost is crucial. While exact calculations can be complex, you can estimate using readily available tools. To get a sense of your monthly payment, you’d typically input the principal loan amount (car price minus down payment), the interest rate (APR), and the loan term in months into a loan calculator. It’s not just about the monthly payment; it’s about the total interest paid over the life of the loan.

Auto Loan from a Credit Union? Unlock Lower Rates

For example, if you borrow $20,000 at 5% APR over 60 months, the calculator will show you an estimated monthly payment and the total amount of interest you’d pay. Compare this to a 4% APR over 60 months to see the savings.

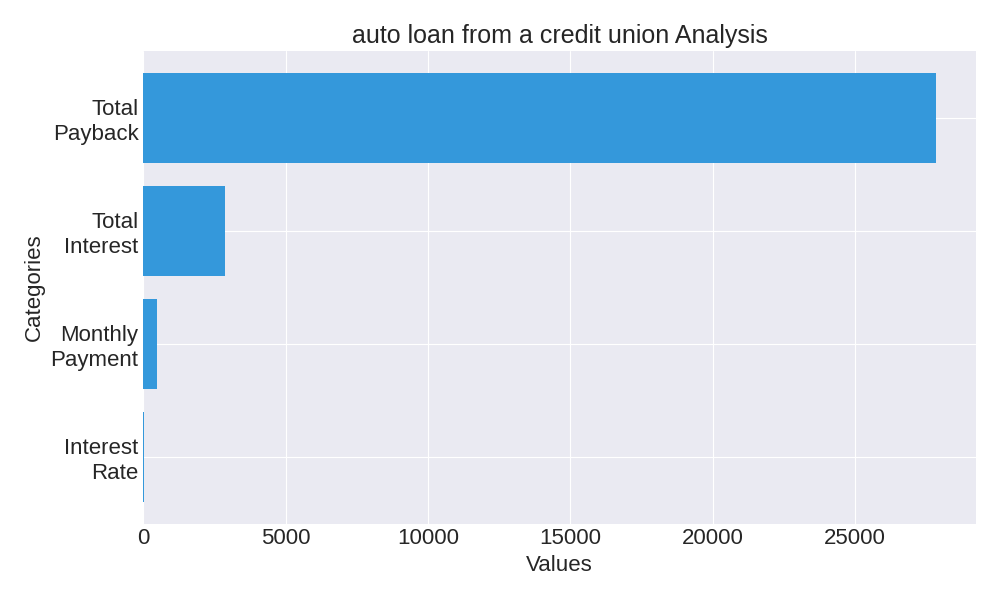

Total Cost Analysis: Credit Union vs. Traditional Lender

To illustrate the potential savings, let’s look at a hypothetical scenario for a $25,000 auto loan.

| Loan Feature | Credit Union (Scenario A) | Traditional Lender (Scenario B) |

|---|---|---|

| Loan Amount | $25,000 | $25,000 |

| Interest Rate (APR) | 4.25% | 6.75% |

| Loan Term | 60 Months | 60 Months |

| Estimated Monthly Payment | ~$464 | ~$493 |

| Estimated Total Interest Paid | ~$2,850 | ~$4,550 |

| Estimated Total Payback | ~$27,850 | ~$29,550 |

As you can see, even a seemingly small difference in APR can result in significant savings on your estimated total interest and overall payback amount, demonstrating the financial power of choosing a credit union.

Common Mistakes to Avoid

When applying for an auto loan, steer clear of these pitfalls:

- Not Getting Pre-Approved: Going to a dealership without pre-approval leaves you vulnerable to their financing offers, which may not be the best for you.

- Focusing Only on Monthly Payment: While important, don’t ignore the total cost of the loan. A lower monthly payment over a longer term often means paying much more interest.

- Accepting the First Offer: Always compare offers from multiple lenders to ensure you’re getting the most competitive rate.

- Ignoring Your Credit Score: A poor credit score can lead to higher rates. Check your score and address any errors before applying. You can often get a free credit report from consumerfinance.gov.

- Skipping the Fine Print: Always read the loan agreement carefully. Understand all fees, penalties, and terms before you sign.

FAQ: Your Auto Loan from a Credit Union Questions Answered

Q1: Is it harder to get an auto loan from a credit union than a bank?

Not necessarily. While you must become a member first, the actual lending criteria (credit score, income) are similar. Many members find credit unions more flexible, especially for those with less-than-perfect credit.

Q2: Can I get an auto loan from a credit union if I have bad credit?

It can be more challenging, but credit unions are often more willing to work with members with lower credit scores than traditional banks. They may offer slightly higher rates or require a larger down payment, but it’s worth exploring before going elsewhere.

Q3: How quickly can I get approved for a credit union auto loan?

Pre-approval can often happen within one to two business days, sometimes even faster, especially if you’re already a member. The full loan closing might take a few days once you’ve chosen your vehicle.

Q4: Do I need a down payment for a credit union auto loan?

While not always strictly required, making a down payment is highly recommended. It reduces your loan amount, lowers your monthly payments, and can help you qualify for better interest rates.

Q5: Can I refinance an existing auto loan with a credit union?

Absolutely! Many people refinance their existing auto loans with a credit union to take advantage of lower interest rates or better terms. This can save you a significant amount over your loan’s remaining life. Check out resources on refinancing at MyFICO for more information.

Conclusion

Choosing an auto loan from a credit union is a financially savvy decision for many car buyers. Their member-focused approach often translates into lower rates, flexible terms, and superior customer service, ultimately saving you money and stress. By understanding the process, knowing what to expect, and avoiding common pitfalls, you can confidently secure the best financing for your next vehicle.

Ready to drive away with a better deal? Explore credit union auto loan options today and discover how being a member can put you in the driver’s seat of your financial future.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.