You’re here because you’re stuck. Maybe an unexpected car repair hit, a medical bill blindsided you, or rent is due and your paycheck just isn’t stretching. You’ve heard about a loan with no credit check, and frankly, it sounds like your last hope. The traditional banking system shut you down, your credit score feels like a permanent scarlet letter, and the idea of another rejection is crushing. I get it. This isn’t about luxury; it’s about survival.

Let’s be clear: navigating the world of a loan with no credit check when your options feel limited requires a sharp mind and a strategic approach. You need cash, and you need it now, but you absolutely cannot afford to make your financial situation worse. I’m here to arm you with the insider knowledge to make the right decision, immediately. We’ll explore legitimate paths and expose the traps.

The Reality of “No Credit Check” Loans: What You Really Need to Know

When a lender promises a “no credit check” loan, it doesn’t mean they’re handing out money blindly. This is one of the biggest common myths to avoid. What it truly means is they aren’t pulling your FICO score or conducting a “hard” inquiry through the major credit bureaus (Equifax, Experian, TransUnion).

Why does this matter in real life? Because while it spares your credit score another potential ding, it doesn’t mean they don’t assess your risk. They simply use different, often less forgiving, criteria. Understanding this shift is your first step to making an informed decision.

How Lenders Really Assess Your Risk

These lenders still need to know you can repay the loan. They pivot their focus to other aspects of your financial life. This includes examining your current income, employment stability, and even your banking history.

Imagine you’re a gig worker with fluctuating income, say between $1,500 and $3,000 per month. A traditional bank might see inconsistency and shy away. However, a no-credit-check lender might look at consistent direct deposits, even if they vary, as proof of income. They might also require recent bank statements to verify your cash flow and ensure you don’t have excessive overdrafts.

Insider Tip: Many of these lenders will verify your identity and income through services that link to your bank account, giving them a real-time snapshot of your financial health. This process is less about your past credit mistakes and more about your present ability to repay. This offers a different avenue for you, but demands transparency on your part.

Your Best Options for a Loan with No Credit Check (or Minimal Checks)

Despite the high costs, sometimes these options are your only bridge to stability. It’s critical to understand each type’s mechanics, pros, and cons. Your goal is to secure the necessary funds without getting trapped in a cycle of debt.

Here are the primary avenues you might consider when seeking a loan with no credit check:

- Payday Loans: These are short-term, high-cost loans typically due on your next payday. They offer quick cash, often between $100-$1,000, without a traditional credit check. However, their fees translate into extremely high annual percentage rates (APRs), often 400% or more. The Consumer Financial Protection Bureau (CFPB) offers resources on understanding these loans and their risks, which you can explore at consumerfinance.gov.

- Pawn Shop Loans: You offer an item of value (jewelry, electronics) as collateral, and the pawn shop lends you money based on a percentage of its resale value. There’s no credit check, and if you don’t repay, you simply lose the item. The downside is that you might get much less than your item is worth, and interest rates can still be high.

- Car Title Loans: These loans use your vehicle’s title as collateral. You keep driving your car, but if you default, the lender can repossess it. They offer larger amounts than payday loans but come with significant risks, including very high interest rates and the potential loss of your transportation. This is a critical decision that could impact your livelihood.

- Installment Loans from “No Credit Check” Lenders: Some online lenders specialize in installment loans for bad credit. They typically offer more manageable repayment terms over several months, rather than a single lump sum. While they avoid hard credit checks, they still assess your income and ability to pay. Their APRs are high but generally lower than payday loans.

- Secured Personal Loans: Offered by traditional banks or credit unions, these loans require collateral, like a savings account or certificate of deposit (CD). Because your own assets secure the loan, the lender’s risk is minimal, often allowing for approval even with poor credit. This can be an excellent way to borrow and simultaneously improve your credit if the payments are reported.

- Credit Builder Loans: While not providing immediate cash in hand, a credit builder loan is designed to help you establish a positive payment history. The loan amount is typically held in a locked savings account, and you make payments over time. Once paid off, you get access to the funds. This is a long-term strategy but highly effective.

The Hidden Costs and Traps to Watch For

The allure of immediate cash without a credit check can blind you to the true costs. High interest rates are just the beginning. Many lenders also stack on fees: origination fees, late payment fees, or even fees for simply processing your payment.

In a real-life scenario, imagine you take out a $500 payday loan with a fee of $75 for a two-week period. That’s a 15% fee for just two weeks, translating to an APR well over 300%. If you can’t repay it in two weeks, you might “roll over” the loan, meaning you pay another $75 fee without reducing the principal. This cycle can quickly turn a small loan into an enormous, unmanageable debt, trapping you financially.

Pro Tip: Always read the fine print. Look for prepayment penalties, which can surprise you if you try to pay off the loan early. Understand if the lender reports payments to credit bureaus; if they don’t, even timely payments won’t help your score.

Calculating Your Loan’s True Cost

Understanding the true cost of a loan is your superpower against predatory lending. It’s not just about the upfront amount; it’s about what you’ll pay back over time. This crucial step prevents you from making a bad situation worse.

How to Calculate Your Loan’s True Cost

To calculate the total cost, start with the amount you’re borrowing, also known as the principal. Add all the fees the lender charges. This could be an origination fee, a processing fee, or specific service charges. Then, determine the total interest you’ll pay. For short-term loans, lenders often state this as a fee per $100 borrowed (e.g., $15 per $100). If it’s an annual percentage rate (APR), you’ll need to calculate the interest over the entire loan term.

Sum these three numbers: principal + total fees + total interest. That’s your total payback. For example, if you borrow $300 and the lender charges a $45 fee for a two-week period, your total payback is $345. If you roll it over, that fee could apply again, quickly doubling your cost without ever touching the original $300.

Calculate Your No-Credit-Check Loan Repayment

Estimated Monthly Payment: $0.00

Total Interest Paid: $0.00

Total Amount Repaid: $0.00

This simple calculation reveals the real impact on your wallet and helps you compare offers effectively.

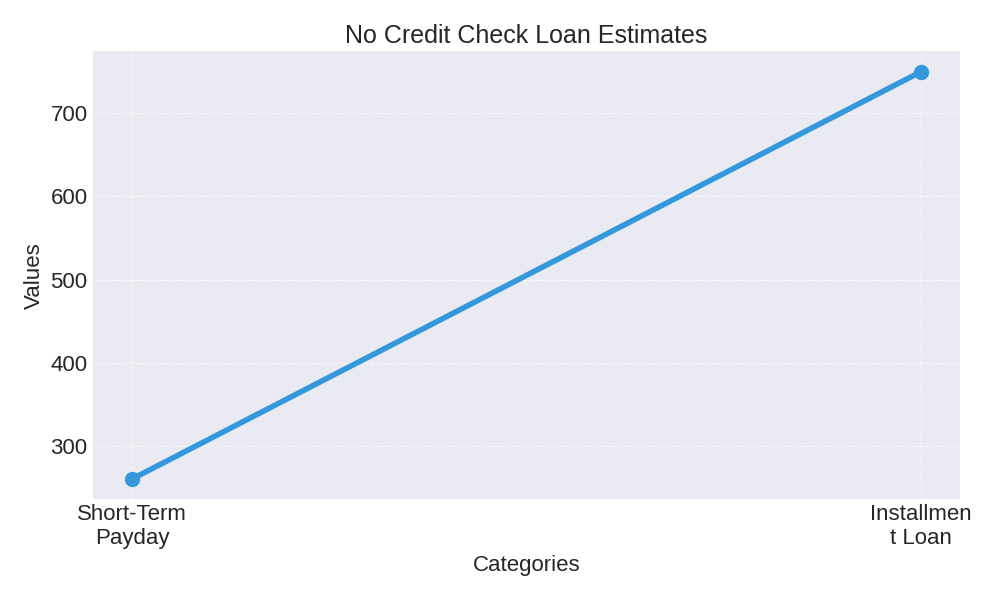

| Loan Type Example | Typical Loan Amount | Approx. Fees/Interest (Example) | Total Payback Estimate |

|---|---|---|---|

| Short-Term Payday Loan (2-4 weeks) | $200 – $500 | $30 – $75 per $100 borrowed | $260 – $875 |

| Installment Loan (3-6 months) | $500 – $2,000 | APR from 150% to 400%+ | $750 – $4,000 |

| Pawn Shop Loan (30 days, renewable) | 25% – 60% of item value | 2% – 25% monthly interest | Varies by item/renewal |

Navigating the Aftermath: Building Credit & Avoiding Traps

Getting a loan when your credit is challenged is often a temporary fix. Your ultimate goal should be to improve your financial standing so you have more options in the future. This requires a conscious effort to build a positive credit history.

Insider Tip: If you must take out a high-interest loan, focus on repaying it promptly. If the lender reports to credit bureaus (many no-credit-check lenders do not), this can eventually help your score. For long-term credit building, consider a secured credit card or a credit builder loan, which are designed specifically to help you establish positive payment history. You can learn more about managing your credit at myFICO.com.

Asking the Right Questions Before You Sign

Before you commit to any loan, especially one advertised as a loan with no credit check, empower yourself by asking these critical questions:

- What is the total amount I will pay back, including all fees and interest? Don’t just look at the monthly payment; demand the bottom line.

- What is the Annual Percentage Rate (APR)? This is the standardized measure of your loan’s cost over a year and makes comparing offers easier.

- Are there any prepayment penalties if I pay off the loan early? You want the flexibility to escape high interest sooner if your financial situation improves.

- Does this lender report my payments to the major credit bureaus? If the answer is no, this loan won’t help you build credit, only solve an immediate cash need.

- What happens if I miss a payment? Understand the late fees, interest accrual, and potential for default or repossession.

By asking these questions, you protect yourself from unexpected costs and predatory practices. The Federal Trade Commission (FTC) provides valuable guidance on avoiding scams and understanding consumer rights, which you can find at ftc.gov.

You have faced financial challenges, but you are not powerless. Securing a loan when your credit is struggling demands caution, research, and a clear understanding of the terms. Don’t let desperation drive you into a worse situation.

Take a deep breath, review your options, and use the knowledge gained here to protect yourself. Only accept terms you fully comprehend and can realistically meet. Your immediate decision today will impact your financial future.

Your Call to Action: Evaluate your true need, compare at least two loan offers using the “Total Cost Analysis,” and prioritize lenders that are transparent. If you’re unsure, consult a non-profit credit counselor before signing anything. Choose wisely to break free, not fall deeper.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.