Navigating the world of personal finance can feel daunting, but understanding your banking account options is a fundamental first step. Whether you’re saving for a big goal, managing daily expenses, or looking to grow your wealth, choosing the right banking account can significantly impact your financial health. This guide will demystify the different types of accounts, explain critical features, and help you make informed decisions to unlock your best financial future.

Having the right banking account isn’t just about where you keep your money; it’s about how effectively your money works for you. From minimizing fees to maximizing interest, a well-chosen banking account is a cornerstone of smart financial management. Let’s dive in and uncover the secrets to optimizing your banking choices.

Types of Banking Accounts Explained

Understanding the different kinds of banking accounts is crucial for managing your money effectively. Each type serves a distinct purpose, offering various features and benefits. Let’s explore the most common ones.

Checking Accounts: Your Daily Financial Hub

A checking account is designed for everyday transactions. It allows you to easily deposit and withdraw money, pay bills, and make purchases using a debit card or checks. These accounts prioritize accessibility over interest earnings.

Why this matters in real life: Imagine you’re a college student receiving your monthly allowance or part-time salary. A checking account lets you pay for textbooks, groceries, and utilities without carrying large amounts of cash. It’s the engine for your daily financial life, enabling quick and secure transactions.

Many checking accounts come with features like online bill pay and mobile deposits, making financial management convenient. However, be mindful of potential monthly maintenance fees or overdraft charges.

Savings Accounts: Building Your Financial Future

Savings accounts are primarily for storing money you don’t need immediately, helping you build an emergency fund or save for specific goals. They typically offer a modest interest rate, allowing your money to grow over time, albeit slowly.

Why this matters in real life: Picture a young couple saving for a down payment on their first home. By putting dedicated funds into a savings account, they earn a small amount of interest, making their money work for them while it accumulates. This separation from their daily checking account helps prevent accidental spending.

While savings accounts usually have withdrawal limits (e.g., six transfers or withdrawals per month), they are a safe place for your money, often insured by the FDIC.

Money Market Accounts (MMAs): A Hybrid Approach

Money market accounts blend features of both checking and savings accounts. They usually offer higher interest rates than standard savings accounts and provide limited check-writing privileges and debit card access.

Why this matters in real life: Consider a freelancer who has saved a substantial amount (say, between $10,000 and $20,000) for a future business investment but also needs occasional access. An MMA provides better interest earnings than a basic savings account while still offering flexibility for a few transactions a month. This balance makes it ideal for funds that are mostly for saving but might need occasional access.

MMAs often require a higher minimum balance to open and maintain compared to standard savings accounts. Failure to meet these minimums can result in fees.

Certificates of Deposit (CDs): Long-Term Savings with Higher Returns

CDs are time-deposit accounts where you agree to leave your money untouched for a fixed period (e.g., 6 months, 1 year, 5 years) in exchange for a higher, fixed interest rate. Withdrawing funds before the term ends usually incurs a penalty.

Why this matters in real life: Imagine an individual who just received a bonus of $5,000 and won’t need that money for three years. Investing it in a 3-year CD ensures a guaranteed return, often higher than a savings account, without the temptation to spend it. It’s a disciplined way to save for future goals like a car purchase or home renovation.

CDs are a secure investment, offering predictable returns, making them a good option for specific future savings goals.

How to Choose Your Ideal Banking Account

Selecting the best banking account involves more than just picking the first option you see. It requires careful consideration of your financial habits and goals. Here’s a step-by-step approach to make an informed choice.

-

Assess Your Financial Needs and Habits: Start by understanding how you use money. Do you make frequent transactions, or do you mostly save? Are you looking for high accessibility or the best interest rates? Your daily activities dictate the best account type. For example, if you typically make 20-30 debit card purchases a month, a robust checking account is essential.

Why this matters: Choosing an account that doesn’t align with your habits can lead to unnecessary fees or missed opportunities for growth. It’s about matching the tool to the task.

-

Compare Fees and Minimums: Banks often charge various fees, such as monthly maintenance fees, overdraft fees, ATM fees, and minimum balance fees. Research these carefully. Some accounts waive fees if you meet certain conditions, like direct deposit or a minimum average balance.

Why this matters: Even small fees can erode your savings over time. A $10 monthly fee adds up to $120 a year, which could instead be growing in your account. Always read the fine print.

-

Evaluate Interest Rates and Benefits: For savings, money market, and CD accounts, the interest rate (Annual Percentage Yield, or APY) is crucial. A higher APY means your money grows faster. Also, look for additional benefits like cash-back rewards on debit card purchases or sign-up bonuses for new accounts.

Why this matters: Over years, even a seemingly small difference in APY (e.g., 0.10% vs. 0.50%) can result in hundreds or thousands of dollars more in earnings, thanks to the power of compounding.

-

Consider Online vs. Traditional Banks: Online banks often offer higher interest rates and lower fees due to reduced overhead. Traditional banks provide in-person services, a wider ATM network, and personal relationship managers. Weigh these pros and cons based on your comfort level with digital banking.

Why this matters: If you value face-to-face interaction and cash deposits, a traditional bank might be better. If you prefer convenience and higher returns, an online bank could be your ideal choice. Your preference impacts your day-to-day banking experience.

-

Review Customer Service and Digital Tools: Good customer service is invaluable when you encounter issues. Check reviews and consider the quality of their mobile app, online banking platform, and customer support channels (phone, chat). A user-friendly digital experience can simplify your financial life.

Why this matters: Frustrating banking apps or unresponsive customer service can turn simple tasks into headaches. A smooth digital experience saves you time and stress, making managing your banking account effortless.

Understanding Fees and Interest Rates

The financial world has its own language, especially when it comes to costs and earnings. Knowing the difference between an APR and an APY, and how various fees impact your balance, is essential.

Common Fees: Monthly maintenance fees can sometimes be avoided by maintaining a minimum balance or setting up direct deposit. Overdraft fees occur when you spend more money than you have in your account. ATM fees can be charged by both your bank and the ATM owner if you use an out-of-network machine.

Interest Rates: For deposit accounts, you’ll often see an Annual Percentage Yield (APY). This rate reflects the total interest earned on an account over a year, taking into account the effects of compounding interest. Compounding means you earn interest not only on your initial deposit but also on the accumulated interest from previous periods.

Mini case study: Imagine you deposit $1,000 into a savings account with a 0.50% APY. After one year, you’d earn about $5 in interest. Now, consider a CD with a 2.00% APY. On that same $1,000, you’d earn around $20 in a year. While these numbers might seem small initially, over many years and with larger deposits, the difference becomes significant, illustrating the power of higher interest rates.

The Importance of FDIC Insurance

When you deposit money into a bank, you want assurance that it’s safe. This is where FDIC insurance comes into play. The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects depositors in the event of a bank failure.

Why it matters: FDIC insurance covers up to $250,000 per depositor, per insured bank, for each account ownership category. This means if your bank were to fail, you wouldn’t lose your insured deposits. It provides a vital safety net, giving you peace of mind that your money is secure, even in turbulent economic times.

Always ensure your chosen financial institution is an FDIC-insured bank. You can verify a bank’s FDIC insurance status on the FDIC official website.

Practical “How to Calculate”

Understanding how your money can grow (or shrink) is key. Let’s look at how to estimate potential growth from interest and the impact of fees.

Estimating Compound Interest for Savings

You don’t need complex formulas to grasp compound interest. Think of it like this: You deposit money, and it earns a little bit of interest. Then, next period, you earn interest not just on your original money, but also on the interest you’ve already earned. It’s like your money having babies that also earn money!

To get a rough idea: take your starting balance, multiply it by your interest rate (as a decimal, e.g., 1% is 0.01) for one period. Add that interest to your balance. Then, for the next period, repeat the process with your new, slightly larger balance. Over many years, this snowball effect becomes very powerful.

For example, if you have $10,000 in a savings account with a 2% annual interest rate, you’d earn $200 in the first year. In the second year, you’d earn interest on $10,200, making slightly more than $200. This continuous growth is why starting early is so beneficial.

Banking Account Secrets Unlock Your Best Option

Estimating Total Fees Over Time

Calculating the impact of fees is simpler: just add them up. If your checking account has a $5 monthly maintenance fee and you don’t meet the waiver conditions, that’s $5 every month. Over a year, that’s $5 multiplied by 12 months, totaling $60. If you typically incur $30 in overdraft fees twice a year, that’s an additional $60 annually.

Why this matters: These costs directly reduce the money available to you. Understanding and minimizing fees is just as important as maximizing interest earnings.

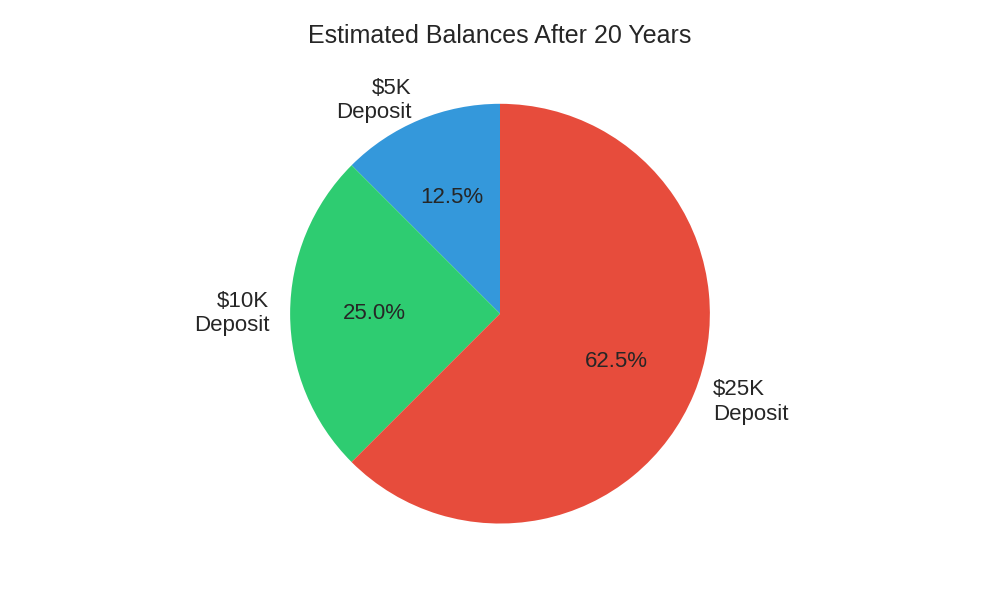

Here’s a simplified illustration of how compound interest can grow your savings over time with hypothetical example ranges:

| Initial Deposit | Annual APY (Range) | Estimated Balance (Year 5) | Estimated Balance (Year 10) | Estimated Balance (Year 20) |

|---|---|---|---|---|

| $5,000 | 1.0% – 2.0% | $5,250 – $5,500 | $5,500 – $6,100 | $6,100 – $7,400 |

| $10,000 | 1.0% – 2.0% | $10,500 – $11,000 | $11,000 – $12,200 | $12,200 – $14,800 |

| $25,000 | 1.0% – 2.0% | $26,250 – $27,500 | $27,500 – $30,500 | $30,500 – $37,000 |

Note: These are illustrative figures and do not include additional deposits or withdrawals. Actual results will vary based on specific APY, compounding frequency, and tax implications.

Frequently Asked Questions (FAQ)

We’ve covered a lot, but here are answers to some common questions you might still have about managing your banking accounts.

What is the difference between APR and APY?

APR (Annual Percentage Rate) typically refers to the cost of borrowing money (like on a loan or credit card) over a year, not including compounding. APY (Annual Percentage Yield) refers to the amount of interest you earn on a deposit account over a year, taking compounding into account. For your savings, APY is the more relevant number to compare.

Can I have multiple banking accounts?

Yes, absolutely! Many people have a checking account for daily spending and a separate savings account for long-term goals. This helps with budgeting and prevents you from accidentally spending your savings. Some even have a money market account for larger emergency funds.

How often should I review my banking account statements?

It’s a good practice to review your statements at least once a month. This helps you track spending, catch any unauthorized transactions, and ensure you’re not incurring unexpected fees. Staying informed about your account activity is a key part of financial hygiene.

Are online-only banks safe?

Yes, reputable online-only banks are just as safe as traditional banks, provided they are FDIC-insured. The Consumer Financial Protection Bureau (CFPB) offers resources on choosing a safe financial institution. They use advanced security measures and typically pass savings from lower overhead onto customers in the form of higher interest rates or lower fees.

What should I do if I notice an error on my statement?

Contact your bank immediately. Most banks have a process for disputing errors. Gather any supporting documentation you have, such as receipts or transaction records, to help resolve the issue quickly. Acting fast is important for protecting your funds.

Conclusion

Choosing and managing your banking account doesn’t have to be a mystery. By understanding the different types of accounts, evaluating fees and interest, and prioritizing security through FDIC insurance, you can make powerful decisions for your financial well-being. Your banking account is more than just a place to keep money; it’s a tool for achieving your financial aspirations.

Unlock Your Best Option Today!

Now that you’re equipped with this comprehensive knowledge, take the first step towards optimizing your finances. Review your current banking accounts, compare options, and choose the services that best fit your lifestyle and goals. Don’t let your money sit idly; make it work smarter for you. Explore options from various institutions and make an informed decision to secure your financial future. You can start by checking out reputable financial news and analysis platforms for current banking offers, such as Bloomberg.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.