Purchasing a new car is an exciting milestone, but the financial commitment requires careful planning. One of the most critical steps in this process is to calculate loan for car payments, ensuring your new vehicle fits comfortably within your budget. Understanding your potential monthly obligation empowers you to make informed decisions, avoid financial strain, and ultimately enjoy your new ride worry-free. This comprehensive guide will break down everything you need to know about car loan calculations, starting from the very basics.

Whether you’re a first-time car buyer or looking to upgrade, mastering how to calculate loan for car payments is essential for financial literacy. It helps you compare different loan offers, negotiate effectively, and budget for the true cost of vehicle ownership. Let’s dive in and demystify the process.

Understanding Car Loans: The Basics

A car loan is a type of secured loan specifically used to purchase a vehicle. When you take out a car loan, a lender (like a bank, credit union, or dealership) provides you with the funds to buy the car, and in return, you agree to repay that amount, plus interest, over a set period. The car itself often serves as collateral for the loan.

What is a Car Loan?

Simply put, a car loan is an agreement between you and a lender. The lender gives you money for the car, and you promise to pay it back. This repayment is typically done through fixed monthly installments over a specific duration. Failing to make these payments can result in the lender repossessing the vehicle.

Key Components of a Car Loan

To accurately calculate loan for car payments, you need to understand its fundamental building blocks:

- Principal: This is the initial amount of money you borrow to purchase the car. It’s the sticker price minus any down payment, trade-in value, or rebates.

- Interest Rate: Expressed as a percentage, the interest rate is the cost of borrowing the principal. It’s what the lender charges you for providing the funds. A lower interest rate means you pay less over the life of the loan.

- Loan Term: Also known as the repayment period, this is the length of time (in months or years) you have to pay back the loan. Common terms range from 36 to 84 months. A longer term often means lower monthly payments but typically results in more total interest paid over time.

Factors Influencing Your Monthly Payment

Several variables come into play when determining your monthly car loan payment. Understanding these can help you strategize for a more affordable outcome.

Loan Amount

The more money you borrow, the higher your monthly payment will be, assuming all other factors remain constant. Reducing your loan amount through a larger down payment or a valuable trade-in is a direct way to lower your monthly expense.

Interest Rate

The interest rate is a significant determinant of your payment. Even a small difference in the interest rate can lead to substantial savings or additional costs over the life of the loan. Your creditworthiness is a primary factor in the interest rate you’ll be offered.

Loan Term

A longer loan term stretches your payments over more months, making each individual payment smaller. However, this convenience often comes at the cost of paying more in total interest. Conversely, a shorter term results in higher monthly payments but less total interest paid.

Down Payment

A down payment is an upfront sum of money you pay towards the car’s purchase price. Making a substantial down payment reduces the principal amount you need to borrow, thereby lowering your monthly payments and the total interest you’ll pay. Many financial experts recommend a down payment of at least 10-20% for new cars.

Trade-in Value

If you’re trading in your old vehicle, its value can be applied directly to the purchase of your new car, effectively acting like an additional down payment. This reduces the amount you need to finance and consequently lowers your monthly payments.

Credit Score

Your credit score is one of the most critical factors influencing the interest rate you qualify for. Lenders use your credit score to assess your risk as a borrower. A higher credit score signals lower risk, often resulting in more favorable, lower interest rates. Conversely, a lower score may lead to higher rates or even loan denial.

Step-by-Step Guide to Calculate Your Car Loan Payment

While complex formulas exist, the easiest way to determine your payment is through online calculators or by understanding the basic logic. Here’s a practical approach:

Step 1: Determine the Total Amount to Borrow

Start with the car’s purchase price. Subtract any down payment you plan to make and the value of any trade-in. Add any relevant fees that will be rolled into the loan, such as sales tax (if financed) and registration fees. This gives you your principal loan amount.

Step 2: Research Interest Rates

Before heading to the dealership, get pre-approved for a loan from a bank or credit union. This gives you a benchmark interest rate. Your actual rate will depend on your credit score and the current market conditions. For general understanding of consumer credit, you can refer to resources from the Federal Reserve.

Step 3: Choose Your Loan Term

Consider your budget and financial goals. A shorter term saves money on interest but means higher monthly payments. A longer term offers lower monthly payments but increases the overall cost. Balance affordability with the desire to pay off the loan quickly.

Step 4: Use a Loan Calculator (or understand the logic)

Most financial websites offer free car loan calculators. These tools allow you to input your principal amount, interest rate, and loan term to instantly get your estimated monthly payment. The underlying logic is that your payment combines a portion of the principal and a portion of the interest due for that month, calculated to fully amortize the loan by the end of the term.

Sample Repayment Scenario & Table

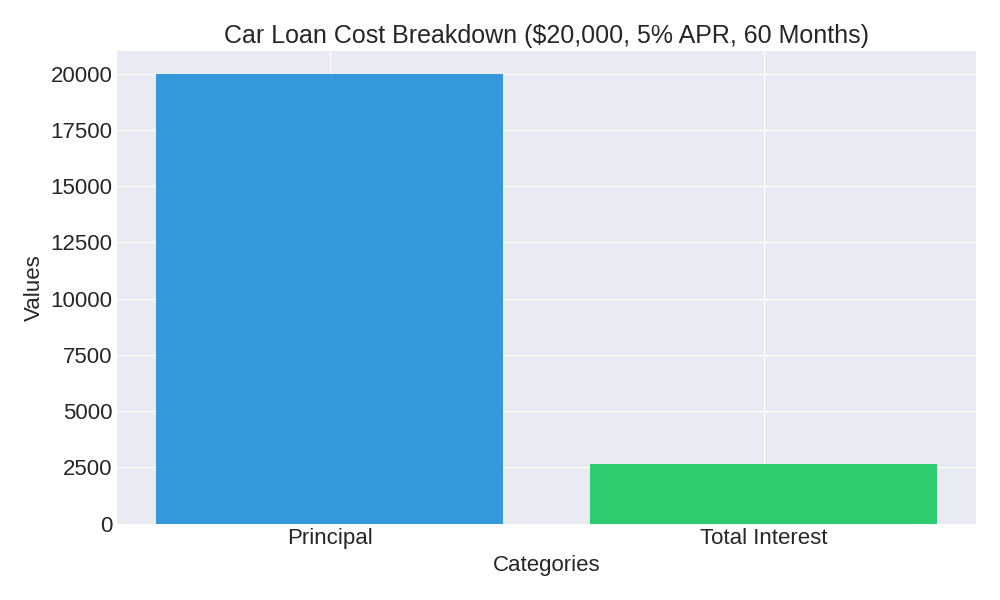

Let’s illustrate with an example. If you borrow $20,000 for a car at an annual interest rate of 5% over a 60-month (5-year) loan term, your monthly payment will be approximately $377.42. Over the course of the loan, you will pay back the $20,000 principal plus an additional amount in interest. This table demonstrates how the loan balance decreases over time with each payment:

| Year | Remaining Balance | Monthly Payment |

|---|---|---|

| Initial | $20,000.00 | – |

| 1 | $16,423.86 | $377.42 |

| 2 | $12,674.30 | $377.42 |

| 3 | $8,740.10 | $377.42 |

| 4 | $4,591.95 | $377.42 |

| 5 (Final) | $0.00 | $377.42 |

Monthly Payment Calculator

Beyond the Monthly Payment: Understanding the Total Cost

While the monthly payment is crucial for budgeting, it’s equally important to consider the total cost of the loan over its entire term. This includes the principal borrowed plus all the interest you’ll pay. A longer loan term might make monthly payments more manageable but often leads to significantly more interest paid in the long run.

Total Interest Paid

In our example of a $20,000 loan at 5% over 60 months, the total payments would be approximately $22,645.20 ($377.42 x 60 months). This means you would pay $2,645.20 in interest alone. Always look at the total interest to understand the true expense of financing your car. This can highlight the benefit of a higher down payment or shorter loan term.

Other Fees to Consider

Remember that the purchase price of a car extends beyond just the loan amount. You’ll also encounter other costs:

- Sales Tax: Most states levy a sales tax on vehicle purchases. This can be a significant amount, often financed into the loan or paid upfront.

- Registration Fees: Fees for registering your vehicle with the state’s Department of Motor Vehicles (DMV) are annual or biennial.

- Documentation Fees: Dealerships often charge a “doc fee” for processing paperwork. These vary by state and dealership.

- Insurance: Car insurance is a mandatory and ongoing cost that is separate from your loan payment.

Frequently Asked Questions (FAQ)

Can I lower my monthly car payment?

Yes, several strategies can help lower your monthly payment. You can increase your down payment, choose a longer loan term (though this increases total interest), secure a lower interest rate through a better credit score or refinancing, or opt for a less expensive vehicle.

What is a good interest rate for a car loan?

A “good” interest rate depends on your credit score, the current economic environment, and the loan term. Generally, rates below 5-6% are considered excellent for borrowers with good to excellent credit. You can check current average rates on financial news sites like Bankrate.

Should I make a large down payment?

Making a larger down payment can reduce your monthly payments and the total interest paid over the life of the loan. It may also improve your chances of approval and help you avoid owing more than the car’s value. However, be sure not to deplete your emergency savings entirely.

Can I get a car loan with bad credit?

Yes, car loans are available for borrowers with bad or limited credit, though interest rates are typically higher. Some lenders specialize in subprime auto loans, and a larger down payment or co-signer can improve terms. It’s important to compare offers carefully.

Is it better to finance through a bank, credit union, or dealership?

Each option has pros and cons. Banks and credit unions often offer lower interest rates, while dealerships provide convenience and promotional offers. Getting pre-approved before visiting a dealership can give you stronger negotiating power.

Can refinancing lower my car loan payment?

Refinancing can lower your monthly payment if your credit score has improved or interest rates have dropped. It may also allow you to adjust your loan term. Always compare the new loan’s total cost to ensure refinancing truly saves money.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.