Imagine the unthinkable: you’re involved in a car accident. Even a minor fender-bender can quickly escalate into a financial nightmare. This is precisely why understanding and having adequate liability insurance on car policies is not just a good idea, it’s a legal and financial imperative. Without proper car liability insurance, you could be on the hook for tens or even hundreds of thousands of dollars in damages and legal fees, potentially wiping out your savings or even your future earnings. This guide will demystify liability insurance, explain its critical role, and help you ensure you’re adequately protected every time you hit the road.

What is Car Liability Insurance?

Car liability insurance is designed to protect you financially if you’re at fault in an accident. It doesn’t cover damages to your own vehicle or your own injuries; instead, it covers the costs you’re legally responsible for causing to other people or their property. Think of it as a safety net that protects your assets.

For example, if you accidentally rear-end another car, your liability insurance would pay for the repairs to the other driver’s vehicle and their medical expenses, up to your policy limits. Without it, you’d have to pay these costs out of your own pocket. This matters in real life because it prevents a single accident from leading to catastrophic personal debt.

Why is Car Liability Insurance Legally Required?

Every state in the U.S., except New Hampshire, mandates that drivers carry a minimum amount of car liability insurance. This isn’t just bureaucracy; it’s a critical measure to protect everyone on the road. The government wants to ensure that if you cause an accident, the victims have a way to be compensated for their losses.

Imagine a scenario where no one had liability insurance. After an accident, injured parties might struggle to get their medical bills paid or their cars repaired, leading to lawsuits and significant financial hardship across society. This requirement ensures a basic level of financial responsibility and protection for all drivers and passengers. You can often find specific requirements from your state’s Department of Motor Vehicles or equivalent authority. For instance, the National Association of Insurance Commissioners (NAIC.org) offers resources on state insurance departments.

The Two Pillars: Bodily Injury and Property Damage

Liability insurance is split into two main components, each addressing different types of damage:

- Bodily Injury Liability (BIL): This covers the costs associated with injuries to other people involved in an accident where you are at fault. This can include medical expenses, lost wages from time off work, pain and suffering, and even funeral costs in severe cases.

- Property Damage Liability (PDL): This covers the costs of damage you cause to someone else’s property. Most commonly, this means repairing or replacing another vehicle, but it can also cover damage to fences, mailboxes, buildings, or other structures you might hit.

Why does this matter in real life? Consider a situation where you swerve and hit a luxury vehicle, causing significant damage, and its driver sustains a severe injury requiring surgery. Your bodily injury liability would cover their medical bills, and your property damage liability would cover the cost of repairing their expensive car. These combined costs can quickly skyrocket, making robust coverage essential.

Understanding Your Coverage Limits

When you look at your policy, you’ll often see liability limits expressed as three numbers, like “25/50/25”. These numbers represent the maximum amounts your insurance company will pay out in an at-fault accident:

- First number ($25,000): Maximum coverage for bodily injury per person.

- Second number ($50,000): Maximum coverage for bodily injury per accident, regardless of how many people are injured.

- Third number ($25,000): Maximum coverage for property damage per accident.

A mini case study: Imagine you’re in an accident that causes $35,000 in injuries to one person and $15,000 in damage to their car. If your policy is 25/50/25, your insurance would pay $25,000 for the bodily injury (the per-person limit) and $15,000 for the property damage. You would still be personally responsible for the remaining $10,000 in medical bills. This matters because minimum limits are often woefully inadequate for serious accidents, leaving you vulnerable to significant out-of-pocket expenses.

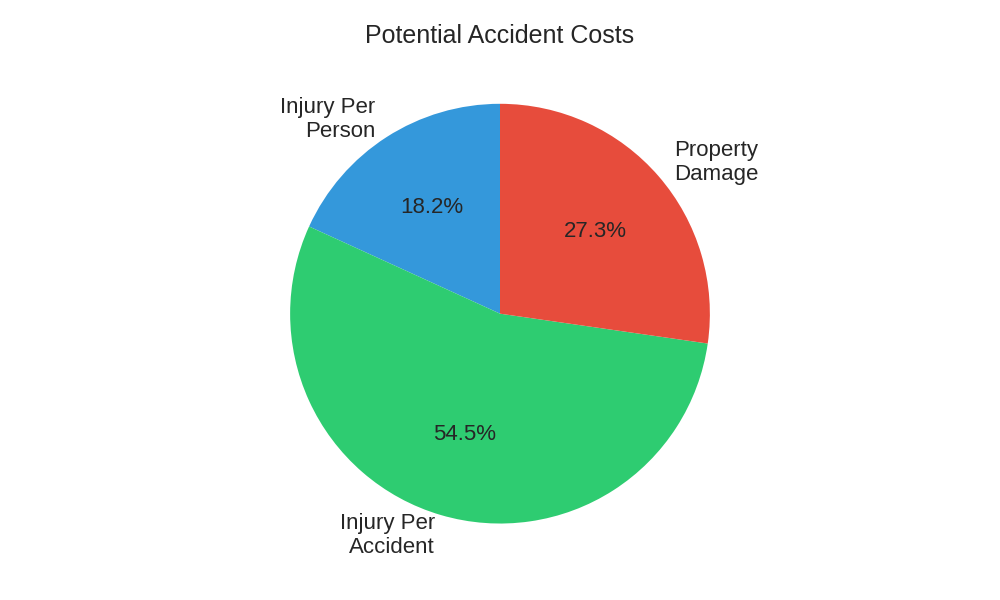

| Coverage Type | Typical State Minimum Example | Recommended Higher Coverage | Potential Accident Costs (Scenario) |

|---|---|---|---|

| Bodily Injury (per person) | $25,000 | $100,000 – $250,000 | $50,000 (moderate injury) |

| Bodily Injury (per accident) | $50,000 | $300,000 – $500,000 | $150,000 (multiple injuries) |

| Property Damage (per accident) | $25,000 | $50,000 – $100,000 | $75,000 (luxury vehicle + property) |

How to Calculate Your Ideal Liability Coverage

Calculating the “right” amount of liability insurance isn’t about a magic formula; it’s about assessing your financial risk. A good rule of thumb is to carry enough liability insurance to cover your total net worth. This includes the value of your savings, investments, and equity in your home, excluding retirement accounts.

Consider your financial situation: If you have significant assets, like a home or substantial savings, you’ll want higher limits. If you cause a severe accident and your insurance limits are exceeded, victims can sue you personally for the difference. This matters because higher coverage acts as a shield for your hard-earned assets.

Here’s a practical way to think about it:

- Add up your assets: List the total value of your bank accounts, investment portfolios, and any equity in real estate.

- Consider your income: If you earn a high income, future wages could be garnished in a lawsuit.

- Factor in your driving habits: Do you drive frequently? Do you commute in heavy traffic? More driving can mean higher exposure to risk.

- Think about where you live: Some areas have higher accident rates or higher costs for repairs and medical care.

- Match coverage to risk: Aim for limits that align with or exceed your total financial exposure.

You can also use online tools to help estimate coverage needs.

Car Accident Financial Risk (Uninsured)

Steps to Choose the Right Policy

Selecting the best liability insurance on car policy involves more than just picking the cheapest option. Follow these steps to make an informed decision:

- Assess Your Needs: Based on the “How to Calculate” section, determine your ideal bodily injury and property damage limits. Don’t just settle for state minimums.

- Gather Quotes: Contact multiple insurance providers. Online comparison tools can be helpful, but also speak directly with agents who can explain coverage options. Compare not just price, but also customer service and claims processing reputation.

- Understand Discounts: Ask about potential discounts. These could be for good driving, bundling policies (auto and home), good student status, or vehicle safety features.

- Read the Fine Print: Before signing, carefully review the policy document. Understand what is and isn’t covered, and be aware of any exclusions.

- Review Annually: Your life changes, and so should your insurance. Review your policy at least once a year or after major life events (new car, new driver, marriage, moving).

This process matters because it ensures you’re not just buying insurance, but buying the right protection for your unique circumstances. For further guidance on choosing an insurer, resources like ConsumerReports.org often provide valuable insights and reviews.

Common Misconceptions About Liability Insurance

Many drivers have misunderstandings about what liability insurance actually covers:

- “Full Coverage” Covers Everything: The term “full coverage” is misleading. It typically means you have liability, collision, and comprehensive insurance. While comprehensive and collision cover your car, liability only covers damages you cause to others. It doesn’t mean you’re covered for every possible scenario.

- Minimum Coverage is Enough: As discussed, state minimums are rarely sufficient to cover the costs of a serious accident. Relying solely on minimums leaves your personal assets exposed.

- My Health Insurance Will Cover Me in an At-Fault Accident: While your health insurance might cover your own medical bills, it won’t cover the medical bills of other people you injure. That’s where bodily injury liability comes in.

Why this matters: These misconceptions can lead to dangerous gaps in coverage, leaving you personally responsible for huge financial burdens after an accident.

Frequently Asked Questions (FAQ)

- Q: What if someone else drives my car and gets into an accident? Am I covered?A: Generally, car insurance follows the car, not the driver. So, your liability policy would likely cover damages if you give permission for someone else to drive your car. However, there can be exceptions, so always check with your insurer.

- Q: Does my liability insurance cover me if I hit an animal?A: No. Hitting an animal falls under your comprehensive coverage, not liability. Liability only covers damage you cause to other people or their property.

- Q: How can I lower my liability insurance premiums?A: You can often lower premiums by maintaining a good driving record, taking defensive driving courses, raising your deductible (for collision/comprehensive, not liability itself), bundling policies, and asking about various discounts. Increasing your liability limits sometimes offers disproportionately low cost increases for significantly more protection.

- Q: What happens if I drive without liability insurance?A: Driving without required liability insurance can result in severe penalties, including fines, license suspension, vehicle impoundment, and even jail time in some states. If you cause an accident, you’ll be personally responsible for all damages and could face lawsuits. Learn more about the implications of driving uninsured from financial news sources like Forbes.com.

Car liability insurance is more than just a legal requirement; it’s a fundamental pillar of responsible driving and personal financial protection. It shields your assets from the unpredictable costs of accidents, ensuring that a moment of misfortune doesn’t derail your financial future.

Don’t wait for an accident to discover you’re underinsured. Take the time to understand your policy, assess your needs, and choose coverage that truly protects you. Review your current policy today, get quotes from different providers, and drive with the peace of mind that you’re adequately covered. Your financial well-being depends on it.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.