The crushing weight of high car insurance premiums is real. You’re probably tired of feeling like you’re just another number, paying too much for coverage you barely understand. Finding the right car insurance near me can feel like navigating a maze blindfolded, especially when every online quote seems to vary wildly. You want to make an informed decision, quickly, and stop overpaying.

As your advocate, I’m here to tell you that you don’t have to settle. We’re going to cut through the noise, expose the hidden factors, and equip you with the insider knowledge to truly compare car insurance near me options and secure your best local rate – starting right now. Let’s make sure your money stays in your pocket.

Stop Overpaying: The Local Factor in Car Insurance

It’s not just your driving record that dictates your rates; your location is a massive, often overlooked, pricing lever. Imagine two identical drivers with perfect records, driving the same car. One lives in a bustling urban zip code with high accident rates and car theft, while the other lives in a quiet rural town. Their premiums for identical coverage could differ by hundreds, even thousands, of dollars annually. This is why knowing how local factors impact your car insurance near me rates is critical.

Why this matters in real life: Insurers assess risk at a micro-level. If your neighborhood has higher claims for vandalism, deer collisions, or even frequent hailstorms, everyone in that area pays a collective premium for that increased risk. You need to understand that the local claim history, repair costs, and even traffic density directly translate to your personal premium.

Insider Tip: Don’t just get a quote based on your current address. If you’re considering a move, even a few miles away, check insurance rates for the potential new zip code before signing a lease or buying a home. A different neighborhood could significantly lower your premium.

Decoding Your Coverage: What You Actually Need (and Don’t)

You’re not just buying a piece of paper; you’re buying financial protection. The fear of being underinsured after an accident is legitimate, but so is the fear of paying for coverage you don’t truly need. Understanding the core types of coverage is crucial, and it’s simpler than insurers make it seem.

- Liability Coverage: This is non-negotiable and legally required in almost every state. It covers damage and injuries you cause to others. Think of it as protecting your assets if you’re at fault in an accident.

- Collision Coverage: This pays for damage to your own car if you hit another vehicle or object. If your car is older or paid off, you might consider if the premium is worth it given its actual cash value.

- Comprehensive Coverage: This covers non-collision damage – theft, vandalism, fire, weather events. If your car is parked outdoors or in an area prone to such incidents, this coverage is invaluable.

- Uninsured/Underinsured Motorist (UM/UIM): A critical, often overlooked, layer of protection. This covers your medical bills and car repairs if you’re hit by someone who doesn’t have insurance or enough insurance. In a typical scenario, if you’re hit by an uninsured driver and have major injuries, UM/UIM protects you from devastating out-of-pocket costs.

Why this matters in real life: Choosing the right balance ensures you’re protected without wasting money. For instance, if you have an older car worth less than, say, $3,000, paying a high premium for collision and comprehensive might not make financial sense, especially if your deductibles are also high. For more in-depth explanations on coverage, check out resources like the Insurance Information Institute.

The “How-To” of Smart Comparison: Beyond the Online Form

Simply plugging your info into one or two online comparison sites isn’t enough. That’s a common myth. These sites often don’t have every insurer, and their quotes can sometimes be estimates. You need a multi-pronged approach to get the absolute best rate.

Common Myths to Avoid:

- Myth 1: “Comparison sites show every option.” Many smaller, regional insurers and some national carriers don’t participate. You could be missing out on a local gem.

- Myth 2: “Loyalty always pays off.” While some insurers offer loyalty discounts, staying with the same company for years without shopping around almost guarantees you’re overpaying.

- Myth 3: “All quotes are created equal.” Make sure you’re comparing identical coverage limits and deductibles across all quotes. A lower premium might just mean less protection.

Insider Tips for Deeper Comparison:

- Contact Local Agents: Independent local agents work with multiple insurers and can often find deals not available through direct online quotes. They know the local market and specific nuances better than any algorithm.

- Bundle Policies: If you have home, renters, or life insurance, ask about bundling discounts. Many insurers offer significant savings (sometimes 10-25%) for combining policies.

- Call Direct: After getting online quotes, call the top 2-3 companies directly. Sometimes, speaking with a representative can unlock additional discounts or provide clearer explanations.

Practical Calculation: Estimating Your True Insurance Cost

Your true insurance cost isn’t just your monthly premium. It’s what you pay PLUS what you could pay out of pocket. To estimate this, consider your annual premium, plus your chosen deductible for collision and comprehensive. If you have an incident, you’ll pay that deductible. For example, if your annual premium is $1,200 and your deductible is $500, your immediate cost in an accident is your premium plus the deductible. You should weigh how often you’d realistically claim against how much you’d save with a higher deductible.

Your Potential Local Car Insurance Savings

A higher deductible lowers your premium but increases your out-of-pocket risk if you have an accident. Conversely, a lower deductible means higher premiums but less cash needed upfront for a claim. Find a balance that suits your emergency fund and risk tolerance.

Unmasking Discounts: Are You Leaving Money on the Table?

Discounts are where serious savings hide. You’re probably aware of good driver discounts, but there’s a whole world of lesser-known ways to slash your premium. Don’t be shy; ask every single insurer what discounts they offer.

- Low Mileage: If you work from home or use public transport, tell your insurer. Driving less often means less risk.

- Defensive Driving Course: Completing an approved course can lead to discounts, especially for younger or older drivers.

- Good Student Discount: If you have a driver on your policy who maintains good grades (typically a B average or higher), you could qualify.

- Professional/Affiliation Discounts: Many insurers offer discounts for members of certain professional organizations, alumni associations, or even credit unions. Always ask!

- Telematics/Usage-Based Insurance: Companies like Progressive (Snapshot) or State Farm (Drive Safe & Save) offer devices or apps that monitor your driving habits. Safe drivers can see significant savings. This can be a game-changer if you have excellent driving habits.

Why this matters in real life: These discounts aren’t just minor adjustments; they can cumulatively reduce your premium by 15-30% or more. Failing to ask means you’re literally paying more than you have to.

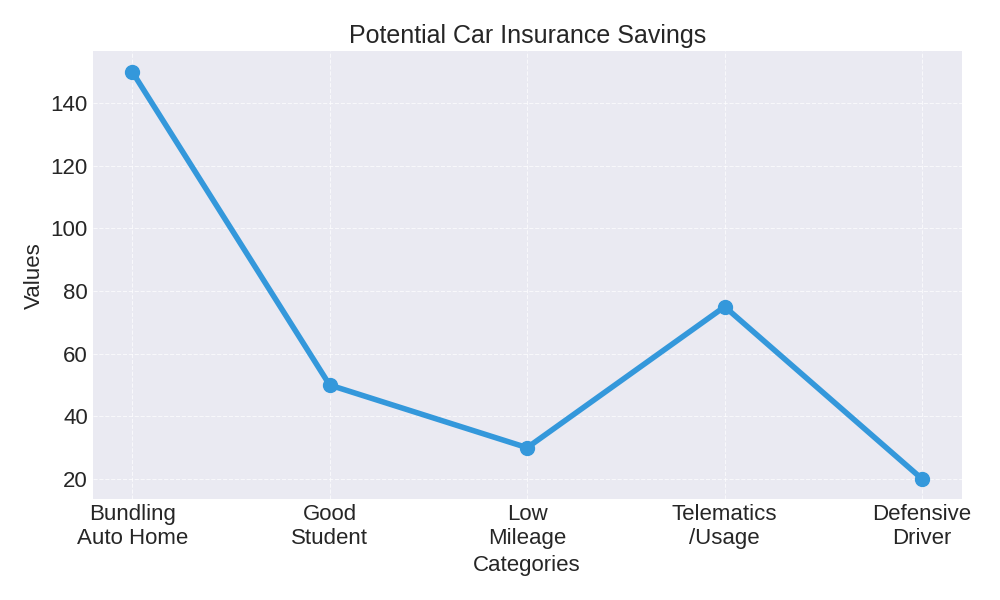

Potential Car Insurance Savings Scenarios

| Discount Type | Scenario Driver Profile | Estimated Annual Savings Range |

|---|---|---|

| Bundling (Auto + Home) | Homeowner with multiple policies | $150 – $400 |

| Good Student | Teen driver with B average or higher | $50 – $250 |

| Low Mileage | Driver commuting less than 7,500 miles/year | $30 – $180 |

| Telematics/Usage-Based | Safe driver with consistent habits | $75 – $300 |

| Defensive Driver Course | Driver completing approved course | $20 – $100 |

For additional consumer protection resources and advice on insurance, you might find the Federal Trade Commission website helpful.

When to Switch (and How to Do It Right)

The best time to shop for new car insurance is before your current policy renews. Aim to get quotes about 4-6 weeks out. But there are other triggers:

- Major Life Events: Getting married, moving, buying a new car, or adding a teen driver. Each of these changes your risk profile and can drastically alter rates.

- Annual Review: Even if nothing changes, make it a habit to shop around every 1-2 years. Rates change constantly, and a new insurer might offer you a better deal.

- Rate Increase: If your current insurer suddenly hikes your premium without a clear reason (like an accident or ticket), it’s a huge red flag to start shopping.

Common Myth to Avoid: “It’s too much of a hassle to switch.” The process is streamlined. You don’t need to break up with your old insurer before finding a new one. In fact, it’s safer not to.

Insider Tip for a Smooth Switch: Don’t cancel your old policy until your new one is active and confirmed. Aim for a small overlap (even just a day) to ensure there are no gaps in coverage. This avoids potential fines or complications if you have an accident during the transition. You’ll often receive a prorated refund from your old insurer for any unused premium. For more insights on switching, sites like NerdWallet often provide helpful guides.

Conclusion: Take Control of Your Car Insurance

You now have the tools and the confidence to stop the cycle of overpaying. By focusing on your unique local situation, understanding your true coverage needs, aggressively seeking out discounts, and knowing when and how to switch, you’re not just comparing policies – you’re reclaiming your financial power. Don’t let insurers dictate your budget.

Your Immediate Call to Action:

- Gather your current policy information and driver details.

- Contact at least three different sources: an online comparison tool, a local independent agent, and one major direct insurer.

- Specifically ask about every discount mentioned here.

- Compare quotes based on identical coverage, not just the lowest premium.

Start today. Your savings are waiting.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.