In today’s dynamic financial landscape, the ability to make your money work harder for you is paramount. A credit card with points offers a compelling avenue to do just that. More than just a tool for convenient payments, a well-chosen credit card with points transforms everyday spending into valuable rewards, opening doors to discounted travel, merchandise, or even cash back. This comprehensive guide will illuminate the path to earning smarter and traveling more, ensuring you make informed decisions about this powerful financial instrument.

Understanding Credit Card Points

A credit card with points is essentially a rewards credit card that gives you points for every dollar you spend. These points then accumulate and can be redeemed for various benefits. Unlike simple cashback cards that offer a percentage back directly, points often provide more flexibility and potentially higher value, especially for travel.

How Points and Rewards Work

- Earning: Most cards offer 1 point per dollar spent on general purchases. Some categories, like dining, groceries, or travel, might earn accelerated rates (e.g., 2x, 3x, or even 5x points).

- Redeeming: Points can be redeemed for flights, hotel stays, gift cards, merchandise, or statement credits. The value of a point varies by card issuer and redemption method. For instance, a point might be worth 1 cent as cashback but 1.5 cents when used for travel.

- Bonuses: Many cards offer substantial sign-up bonuses for new cardholders who meet a specified spending threshold within the first few months.

Choosing the Right Points Credit Card

Selecting the ideal points card requires careful consideration of your spending habits, financial goals, and lifestyle. There isn’t a one-size-fits-all solution, so understanding the nuances is key.

Key Factors to Evaluate

- Annual Fee: Some premium cards come with annual fees, which can be offset by superior rewards, benefits, and sign-up bonuses. Others are fee-free.

- Rewards Structure: Look at categories where you spend the most. Does the card offer bonus points on those purchases?

- Redemption Options: Do the available redemption options align with your goals (e.g., specific airlines, hotel chains, or flexible travel portals)?

- Welcome Bonus: A significant factor for initial value. Compare spending requirements against your typical budget to ensure it’s achievable without overspending.

- APR & Fees: While points are great, paying high interest negates their value. Always aim to pay your balance in full. Understand foreign transaction fees if you travel internationally.

According to the Consumer Financial Protection Bureau (CFPB), it’s crucial to review credit card agreements thoroughly to understand all terms and conditions, including fees and interest rates.

Maximizing Your Points and Rewards

Once you have a points credit card, strategic usage can significantly amplify your earnings. Smart habits go beyond just swiping your card.

Strategies for Enhanced Earning

- Category Bonuses: Pay attention to rotating bonus categories (e.g., 5x points on gas in Q1, groceries in Q2) and use the appropriate card for those purchases.

- Sign-up Bonuses: These are often the quickest way to earn a large chunk of points. Plan your large purchases around meeting the spending requirement.

- Referral Bonuses: If your card offers a referral program, encourage friends or family to apply, earning you extra points if they are approved.

- Travel Partners: Many travel points cards allow you to transfer points to airline or hotel loyalty programs, often at a favorable rate, unlocking higher value redemptions.

- Authorized Users: Adding an authorized user can boost spending and, consequently, points earned, assuming they use the card responsibly.

The Critical Importance of Responsible Use: Avoiding Debt

While earning points is exciting, the primary rule of any credit card is to use it responsibly. Carrying a balance and incurring interest charges can quickly erode the value of any rewards you earn. The average credit card with points often has a relatively high Annual Percentage Rate (APR), making it essential to pay off your balance in full each month.

Understanding Credit Card Interest

Interest is the cost of borrowing money. If you don’t pay your full statement balance by the due date, interest will be charged on the unpaid portion. This interest can compound daily, making even small balances grow over time. Always consider the potential interest charges when evaluating the benefits of a rewards card. For example, if you carry a balance of $1,000 at 20% APR, you could pay hundreds of dollars in interest over a year, far outweighing any points earned.

The Impact of Payment Habits

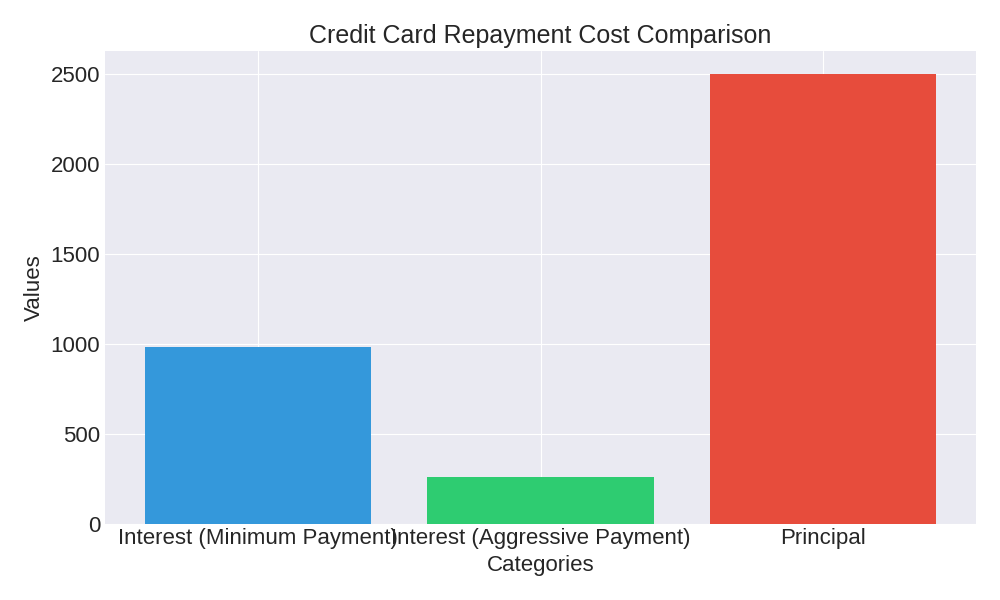

If you have a balance of $2,500 on a credit card at an APR of 19.99%, your payment strategy significantly impacts the total cost. Let’s look at how different payment approaches can affect your finances:

| Payment Strategy | Monthly Payment (Example) | Total Interest Paid (Approx.) |

|---|---|---|

| Paying Minimum Only (e.g., 2% or $30) | ~$50 | ~$980 (over ~5 years) |

| Paying Aggressively | ~$150 | ~$260 (over ~19 months) |

As this table illustrates, simply paying the minimum amount on your credit card can lead to significantly higher interest payments and a much longer repayment period. Conversely, making larger payments can save you hundreds of dollars and free you from debt much faster. This underscores the importance of treating your credit card with points as a payment tool, not a long-term borrowing mechanism.

For more detailed insights into managing credit and debt, resources like Investopedia’s guides on credit card debt management can be invaluable.

FAQ: Your Questions About Points Credit Cards Answered

Q: Are points credit cards worth it?

A: Yes, if used responsibly. For those who pay their balance in full each month, points cards offer significant value in terms of travel, cashback, or other rewards without incurring interest charges. The key is to match the card to your spending habits and redemption goals.

Q: How do I redeem my points?

A: Redemption methods vary by issuer. Typically, you log into your online account or call customer service. You can then choose from available options like booking travel through a portal, transferring to partner loyalty programs, getting statement credits, or selecting gift cards and merchandise.

Q: Do points expire?

A: It depends on the card issuer and specific program. Many programs state that points do not expire as long as your account is open and in good standing. However, some might have expiration policies if there’s inactivity or if you close the account. Always check your card’s terms and conditions.

Q: Can I transfer points between different credit cards?

A: Generally, points can be transferred between different cards within the same issuer’s loyalty program (e.g., from one Chase card to another Chase card). Transferring points between different issuers (e.g., Chase to American Express) is usually not possible, though some programs allow transfers to shared external travel partners.

Q: What is the best credit score for a points credit card?

A: Most premium points credit cards require a good to excellent credit score, typically 670 and above. Cards with lucrative rewards and benefits often look for scores in the 700s or higher. Building a strong credit history is crucial for approval.

Building and maintaining good credit is essential, as highlighted by financial experts on NerdWallet’s credit score improvement tips.

Conclusion: Empowering Your Spending

A credit card with points, when managed wisely, is far more than just a payment method; it’s a powerful financial tool that can enrich your life by turning everyday expenditures into exciting rewards. From funding your next vacation to providing valuable cashback, the benefits are substantial. However, remember that the true value lies in responsible use – always prioritize paying your balance in full to avoid interest and maximize your rewards.

Ready to Elevate Your Everyday Spending?

Explore reputable financial institutions and compare top-tier points credit cards today. Evaluate your spending habits, assess potential annual fees against expected rewards, and choose the card that best aligns with your financial aspirations. Start earning smarter and traveling more!

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.