Navigating college financing can feel overwhelming, but understanding your options is crucial. Among the most beneficial pathways are federal education loans. These aren’t just any loans; they are specially designed by the U.S. government to make higher education more accessible and affordable. This comprehensive guide will demystify the process, highlight key benefits, and provide actionable steps to secure and manage your future with an education loan federal program.

Simply put, federal education loans offer distinct advantages over private alternatives. They come with benefits like lower fixed interest rates, various income-driven repayment plans, and potential loan forgiveness programs. These features create a crucial safety net, ensuring that pursuing your education doesn’t lead to insurmountable debt. Understanding these benefits is your first step towards making informed financial decisions for college.

Understanding Federal Education Loans: Why They Matter

Federal education loans are financial aid provided by the U.S. Department of Education. Unlike private loans, which come from banks or credit unions, federal loans offer more favorable terms and protections. These government-backed options are designed to support students and families, prioritizing access to education over profit.

Why does this matter in real life? Imagine you’ve just graduated and are struggling to find a high-paying job. With federal loans, you can adjust your monthly payments based on your income, or even pause them temporarily if you’re facing financial hardship. This flexibility is a significant advantage, as many private lenders offer no such relief, potentially leading to default and damaged credit.

Key Benefits of Federal Loans

- Fixed Interest Rates: Your interest rate won’t change over the life of the loan, providing predictability in your payments.

- Income-Driven Repayment (IDR) Plans: Your monthly payment can be capped at an affordable percentage of your discretionary income. This prevents payments from overwhelming your budget, even if your income is modest.

- Deferment and Forbearance: These options allow you to temporarily pause or reduce your payments if you’re facing economic hardship or returning to school. This acts as a financial safety net.

- Loan Forgiveness Programs: Certain federal programs, like Public Service Loan Forgiveness (PSLF), can erase your remaining loan balance after a period of qualifying payments and employment.

- No Credit Check (for most undergraduate loans): Unlike private loans, undergraduate federal loans typically don’t require a credit check, making them accessible to a broader range of students.

Types of Federal Education Loans: Finding Your Fit

The U.S. government offers several types of federal loans, each with unique features and eligibility requirements. Knowing the differences is key to choosing the best option for your circumstances. Selecting the right loan can significantly impact how much you pay back over time.

Direct Subsidized Loans

These loans are available to undergraduate students who demonstrate financial need. The U.S. Department of Education pays the interest on the loan while you are enrolled at least half-time, during the grace period, and during periods of deferment. This means you accrue less debt.

Why this matters: Consider Sarah, an undergraduate student from a lower-income family. She qualifies for a Direct Subsidized Loan. If her loan is $10,000 at a 5% interest rate, the government pays the interest while she’s in school for four years. This saves her roughly $2,000 in interest she would have accumulated otherwise, reducing her total repayment burden.

Direct Unsubsidized Loans

These loans are available to both undergraduate and graduate students, regardless of financial need. You are responsible for paying all the interest on the loan. Interest begins to accrue immediately after the loan is disbursed, even while you are in school.

Why this matters: David, a graduate student, doesn’t qualify for subsidized loans but still needs aid. He takes out a Direct Unsubsidized Loan. He has the option to pay the interest while in school, or it will be capitalized (added to his principal balance) after graduation, increasing his total loan amount. Understanding this helps you decide whether to pay interest during school to save money long-term.

Direct PLUS Loans

These loans are available to graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS). Eligibility for PLUS loans is based on a credit check, and borrowers cannot have an adverse credit history. Parents are generally responsible for repayment, not the student.

Why this matters: A parent, Maria, wants to help her child attend a specific university. She considers a Parent PLUS Loan. While it requires a credit check, it offers the same federal protections as other Direct Loans, unlike a private loan. This includes income-driven repayment options (though more limited for Parent PLUS) and deferment, which provides more security than many private options.

The Application Process: Your Step-by-Step Guide

Applying for federal education loans is a straightforward process centered around one crucial form: the Free Application for Federal Student Aid (FAFSA). Completing this form accurately and on time is your gateway to accessing financial aid.

- Complete the FAFSA: This is the first and most important step. The FAFSA collects information about your financial situation to determine your eligibility for federal student aid. You can complete it online at StudentAid.gov.

- Review Your Student Aid Report (SAR): After submitting the FAFSA, you’ll receive a SAR, which summarizes your submitted data. Review it carefully for any errors, as mistakes can affect your aid eligibility.

- Receive Your Financial Aid Offer: Your chosen college will use your FAFSA data to create a financial aid offer. This letter outlines the grants, scholarships, work-study, and federal loans you’re eligible for. Compare offers from different schools if you applied to multiple.

- Accept or Decline Aid: Carefully consider your financial aid offer. You don’t have to accept all the aid offered. For loans, only borrow what you truly need.

- Complete Entrance Counseling: If you accept federal loans, you’ll need to complete entrance counseling. This online session explains your rights and responsibilities as a borrower. This ensures you understand your commitment.

- Sign the Master Promissory Note (MPN): The Master Promissory Note (MPN) is a legal document in which you promise to repay your loan(s) and any accrued interest and fees to the U.S. Department of Education. It can cover multiple loans over several years.

Imagine you’re filling out the FAFSA. It asks for your family’s income and assets. Why does this matter? Because accurate information determines your Expected Family Contribution (EFC). This EFC is used by schools to calculate your financial need, directly impacting the amount and type of federal aid, including loans, you qualify for. Missing deadlines or making errors can mean missing out on valuable aid.

Smart Repayment Strategies for Your Federal Loans

Once you finish school, understanding your repayment options for an education loan federal is crucial. Federal loans offer a variety of plans, designed to help you manage your debt effectively. Choosing the right plan can make a significant difference in your monthly budget and overall financial health.

Understanding Your Repayment Options

- Standard Repayment Plan: This is the default plan, with fixed monthly payments over 10 years. It typically results in the least interest paid over the life of the loan.

- Graduated Repayment Plan: Payments start low and gradually increase every two years, usually over 10 years. This plan is good if you expect your income to grow over time.

- Extended Repayment Plan: Offers lower monthly payments over an extended period (up to 25 years) for borrowers with larger loan balances. However, you’ll pay more interest over the long term.

- Income-Driven Repayment (IDR) Plans: These plans cap your monthly payments based on your income and family size, usually between 10-20% of your discretionary income. Any remaining balance after 20 or 25 years of payments may be forgiven. Popular IDR plans include REPAYE, PAYE, IBR, and ICR. This matters because it provides an affordable safety net, preventing default even if your income is low.

Consider a new graduate, Alex, who has $30,000 in federal loans and starts a job earning $35,000 annually. Under the standard 10-year plan, his monthly payments might be around $300-$350, which could be tight. By opting for an IDR plan, his payment could drop to, say, $150-$200, making it much more manageable. This flexibility is a core benefit, allowing borrowers to navigate fluctuating income while staying current on their obligations.

Public Service Loan Forgiveness (PSLF)

For individuals working in eligible public service jobs (government, non-profit organizations), the Public Service Loan Forgiveness (PSLF) program offers the ultimate benefit: forgiveness of the remaining balance on Direct Loans after 120 qualifying monthly payments while working full-time for a qualifying employer. This can be a life-changing benefit for those committed to public service careers.

You can learn more about these options and manage your loans through official resources like The Consumer Financial Protection Bureau, which provides guidance on student loan repayment.

How to Estimate Your Loan Costs

Understanding the total cost of your federal loan involves more than just the principal amount; it also includes the interest that accrues over time. Calculating this can help you prepare for repayment and evaluate different strategies. While exact calculations can be complex, you can estimate your costs in plain language.

Essentially, your interest is typically calculated daily based on your outstanding loan balance. Each month, a portion of your payment goes towards interest, and the rest reduces your principal. The faster you pay down the principal, the less interest you’ll pay overall. Many online calculators can help you visualize this.

Here’s a simplified way to think about it:

- Principal Amount: This is the money you borrowed.

- Interest Rate: This is the cost of borrowing, expressed as a percentage. It’s applied to your principal.

- Repayment Term: This is how long you have to pay back the loan (e.g., 10 years).

- Monthly Payment: Each payment covers some interest and some principal. Earlier payments tend to have a higher proportion of interest.

- Total Interest Paid: This is the sum of all interest payments over the life of the loan.

- Total Amount Paid: This is your principal amount plus the total interest paid.

The longer your repayment term or the higher your interest rate, the more total interest you will pay, even if your monthly payments seem lower. Shortening your repayment term or making extra payments can significantly reduce your total cost. Why does this matter? Because even a seemingly small difference in interest or repayment term can add thousands to your total repayment. Being aware helps you make smarter repayment choices.

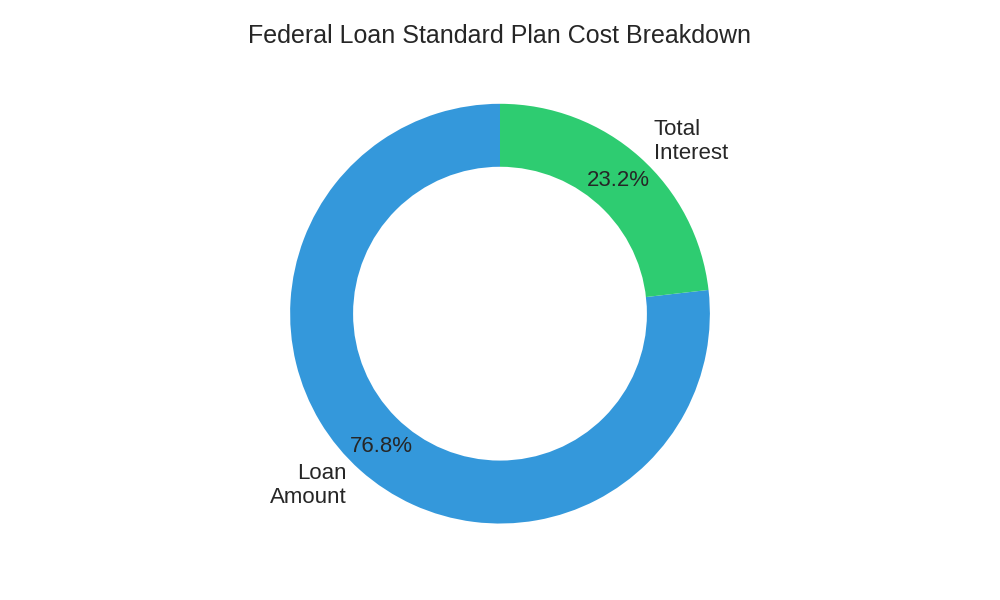

Estimate Your Federal Loan Payments

To illustrate the impact of different repayment choices, consider a federal loan scenario:

| Loan Feature | Scenario 1: Standard Plan | Scenario 2: Extended Plan |

|---|---|---|

| Loan Amount | $20,000 | $20,000 |

| Interest Rate (Fixed) | 5.5% | 5.5% |

| Repayment Term | 10 Years | 20 Years |

| Estimated Monthly Payment | ~$217 | ~$136 |

| Total Interest Paid (approx.) | ~$6,040 | ~$12,640 |

| Total Amount Paid (approx.) | ~$26,040 | ~$32,640 |

As you can see, while the extended plan offers lower monthly payments, it significantly increases the total interest paid over the life of the loan. This table demonstrates why selecting a repayment plan that balances affordability with minimizing overall cost is so important.

Frequently Asked Questions (FAQ)

Are federal education loans always better than private loans?

For most students, yes. Federal loans typically offer more generous repayment options, fixed interest rates, and access to forgiveness programs that private loans do not. Private loans often require a credit check, may have variable interest rates, and fewer borrower protections. Always exhaust your federal loan options before considering private loans.

What is the FAFSA deadline?

The FAFSA opens on October 1st each year. While there are federal deadlines (usually June 30th), many states and individual colleges have earlier priority deadlines. It’s crucial to submit your FAFSA as early as possible to maximize your eligibility for all types of aid, including grants and scholarships that are often first-come, first-served.

Can I get federal loans if my parents make a lot of money?

Yes, often you can. While financial need is a factor for some federal aid (like Direct Subsidized Loans), others, like Direct Unsubsidized Loans, are available regardless of your or your parents’ income. Grad PLUS and Parent PLUS loans are also available to higher-income families, subject to a credit check. Filling out the FAFSA is the only way to know what you qualify for.

What happens if I can’t afford my federal loan payments?

If you face financial hardship, federal loans offer several solutions. You can apply for deferment or forbearance to temporarily pause payments, or enroll in an Income-Driven Repayment (IDR) plan to lower your monthly amount based on your income. Contact your loan servicer immediately to explore these options before missing a payment.

Conclusion

Federal education loans are a cornerstone of financial aid for higher education, offering unparalleled benefits and flexibility compared to private alternatives. By understanding the types of loans available, diligently completing the FAFSA, and strategically managing your repayment, you can navigate your academic journey without undue financial stress. These loans are designed to support your success, providing a secure pathway to achieving your educational goals.

Take Action Today!

Don’t let the cost of college deter you. Take the first step by completing your FAFSA and exploring the federal loan options available to you. Your future is an investment worth making, and federal student aid is here to help you achieve it. Visit StudentAid.gov to begin your application and learn more.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.