The dream of homeownership often feels out of reach for many, primarily due to the significant upfront costs involved, particularly the down payment. However, there’s a powerful tool designed to make this dream more accessible: the FHA loan.

This guide will walk you through everything you need to know about purchasing a home with less cash upfront, helping you understand the path to securing a favorable mortgage. An FHA loan, backed by the government, offers a unique opportunity for aspiring homeowners to enter the market with more flexible requirements than conventional loans. It truly makes a difference for those looking to buy a home without a huge initial investment.

What is an FHA Loan?

An FHA Loan, officially known as an FHA loan, is a mortgage insured by the Federal Housing Administration (FHA), which is part of the U.S. Department of Housing and Urban Development (HUD). It’s crucial to understand that the FHA doesn’t actually lend money directly. Instead, it insures the loan against borrower default, reducing the risk for lenders. This government backing encourages approved lenders to offer more favorable terms, especially to borrowers who might not qualify for traditional financing.

The primary purpose of an FHA loan is to make homeownership accessible to a broader range of individuals. This includes first-time homebuyers, those with lower credit scores, or individuals with limited funds for a down payment. By insuring these loans, the FHA helps millions achieve their dream of owning a home across the United States. It’s a cornerstone program designed to foster economic stability and community growth.

Key Benefits of an FHA Loan

FHA loans come with several significant advantages that set them apart from conventional mortgages. These benefits are specifically tailored to help make homeownership more attainable, especially for those facing financial hurdles.

- Low Down Payment Requirements: One of the most attractive features of an FHA loan is its low down payment. Borrowers can qualify with as little as a 3.5% down payment of the home’s purchase price, provided they meet certain credit score criteria.

- Flexible Credit Score Requirements: FHA loans are known for having more lenient credit score guidelines compared to conventional loans. While a higher score is always better, it’s possible to qualify with a credit score in the mid-500s, though a 580+ score typically secures the lowest down payment.

- Competitive Interest Rates: Due to the government insurance, lenders often view FHA loans as less risky. This can translate into more competitive interest rates for borrowers, potentially saving thousands over the life of the loan.

- Assumable Mortgages: In many cases, FHA loans are assumable. This means a new buyer can take over the existing mortgage, potentially benefiting from the original interest rate and terms, which can be a significant advantage in certain market conditions.

- Acceptance of Gift Funds: FHA loans allow down payment funds to be a gift from a family member, employer, or charitable organization, which further eases the financial burden on the borrower.

Eligibility Requirements for an FHA Loan

While FHA loans are designed for accessibility, there are still specific criteria borrowers must meet to qualify. Understanding these requirements is the first step towards securing your mortgage.

- Credit Score: Generally, a minimum credit score of 580 is required for the 3.5% down payment option. Borrowers with scores between 500-579 may still qualify but will typically need a 10% down payment.

- Down Payment: As mentioned, a minimum of 3.5% of the purchase price is required. These funds must be verifiable and can come from savings, a gift, or specific down payment assistance programs.

- Debt-to-Income (DTI) Ratio: Lenders will examine your DTI ratio, which compares your total monthly debt payments to your gross monthly income. While the FHA has flexible guidelines, most lenders prefer a front-end ratio (housing expenses) no higher than 31% and a back-end ratio (total debts) no higher than 43%. However, exceptions can be made for strong borrowers.

- Property Requirements: The home being purchased must meet FHA appraisal standards to ensure it is safe, sound, and secure. This is to protect both the borrower and the FHA. The property must also be used as the borrower’s primary residence.

- Stable Employment and Income: Borrowers must demonstrate a stable employment history, typically for the past two years, and a reliable income source to prove their ability to repay the loan.

Understanding FHA Loan Costs

While FHA loans offer many advantages, it’s important to be aware of the associated costs beyond the principal and interest. These include mortgage insurance premiums and typical closing costs.

- Mortgage Insurance Premium (MIP): All FHA loans require MIP, which serves as the FHA’s insurance policy against default. This comes in two forms:

- Upfront Mortgage Insurance Premium (UFMIP): A one-time fee equal to 1.75% of the loan amount, typically financed into the loan, meaning you don’t pay it out of pocket at closing.

- Annual Mortgage Insurance Premium (Annual MIP): An ongoing premium paid monthly, with the rate varying based on loan amount, loan-to-value (LTV) ratio, and loan term. This fee is often for the life of the loan unless certain conditions are met, such as having a low LTV ratio at the start of the loan for 11 years, or refinancing into a conventional loan.

- Closing Costs: Like all mortgages, FHA loans come with closing costs, which are fees associated with processing the loan and transferring property ownership. These can include appraisal fees, title insurance, loan origination fees, and more. FHA rules allow sellers to contribute up to 6% of the sale price towards a buyer’s closing costs.

Step-by-Step Guide to Getting an FHA Loan

Navigating the mortgage process can seem daunting, but breaking it down into manageable steps makes it much clearer. Here’s a practical guide to securing your FHA loan.

- Check Your Eligibility: Start by assessing your financial situation against the FHA’s credit score, down payment, and DTI requirements. A basic self-assessment will help you understand where you stand.

- Get Pre-approved: Contact an FHA-approved lender to get pre-approved for a loan. This involves providing financial documents for review and will give you a clear idea of how much you can afford, strengthening your offer when you find a home.

- Find an FHA-Approved Property: Work with a real estate agent experienced in FHA transactions to find a home that meets FHA property standards. Remember, the home must pass an FHA appraisal.

- Apply for the Loan: Once you’ve found a home and your offer is accepted, complete the full loan application with your chosen lender. This is where you’ll submit all necessary financial documentation for a thorough review.

- Underwriting and Approval: The lender’s underwriting team will meticulously review your application, credit, income, and the property appraisal. They ensure everything aligns with FHA and lender guidelines before granting final approval.

- Closing: After final approval, you’ll attend the closing appointment. Here, you’ll sign all necessary paperwork, pay any remaining closing costs, and officially become the homeowner. Congratulations!

How FHA Loan Payments Work: A Simple Explanation

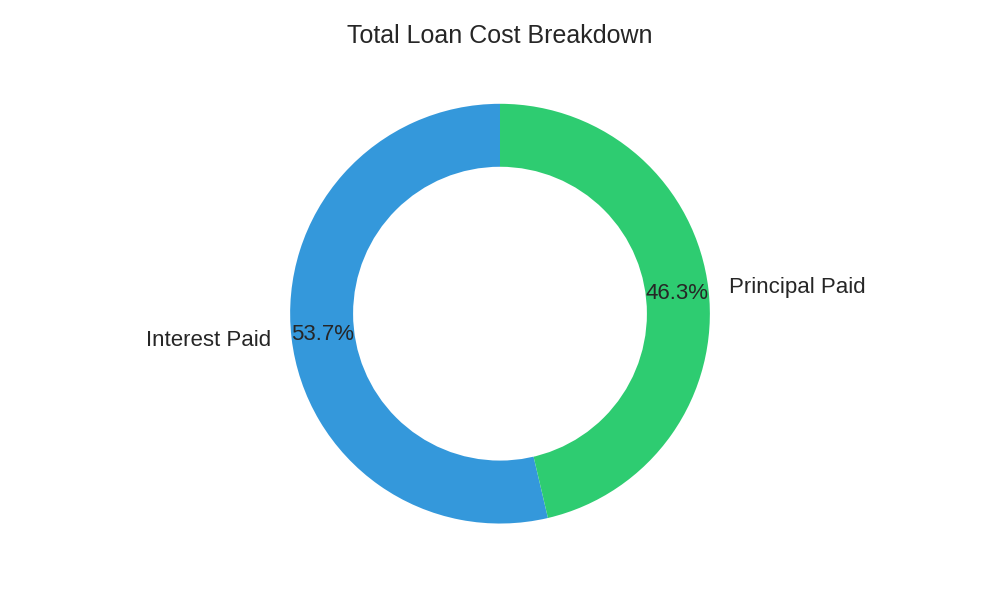

Understanding your monthly mortgage payment is key to budgeting and financial planning. An FHA loan payment primarily consists of two components: principal and interest. The principal is the amount you borrowed, and the interest is the cost of borrowing that money. Over the life of a typical 30-year mortgage, your early payments will primarily go towards interest, with a smaller portion reducing your principal balance. As time progresses, more of your payment will be applied to the principal. This repayment structure is known as amortization.

If you borrow a principal amount of $150,000 at a fixed interest rate of 6.0% over a 30-year term, you would pay approximately $899.33 per month (excluding taxes and insurance). Over the entire 30 years, your total payments would amount to roughly $323,758.80. This illustrates how interest significantly impacts the total cost of your loan. The table below shows a simplified view of how your loan balance might decrease over time.

| Year | Remaining Balance | Monthly Payment |

|---|---|---|

| Start | $150,000.00 | $899.33 |

| 5 | $137,300.00 | $899.33 |

| 10 | $120,400.00 | $899.33 |

| 15 | $98,900.00 | $899.33 |

| 20 | $72,100.00 | $899.33 |

| 25 | $39,200.00 | $899.33 |

| 30 | $0.00 | $899.33 |

Monthly Payment Calculator

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.