Your business is growing, and suddenly, your current bank account feels like a straitjacket. You’re hitting transaction limits, paying unexpected fees, or your banking just isn’t keeping pace with your expanding operations. This isn’t just an inconvenience; it’s a drag on your profitability and a major source of stress. You need more than just a place to hold money; you need a strategic partner that understands and supports your ambition.

Finding the best business banking accounts isn’t about picking the cheapest option; it’s about aligning your financial infrastructure with your growth trajectory. Many entrepreneurs make the mistake of sticking with their initial personal bank or choosing a basic business account that quickly becomes outdated. This guide is designed to help you cut through the noise and find the best business banking accounts tailored for your success, not just today, but for the future you’re building.

Decoding Your Business Banking Needs for Optimal Growth

Before you even look at a single bank, you need a clear picture of your business’s financial habits. This isn’t just about current needs, but also anticipating future demands. Imagine you are a burgeoning e-commerce store. Initially, you might have low transaction volumes, but within a year, you could be processing hundreds of payments daily, requiring robust digital integration and higher limits.

Why does this matter in real life? Choosing the wrong account now can lead to expensive fees and operational headaches later. You might incur significant charges for exceeding transaction limits or for needing features (like international wire transfers) that your basic account doesn’t offer at a reasonable price.

- Transaction Volume: How many deposits, withdrawals, and payments do you make monthly? Some accounts offer “free” transactions up to a certain point, then charge per item.

- Cash Handling: Do you deal with a lot of physical cash deposits? Some online-only banks have limited options, while traditional banks might charge significant cash handling fees.

- Digital Integration: Do you use accounting software (like QuickBooks) or payment processors (like Stripe)? Seamless integration can save hours of manual reconciliation.

- Employee Access: Will multiple team members need access to banking functions? Look for accounts with robust user management and permission controls.

- International Needs: Do you make or receive international payments? Consider currency exchange rates and wire transfer fees.

Common Myths to Avoid When Choosing Accounts

Many business owners fall for common misconceptions. One prevalent myth is that “free” business checking means truly free. In reality, these accounts often come with hidden catches like high minimum balance requirements or per-transaction fees once you exceed a low threshold. Another myth is that you need to stick with a big national bank; often, local credit unions or online-only banks offer more tailored and cost-effective solutions for specific business types.

Insider Tip: Always read the fee schedule meticulously. Don’t just look for “no monthly fee.” Dig into transaction fees, ATM fees, cash deposit limits, and potential charges for low balances or account inactivity. These are the details that separate truly cost-effective options from those that just look good on the surface.

Key Features to Prioritize in the Best Business Banking Accounts

Once you understand your needs, you can evaluate specific features. Think of your banking account as a toolbox for your financial operations. You want the right tools for the job, and perhaps a few extra for future growth.

- Fee Structure: Beyond monthly fees, scrutinize transaction limits, ATM charges, and wire transfer costs. Some banks waive fees with a minimum balance or specific activity.

- Online & Mobile Banking: A robust, intuitive platform is non-negotiable. Look for features like mobile check deposit, bill pay, and multi-user access with customizable permissions.

- Integration Capabilities: Does the bank easily link with your accounting software, payroll providers, and payment processors? This can streamline your bookkeeping immensely.

- Cash Deposit Options: If you handle cash, consider branch access, ATM networks, or partnerships with third-party cash deposit services.

- Customer Service: Accessible and knowledgeable support is crucial, especially when issues arise. Test their responsiveness during your research phase.

The Hidden Costs: What Generic Articles Miss

Most articles just list features. As your financial strategist, I’m here to tell you about the often-overlooked costs. For example, some banks offer great introductory rates or low fees, but then sharply increase them after a year. Or, they might have a low monthly fee, but astronomical charges for every transaction over a low limit. This impacts your real-life profitability significantly.

Scenario: Imagine your small consulting firm starts to land bigger clients. Your monthly transactions jump from 20 to 100. If your current account charges $0.50 per transaction over 50, that’s an extra $25 a month you weren’t expecting. Over a year, that’s $300 that could have been reinvested in marketing or software. These small, recurring fees chip away at your profit margin.

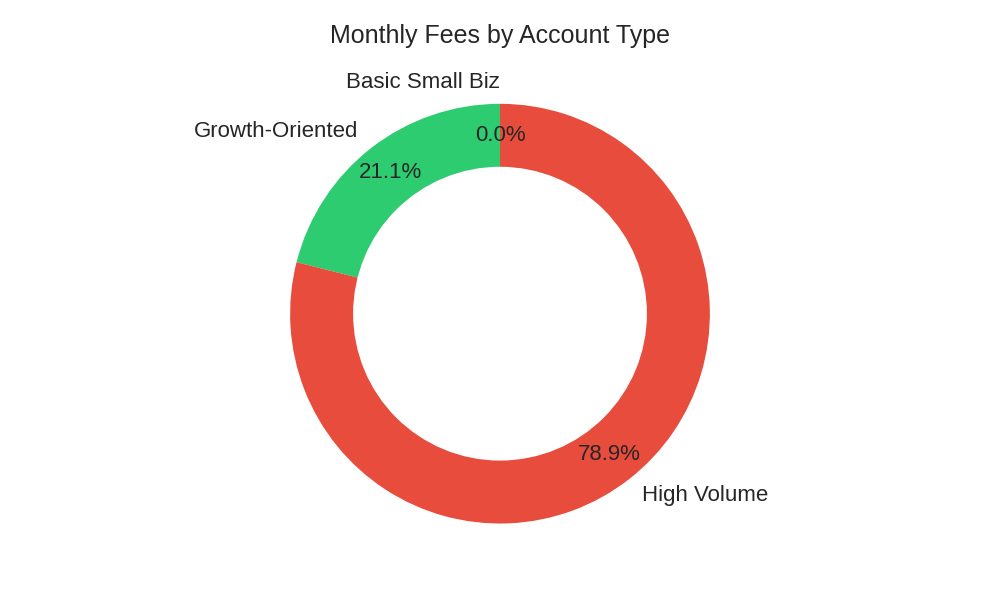

Here’s a comparison of how different account types might impact your business over time:

| Account Type | Monthly Fee Range | Typical Transaction Limit |

|---|---|---|

| Basic Small Biz | $0 – $15 | 20 – 100 free |

| Growth-Oriented | $20 – $50 | 200 – 500 free |

| High Volume/Enterprise | $75+ | Unlimited or very high |

This table illustrates how crucial it is to match your account to your current and projected transaction needs to avoid unnecessary costs.

How to Calculate Your Effective Banking Costs

Understanding the true cost of a business banking account goes beyond just looking at the advertised monthly fee. You need to factor in all potential charges based on your anticipated activity.

Here’s a practical way to estimate your effective monthly banking cost:

Start with the base monthly service fee, if any. Then, identify your typical monthly transaction volume: how many checks do you write, how many debit card purchases do you make, how many times do you deposit cash, how many incoming/outgoing wires?

Next, look at the bank’s fee schedule for each of these activities. If an account offers 50 free transactions but you typically do 75, multiply the 25 excess transactions by the per-item fee. Add any fees for cash deposits, wire transfers, or out-of-network ATM withdrawals you anticipate making.

Sum all these potential charges to the base monthly fee. This gives you a more realistic picture of your overall monthly banking expense. Compare this ‘effective cost’ across several different banks to find the one that offers the best value for your specific business activity.

Business Banking Fee Savings Calculator

Your Current Bank:

Proposed New Bank:

Your Monthly Business Activity:

For instance, if a bank charges a $10 monthly fee, plus $0.50 for every transaction over 100. If you process 150 transactions, your additional cost is $25 (50 transactions * $0.50). Your total effective cost would be $35 ($10 base + $25 excess transaction fees). This simple calculation reveals the true financial impact.

Choosing Between Traditional, Online, and Credit Union Options

The landscape of business banking is diverse. You’re not limited to the branch down the street. Each type of institution offers distinct advantages and disadvantages.

- Traditional Banks (e.g., Chase, Bank of America): Offer extensive branch networks, a wide range of services, and often dedicated business relationship managers. They are ideal if you require frequent in-person services, cash deposits, or complex lending needs. However, they can have higher fees and more rigid policies. Learn more about the role of banking institutions at the Federal Reserve website.

- Online Banks (e.g., Bluevine, Mercury): Typically have lower fees, higher interest rates on balances, and cutting-edge digital platforms. They are excellent for businesses that operate primarily digitally and have minimal cash needs. Their main drawback is limited or no physical branch access, which can be an issue for cash-heavy businesses or those preferring face-to-face interaction.

- Credit Unions: Member-owned, credit unions often offer more personalized service, lower fees, and better interest rates than traditional banks. They are fantastic for community-focused businesses. Their network and service offerings might be less extensive than large banks, but their customer-centric approach can be a huge benefit for small and growing businesses. You can find resources on managing small business finances on the U.S. Small Business Administration (SBA) site.

Insider Tip: Don’t Forget About Deposit Insurance

Regardless of where you bank, ensure your deposits are protected. Most reputable banks and credit unions offer deposit insurance. For banks, this is typically through the FDIC (Federal Deposit Insurance Corporation), and for credit unions, it’s the NCUA (National Credit Union Administration). This protects your money up to $250,000 per depositor, per insured bank, for each account ownership category. Always verify this critical protection. You can verify a bank’s FDIC coverage at the FDIC website.

Conclusion: Your Strategic Banking Partner for Growth

Choosing the best business banking accounts isn’t a one-time decision; it’s an ongoing strategy. As your business evolves, your banking needs will too. Don’t let inertia keep you tethered to an account that no longer serves you. Proactively reviewing your banking relationship ensures your financial infrastructure is always optimized for efficiency and growth.

Take control of your business finances today. Evaluate your current account against the insights provided, explore alternatives, and choose a banking partner that empowers your ambitions, rather than hinders them. Your business deserves a financial foundation that supports every step of its journey.

Call to Action: Review your last three months of bank statements today. Identify all fees charged and compare them with the features you actually use. Then, research at least three alternative business banking accounts using the criteria outlined above. Make a switch if it means better alignment with your growth goals!

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.