You’re probably feeling stuck, right? You know you need solid protection for your vehicle – that feeling of security if something goes wrong. But the thought of adding another hefty monthly payment to your budget makes your stomach clench. You’re caught in the dilemma of finding low cost full coverage car insurance that actually protects you, not just drains your wallet.

Forget the endless online searches filled with generic advice. You’re here because you want real answers, strategies, and insider tips to navigate the insurance labyrinth and find truly low cost full coverage car insurance without sacrificing peace of mind. Let’s cut straight to it: securing affordable, comprehensive protection for your car is absolutely possible, but it requires a smart, strategic approach. The quest for low cost full coverage car insurance can feel like chasing a ghost, but I’m here to show you exactly how to catch it.

The “Full Coverage” Myth: What You Really Need to Know

First, let’s bust a common myth. There’s no single insurance product officially called “full coverage.” When people, or even insurers, say it, they’re generally referring to a combination of policies that provide comprehensive protection beyond just the legal minimum liability. This typically includes liability insurance, collision insurance, and comprehensive insurance.

Why does this matter in real life? Because knowing what these components cover empowers you to tailor your policy, rather than just accepting a “full coverage” label that might have gaps.

Liability Insurance: This is your foundation. It covers damages and injuries you might cause to other people and their property*. If you cause an accident, your liability coverage pays for the other driver’s car repairs and medical bills, up to your policy limits.

Collision Insurance: This is crucial for protecting your own vehicle* in an accident, regardless of who is at fault. If you hit another car, a pole, or even just back into a tree, collision coverage helps pay for your car’s repairs (minus your deductible).

Comprehensive Insurance: This protects your car from just about everything else* that isn’t a collision. Think theft, vandalism, fire, natural disasters, or hitting an animal. If a rogue tree branch falls on your car, this is your savior.

Common Myth to Avoid: Believing “full coverage” is a magic bullet that covers everything imaginable. It doesn’t typically cover mechanical breakdowns, wear and tear, or items stolen from inside your car (that’s usually covered by homeowners/renters insurance). Always read the policy details.

Unmasking Hidden Costs and Finding Real Savings

Your insurance premium isn’t some arbitrary number; it’s a calculation based on dozens of factors, many of which you can influence. Understanding these drivers is your first step to unlocking significant savings.

Your Driving Profile: It’s More Than Just Accidents

Insurance companies assess your risk profile extensively. It’s not just about your driving record, though that’s certainly a major factor.

• Your Credit Score: This might surprise you, but in most states, your credit-based insurance score plays a substantial role. Insurers view those with higher credit scores as more responsible and less likely to file claims. Improving your credit can genuinely lower your premiums. For tips on managing your credit, check out resources like MyFico.com.

• Annual Mileage: If you work from home or have a short commute, you’re driving less, which means less time on the road and lower risk. Some insurers offer discounts for low mileage drivers.

• Occupation: Believe it or not, some professions are statistically associated with lower claims rates. If your job involves less driving or is considered lower risk, you might benefit.

• Driving Record: This is obvious, but worth reiterating: a clean driving record with no accidents or moving violations is your most powerful tool for securing the best rates. Avoid tickets like the plague.

Your Vehicle’s Impact on Premiums

The car you drive is a huge piece of the puzzle. It’s not just the make and model, but its safety features and theft risk.

• Safety Features: Modern cars with advanced safety features like automatic emergency braking, lane departure warning, and adaptive cruise control can qualify for discounts. These features reduce the likelihood of accidents or the severity of damage. You can research vehicle safety ratings on sites like IIHS.org.

• Anti-Theft Devices: A car with a factory-installed alarm system, GPS tracking, or an immobilizer is less likely to be stolen. This translates to lower comprehensive coverage costs.

• Vehicle Age and Value: Older, less valuable cars often cost less to insure because their replacement parts and overall value are lower. If you have an older car, carefully consider if the cost of collision and comprehensive coverage still makes financial sense compared to the car’s market value. This is where you might decide to drop “full coverage.”

Strategic Shopping: How to Get the Best Deals

You wouldn’t buy a house or a major appliance without comparing prices, so why treat your insurance differently? This is where your power truly lies.

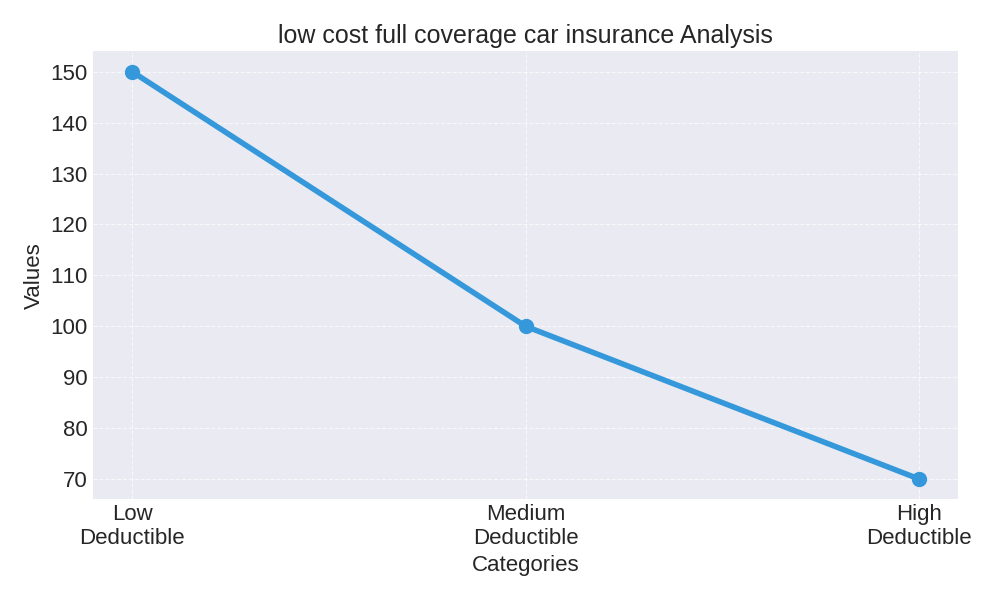

Demystifying Deductibles: A Pro/Con Analysis

Your deductible is the amount you pay out-of-pocket before your insurance kicks in for a claim. This is a critical lever for adjusting your premium.

Imagine you’re reviewing two policies. Both offer the same coverage, but one has a $500 deductible, and the other has a $1,000 deductible. The policy with the $1,000 deductible will have a noticeably lower monthly premium. This is because you’re taking on more of the financial risk upfront.

Here’s a practical look at how different deductibles can impact your costs:

| Deductible Level | Monthly Premium Impact (Illustrative) | Out-of-Pocket Risk (Per Claim) |

|---|---|---|

| Low ($250-$500) | Higher Premium (e.g., $150-$200) | Lower (e.g., $250-$500) |

| Medium ($750-$1,000) | Moderate Premium (e.g., $100-$150) | Moderate (e.g., $750-$1,000) |

| High ($1,500-$2,500) | Lower Premium (e.g., $70-$100) | Higher (e.g., $1,500-$2,500) |

Pro/Con: A higher deductible saves you money on premiums but means you need to have more cash saved up in an emergency fund for potential repairs. A lower deductible means higher premiums but less upfront cost if you file a claim. Choose a deductible you can realistically afford to pay without financial strain.

Bundling & Discounts: More Than Just a Marketing Gimmick

Never underestimate the power of discounts. Insurance companies offer a multitude of ways to lower your premium, and it’s your job to ask for them.

• Bundling Policies: This is one of the easiest ways to save big. If you combine your auto insurance with your home, renters, or even life insurance, you can often save between 10-25% on your total premium. Imagine you pay $150/month for auto and $50/month for renters. Bundling could reduce that to $160/month total, saving you $40/month! Find more tips on bundling from financial experts at NerdWallet.com.

• Multi-Car Discount: Insuring more than one vehicle with the same provider often leads to a discount.

• Good Student Discount: If you have a student driver on your policy with good grades (typically a B average or higher), you could get a break.

• Safe Driver/Telematics Discount: Many companies now offer devices or apps that monitor your driving habits (speeding, hard braking, mileage). Drive safely, and you’ll be rewarded.

• Payment Discounts: Setting up auto-pay, paying your premium in full upfront, or opting for paperless billing can all net you small but meaningful savings.

Your “How to Calculate” Savings Power

To truly find low cost full coverage car insurance, you need to compare, compare, compare. Don’t just stick with your current provider out of loyalty. Loyalty often costs you money in the long run.

Here’s how to approach it:

1. Gather Your Information: Have your current policy details, driver’s license numbers, vehicle information (VIN, make, model, year), and any recent driving history handy.

2. Decide Your Coverage Needs: Based on what you learned about liability, collision, and comprehensive, determine the limits and deductibles that make sense for your budget and vehicle value. For example, if your car is only worth $3,000, paying $1,000 a year for full coverage with a $1,000 deductible might not be the most economical choice.

3. Get Multiple Quotes: Contact at least 3-5 different insurance providers. Use online comparison tools, or call agents directly. Don’t be afraid to pit them against each other (politely!). Ask for a detailed breakdown of what each quote includes.

4. Compare Apples to Apples: Ensure each quote provides identical coverage limits and deductibles. A lower premium means nothing if it’s for significantly less protection. Look for the “why” behind any major price differences.

5. Calculate Your Total Cost: Factor in the annual premium minus any discounts plus your chosen deductible. This gives you a clear picture of your actual financial outlay in a year, or if you had to make a claim.

Imagine you get one quote for $120/month with a $500 deductible and another for $100/month with a $1,000 deductible. Over a year, the first is $1,440 and the second is $1,200. That’s a $240 annual difference. But if you have an accident, you’d pay $500 on the first, and $1,000 on the second. You need to weigh that $240 annual saving against the extra $500 out-of-pocket risk.

Full Coverage Savings Estimator

Select potential savings strategies:

Common Pitfalls to Avoid When Seeking Low Cost Full Coverage Car Insurance

Even with the best intentions, people often make mistakes that cost them hundreds annually. Don’t be one of them.

• Going Too Cheap on Liability: You might think you’re saving money by choosing the bare minimum liability. But if you cause a serious accident, and your limits are too low, you could be personally responsible for hundreds of thousands in damages. That’s a financial catastrophe. Aim for at least $100,000/$300,000/$100,000 (per person/per accident/property damage) if your budget allows.

• Not Reviewing Your Policy Annually: Your life changes, and so should your insurance. Did you get married? Buy a house? Your kids got their licenses? Your old car is now paid off? All these events can impact your rates and qualify you for new discounts. Always review and re-quote.

Being Afraid to Switch: Many people stay with the same insurer for years out of convenience or perceived loyalty. Insurers often offer their best rates to new* customers to lure them in. Don’t be afraid to take your business elsewhere if it means substantial savings for the same (or better) coverage.

• Forgetting About Usage-Based Insurance: Telematics programs might feel intrusive, but they can offer significant discounts for safe drivers. If you’re confident in your driving habits, it’s an easy way to save.

Conclusion: Take Control of Your Car Insurance Costs

You don’t have to choose between financial stability and proper protection for your vehicle. By understanding the components of full coverage, actively managing your risk factors, and engaging in smart, strategic shopping, you are empowered to find genuinely low cost full coverage car insurance. This isn’t about cutting corners; it’s about being an informed consumer.

Call to Action: Don’t wait. Open a new tab right now and start comparing quotes from at least three different providers. Use the knowledge you’ve gained here to ask the right questions and demand the best rates. Your budget will thank you, and you’ll drive with true peace of mind.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.