You’re standing at a critical juncture, aren’t you? You know investing is essential for your future, for building true wealth, but the sheer volume of options and the fear of making the wrong choice—or worse, falling victim to a scam—is paralyzing. You’ve heard the horror stories, the missed opportunities, the confusing jargon. How do you cut through the noise to find trusted investing companies that genuinely have your best interest at heart?

Forget the bland introductions and endless definitions. This isn’t about theory; it’s about action. Your hard-earned money deserves more than a leap of faith. It needs a strategy, a checklist, and an advocate. I’m here to give you that.

Why Trust Matters More Than You Think

You’re not just handing over money; you’re entrusting your financial future. Imagine pouring years of savings into an account, only to find later that excessive, hidden fees have silently eaten away at your returns, or that the company wasn’t as reputable as it seemed. This isn’t just about losing a few dollars; it’s about losing years of potential growth and eroding your confidence in the market.

Why this matters in real life: A truly trustworthy firm acts as a fiduciary, meaning they are legally obligated to put your interests first. This isn’t a “nice-to-have”; it’s a non-negotiable requirement. Without this commitment, you’re playing a dangerous game where your advisor’s commission might take precedence over your financial well-being.

Common Myths to Avoid When Choosing Investing Companies

Don’t fall for these widespread misconceptions that can steer you wrong:

- Myth #1: “The biggest name is always the best name.” While large firms often have extensive resources, they aren’t immune to issues, and their size doesn’t automatically mean personalized service or lower fees for smaller investors. Sometimes, smaller, specialized investing companies offer more tailored attention.

- Myth #2: “Lowest fees always win.” While fees are crucial, an extremely low-fee company might skimp on customer service, educational resources, or robust technology. The goal isn’t just cheap; it’s value for money.

- Myth #3: “Guaranteed returns exist.” This is perhaps the most dangerous myth. Any company promising “guaranteed high returns” or “no risk” is a major red flag. All investments carry some level of risk. This should make you walk away immediately.

Why this matters in real life: Believing these myths can lead you to firms that are either a poor fit for your needs, or worse, outright fraudulent. Understanding what’s truly important helps you make informed choices.

Your Blueprint for Vetting Investing Companies

You need a systematic approach, not guesswork. This isn’t about finding the perfect company, but the right one for you, backed by solid verification.

-

Check Regulatory Compliance: This is your first and most critical step. Every legitimate investment firm and financial advisor must be registered with the appropriate regulatory bodies. For brokers and investment advisors in the U.S., this means the Securities and Exchange Commission (SEC) or state securities regulators, and often the Financial Industry Regulatory Authority (FINRA).

Why this matters in real life: Checking these databases allows you to see if a firm or individual is registered, if they have any disciplinary history, or if they’re operating illegally. For example, you can search the SEC’s Investment Adviser Public Disclosure (IAPD) database to verify an advisor’s credentials and history. If they’re not listed or have a problematic record, move on.

-

Understand Their Fiduciary Duty: Insist on working with a fiduciary. A fiduciary is legally and ethically bound to act in your best interest. Non-fiduciaries (like some brokers) only need to recommend suitable products, which might still earn them a higher commission.

Why this matters in real life: This distinction can save you thousands over time. A fiduciary will recommend low-cost index funds if that’s best for you, even if it means less profit for them. A non-fiduciary might push a higher-fee mutual fund that’s “suitable” but not optimal.

The Crucial Role of Regulatory Bodies

Think of the SEC and FINRA as the watchdogs of the financial world. The SEC oversees investment advisers and the broader securities markets, ensuring fair dealings. FINRA focuses on brokerage firms and their registered representatives, enforcing rules and disciplining those who violate them.

Why this matters in real life: These bodies provide transparency and a layer of protection. Without them, the market would be a free-for-all. Always use their public databases to confirm credentials and check for past misconduct. It’s your first line of defense against bad actors.

Decoding Fees and Services: What You’re Really Paying For

Fees are not just an annoyance; they are a direct attack on your long-term returns. Even seemingly small percentages can compound into significant amounts over decades. You need to understand every fee structure.

- Advisory Fees: Often a percentage of assets under management (AUM), typically ranging from 0.5% to 1.5% annually.

- Transaction Fees/Commissions: Charged per trade, common with discount brokers.

- Expense Ratios: Fees embedded within mutual funds and ETFs, covering management and operating costs.

- Account Maintenance Fees: Charged for holding an account, though many firms waive these for larger balances.

Why this matters in real life: Let’s say you invest $100,000 expecting an 8% annual return. If you pay an extra 1% in fees (e.g., a 0.5% advisory fee plus a 0.5% fund expense ratio), your net return drops to 7%. Over 20 years, that 1% difference can cost you tens of thousands of dollars.

How to Calculate Your Potential Investment Growth (and Fee Impact)

Understanding the impact of fees is crucial. While calculating exact future returns is impossible due to market volatility, you can model how fees erode your potential gains.

To estimate your potential growth:

1. Start with your initial investment amount.

2. Add your expected annual contribution.

3. Multiply this total by your expected annual growth rate (e.g., 7% or 8%).

4. Then, subtract the total annual fees as a percentage of your total investment.

5. Repeat this for each year to see the compounding effect.

For example, if you start with $10,000, add $2,400 each year ($200/month), and expect 7% growth before fees, but pay 1.5% in fees, your net growth is 5.5%. This difference adds up rapidly.

INVESTMENT GROWTH ESTIMATOR

Why this matters in real life: This simple exercise reveals the profound impact of fees. A seemingly small 1% difference in fees can mean you retire with hundreds of thousands less. Always negotiate fees or choose providers known for their low-cost structure.

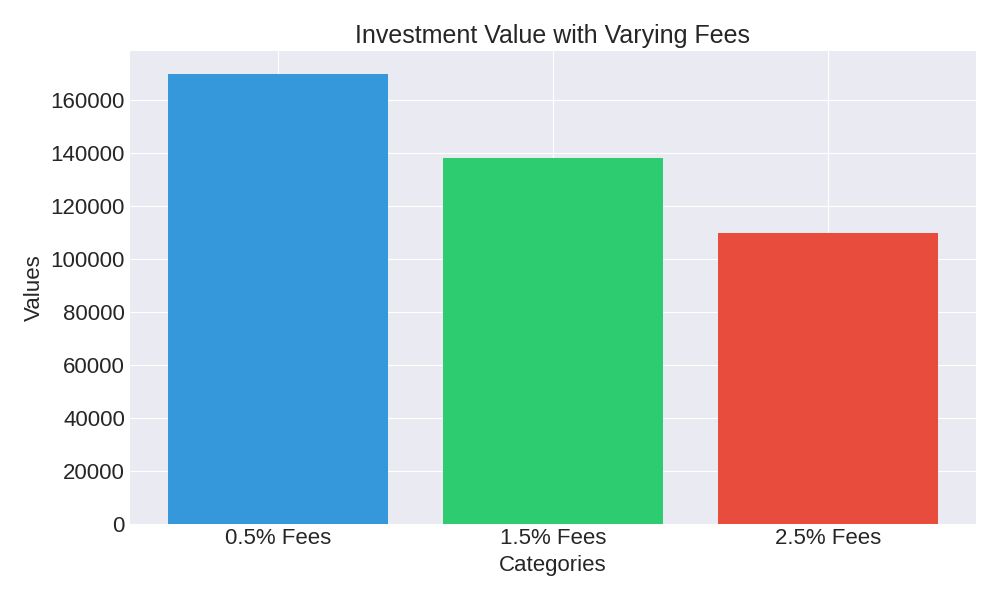

| Investment Scenario (Initial $10,000, $200/month contribution) | Projected Value (Year 5) | Projected Value (Year 10) | Projected Value (Year 20) |

|---|---|---|---|

| Scenario A: 7% Annual Return (0.5% Total Fees) | ~$26,000 | ~$58,000 | ~$170,000 |

| Scenario B: 7% Annual Return (1.5% Total Fees) | ~$24,800 | ~$53,000 | ~$138,000 |

| Scenario C: 7% Annual Return (2.5% Total Fees) | ~$23,600 | ~$48,000 | ~$110,000 |

(Note: These are illustrative projections based on consistent growth and contributions. Actual returns vary.)

The Power of Peer Reviews and Professional Endorsements

Beyond the regulatory checks, anecdotal evidence and third-party insights can provide valuable context. Don’t just rely on a company’s own marketing.

- Read Unbiased Reviews: Look for reviews on independent financial forums, consumer advocacy sites, or reputable financial news outlets. Sites like Bloomberg or others often publish rankings and reviews of financial services.

- Check Professional Ratings: Some firms receive ratings from organizations like J.D. Power for customer satisfaction or Morningstar for fund performance. While not the be-all and end-all, these can offer additional data points.

Insider Tip: Be wary of review sites that seem overly positive or negative without specific, verifiable details. Look for patterns in feedback regarding customer service, fee transparency, or platform usability. Generic praise or vague complaints are less helpful.

Identifying Red Flags and When to Walk Away

Your gut feeling is important, but there are concrete warning signs you must recognize:

- High-Pressure Sales Tactics: Any firm pushing you to make a decision quickly, without fully understanding the product or service, is a red flag. Real advisors empower you; they don’t pressure you.

- Unsolicited Offers: Be extremely cautious of cold calls, emails, or social media messages promoting “exclusive” investment opportunities from unknown entities.

- Lack of Transparency: If fees are vague, difficult to find, or explained confusingly, this is a major warning. Transparency is a cornerstone of trust.

- Promises of “Guaranteed” or “Too Good to Be True” Returns: Again, any investment promising high returns with no risk is a scam. Period.

Why this matters in real life: Recognizing these red flags protects you from losing money to fraudulent schemes or unsuitable investments. Your money is too valuable to risk on a sketchy deal.

Different Types of Investing Companies: Finding Your Match

Not all investing companies are created equal, and what’s right for your neighbor might be wrong for you.

- Full-Service Brokerages: Offer comprehensive financial planning, investment advice, and often proprietary products. Best for those who want hands-on guidance and don’t mind higher fees.

- Discount Brokerages: Provide platforms for self-directed investing with low fees or even commission-free trades. Ideal if you’re comfortable making your own investment decisions.

- Robo-Advisors: Automated, algorithm-driven platforms that manage diversified portfolios based on your risk tolerance. A great entry point for beginners or those seeking low-cost, hands-off management.

- Independent Financial Advisors: Often fiduciaries, these professionals offer personalized advice and can help you build a comprehensive financial plan. They typically charge AUM fees or hourly rates. For more on finding qualified advisors, explore resources like those from the National Association of Personal Financial Advisors (NAPFA).

Why this matters in real life: Understanding these options allows you to align a company’s services with your comfort level, desired level of involvement, and budget. Don’t pay for services you don’t need, but also don’t forgo essential guidance if you’re a beginner.

Conclusion: Empower Yourself, Invest Confidently

Finding trusted investing companies isn’t about luck; it’s about diligence. You now have the blueprint: vet regulatory status, understand fiduciary duty, scrutinize fees, and look for red flags. You are no longer a passive observer but an informed decision-maker.

The market can be daunting, but with the right partners, it can also be incredibly rewarding. Take control of your financial journey.

Your Call to Action: Start Vetting Today

Don’t delay. Pick one or two potential investing companies that align with your initial thoughts and apply this blueprint. Check their regulatory records, review their fee structures, and reach out with your questions. Your future self will thank you for taking these decisive steps now.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.