Feeling overwhelmed by the sheer complexity of finding decent, affordable healthcare? You’re not alone. The search for reliable coverage often feels like navigating a minefield of jargon, hidden costs, and confusing options. But let me tell you, as your financial strategist and consumer advocate, securing quality marketplace health insurance doesn’t have to be a nightmare.

You’re not just looking for a piece of paper; you’re looking for peace of mind. You want to know that when life throws a curveball – a sudden illness, an unexpected injury – you won’t be financially crippled. Your goal is smart protection without breaking the bank. And frankly, your fear is picking the wrong plan and ending up with huge bills or no coverage for your trusted doctors. Let’s cut through the noise and empower you to make an informed decision about your marketplace health insurance, right now.

Unmasking the Marketplace: What You NEED to Know

Forget the generic definitions. What you truly need to understand is how the tiers of marketplace plans directly impact your wallet and your access to care. The system uses metal categories: Bronze, Silver, Gold, and Platinum. This isn’t just about fancy names; it’s a critical balancing act between your monthly premium and what you pay when you actually use healthcare services.

Insider Tip: Don’t assume Bronze is always the “cheapest.” While it has the lowest monthly premiums, its high deductibles mean you pay a lot out-of-pocket before insurance kicks in. Conversely, Platinum plans have the highest premiums but minimal out-of-pocket costs when you get care. For many, Silver plans offer the best balance, especially if you qualify for extra savings.

Why this matters in real life: Imagine you’re generally healthy but anticipate one or two doctor visits a year and maybe a prescription. A Silver plan might be ideal. Your monthly payment is manageable, and your co-pays for routine care are reasonable. However, if you have a chronic condition requiring frequent doctor visits and medications, a Gold or Platinum plan, despite the higher premium, could save you thousands in deductibles and co-insurance over a year. It’s about predicting your usage, not just picking the lowest sticker price.

The Hidden Power of Subsidies: You Might Qualify for More Than You Think

One of the biggest myths I encounter is people believing they earn “too much” for financial assistance. This is often not true. The marketplace offers two main types of subsidies: Premium Tax Credits (PTC) and Cost-Sharing Reductions (CSR). These are game-changers for affordability.

- Premium Tax Credits (PTC): These credits directly lower your monthly premium. They are based on your household income and size. Many individuals and families earning up to 400% of the Federal Poverty Level (and even higher in some situations, depending on current laws) can qualify for significant help. This is money that you do not have to pay back, making coverage genuinely affordable.

- Cost-Sharing Reductions (CSR): This is an even more powerful, but less understood, subsidy. CSRs reduce your deductible, co-insurance, and co-pays. They are only available if you enroll in a Silver plan and your income falls within specific brackets (typically up to 250% of the Federal Poverty Level). This means a Silver plan can offer benefits almost as rich as a Gold plan, but at a much lower cost.

Why this matters in real life: Consider a single individual earning around $35,000 annually. Without subsidies, a mid-range plan might cost them $400-$500 a month. With PTC, that premium could drop to under $100. If their income is closer to $25,000, they might also qualify for CSRs on a Silver plan, meaning their deductible could be reduced from $5,000 to, say, $1,500. This dramatically changes their financial vulnerability. To explore your potential savings, visit the official marketplace at Healthcare.gov.

Calculating Your True Cost: Beyond the Monthly Premium

Your monthly premium is just one piece of the puzzle. To understand your true healthcare cost, you need to factor in several other components. This is where most people get tripped up, focusing only on the lowest monthly bill.

- Premium: Your fixed monthly payment for coverage.

- Deductible: The amount you must pay out of your own pocket for covered services before your insurance company starts to pay. Think of it as your “self-pay” threshold.

- Co-pay: A fixed amount you pay for a covered healthcare service (like a doctor’s visit or prescription) after you’ve met your deductible (though some plans have co-pays for certain services even before meeting the deductible).

- Co-insurance: Your share of the cost of a covered healthcare service, calculated as a percentage (e.g., 20%) of the allowed amount for the service. You pay this after you’ve met your deductible.

- Out-of-Pocket Maximum: The absolute most you will have to pay for covered services in a plan year. Once you hit this limit, your insurance plan pays 100% of the cost of covered benefits for the rest of the year. This is your ultimate financial safety net.

Why this matters in real life: Imagine you pick a Bronze plan with a $300 premium and a $7,000 deductible, versus a Silver plan with a $450 premium and a $3,000 deductible. If you have an unexpected surgery costing $10,000, with the Bronze plan, you’ll pay the first $7,000 plus your premiums. With the Silver plan, you’ll pay $3,000 plus your premiums. The difference in out-of-pocket expense is substantial, making the Silver plan far more protective despite its higher monthly premium. You need to consider what you’d pay in a worst-case scenario, not just the best case.

Here’s a practical way to estimate your costs:

1. Estimate Your Annual Healthcare Use: How many doctor visits? Any specialists? How many prescriptions? Are you planning a surgery or expecting a baby?

2. Add Up Potential Co-pays/Co-insurance: Based on your estimated usage and the plan’s specific rates.

3. Factor in the Deductible: If your estimated costs exceed the deductible, assume you’ll pay up to that amount (or a significant portion of it).

4. Consider the Out-of-Pocket Maximum: In a catastrophic scenario, this is your total risk.

5. Calculate Total Annual Cost: (Monthly Premium x 12) + (Estimated Out-of-Pocket Expenses: Deductible + Co-pays/Co-insurance up to the Out-of-Pocket Max).

For a more precise estimate, utilize the tools available:

Your Estimated Annual Healthcare Costs

Strategic Plan Selection: Insider Tips for Smarter Choices

Choosing the right plan involves more than just glancing at the metal category. You need a strategic approach to match your health needs with your financial reality.

Common Myth to Avoid: “All plans are the same, so just pick the cheapest.” Absolutely not! Plans differ widely in their provider networks, prescription drug coverage, and specific benefits. A cheap plan is useless if your trusted doctor isn’t in-network or your essential medication isn’t covered.

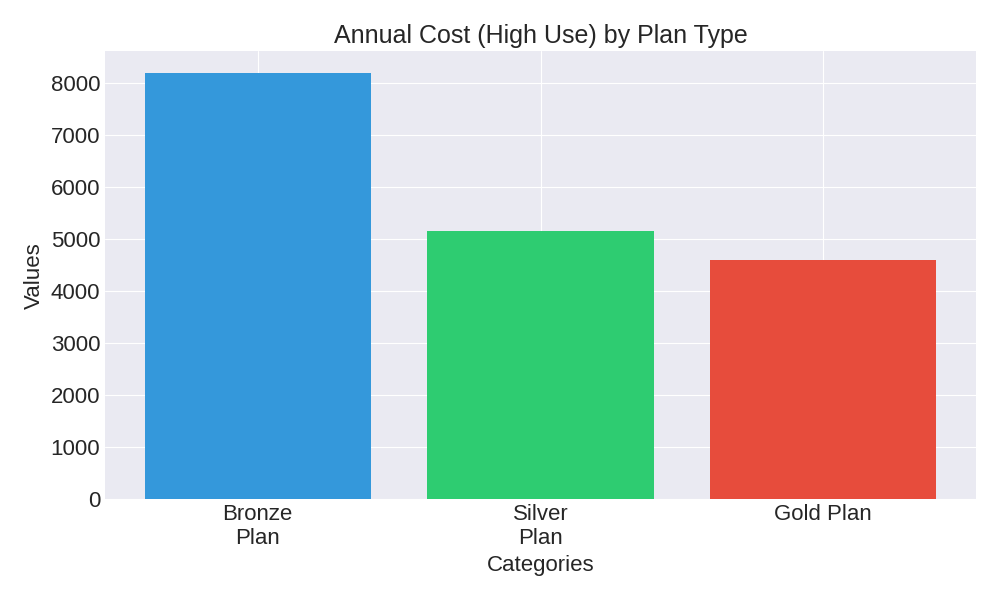

Here’s a comparison to illustrate how plan choices impact total cost over a year:

| Plan Feature | Bronze Plan (Scenario A) | Silver Plan (Scenario B) | Gold Plan (Scenario C) |

|---|---|---|---|

| Monthly Premium (after subsidies) | $100 – $150 | $180 – $250 | $300 – $400 |

| Deductible | $6,000 – $8,500 | $2,500 – $4,500 | $500 – $1,500 |

| Out-of-Pocket Maximum | $7,500 – $9,100 | $7,000 – $8,700 | $6,000 – $8,000 |

| Typical Doctor Visit Co-pay (after deductible) | 20% – 30% Co-insurance | $30 – $60 | $15 – $40 |

| Est. Total Annual Cost (Low Use: 2 doctor visits, no major issues) | $1,200 (premiums) + $150 (co-pays) = ~$1,350 | $2,160 (premiums) + $80 (co-pays) = ~$2,240 | $3,600 (premiums) + $50 (co-pays) = ~$3,650 |

| Est. Total Annual Cost (High Use: minor surgery, Rx, several visits) | $1,200 (premiums) + $7,000 (deductible) = ~$8,200 | $2,160 (premiums) + $3,000 (deductible) = ~$5,160 | $3,600 (premiums) + $1,000 (deductible) = ~$4,600 |

Pro/Con: HMO vs. PPO. These are common types of provider networks. HMOs (Health Maintenance Organizations) typically have lower premiums and require you to choose a primary care physician (PCP) who refers you to specialists. They don’t usually cover out-of-network care. PPOs (Preferred Provider Organizations) offer more flexibility, allowing you to see specialists without a referral and often providing some coverage for out-of-network providers, though at a higher cost. This flexibility comes with higher premiums.

Why this matters in real life: If you value having control over specialist visits and potentially seeing out-of-network doctors, a PPO might be worth the higher premium. If you’re comfortable with a structured network and a PCP managing your referrals, an HMO could save you money. Always check if your current doctors are in a plan’s network before enrolling. Websites like Consumer Reports offer great advice on understanding health plan types.

Special Enrollment Periods (SEPs): Your Lifelines

Did you miss the annual Open Enrollment? Don’t panic. If you’ve experienced certain qualifying life events, you may be eligible for a Special Enrollment Period (SEP). This allows you to enroll in or change your health plan outside of the regular window.

Common qualifying events include:

- Marriage or divorce.

- Birth of a child, adoption, or placement for adoption.

- Moving to a new area that offers different health plans.

- Losing other health coverage (e.g., job loss, aging off a parent’s plan, COBRA ending).

- Changes in income that affect your eligibility for subsidies.

Why this matters in real life: Life happens. If you suddenly lose your job and your employer-sponsored coverage, an SEP ensures you don’t go uninsured. It’s a critical safety net that you should be aware of, giving you 60 days from the event to enroll.

Avoiding Common Pitfalls and Ensuring Coverage

Navigating marketplace health insurance can be tricky, but knowing the common traps can help you steer clear of trouble.

Myth to Avoid: “It’s okay to estimate my income when applying.” Your income estimate is crucial because it determines your subsidy eligibility. Underestimating your income could lead to receiving too much in premium tax credits, which you might have to pay back at tax time. Overestimating could mean you miss out on valuable assistance.

Pro Tip: Be as accurate as possible with your income projections. If your income changes significantly during the year, update your information on your marketplace account immediately. This helps adjust your subsidies in real-time, preventing surprises later. The IRS provides guidance on how premium tax credits interact with your taxes; check IRS.gov for details.

Why this matters in real life: Imagine you got $300 a month in subsidies based on an income estimate. If your income ends up being higher than projected, you might owe $3,600 back to the IRS when you file taxes. That’s a huge unexpected bill. Staying current with your income updates protects your financial stability.

You have the power to choose wisely. Don’t let the complexity deter you from securing essential healthcare coverage. By understanding the true cost, leveraging available subsidies, and selecting a plan that genuinely fits your needs, you can protect your health and your financial future.

Your journey to affordable, reliable coverage starts now. Explore your options, use the tools, and remember: an informed decision is your best defense against unexpected medical bills.

Call to Action: Don’t wait until you’re sick. Visit your state’s Health Insurance Marketplace or Healthcare.gov today to explore plans and see what subsidies you qualify for. Take control of your healthcare future.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.