Bringing a dog into your home fills it with unconditional love, boundless energy, and endless tail wags. However, along with the joy comes the significant responsibility of ensuring their health and well-being. Unexpected vet bills, often totaling thousands of dollars, can quickly turn a loving bond into a financial strain. This is where insurance for dogs steps in, offering a crucial safety net for your furry family member.

Insurance for dogs helps pet owners manage the often unpredictable costs of veterinary care, from sudden accidents to chronic illnesses. Understanding the ins and outs of pet insurance can safeguard your finances and ensure your canine companion receives the best possible treatment without compromise.

Why Consider Pet Insurance for Your Dog?

Veterinary care costs have been on a steady rise, driven by advancements in medicine and technology. What was once considered a minor procedure can now involve complex diagnostics, specialized treatments, and rehabilitation. Without adequate planning, a severe illness or injury could force difficult decisions about your pet’s care.

Pet insurance offers peace of mind. It allows you to focus on your dog’s recovery rather than the escalating costs. Many pet parents find it invaluable for managing emergencies, cancer treatments, or lifelong conditions that require ongoing medication and specialist visits.

The Rising Cost of Vet Care

The average cost of treating common canine ailments can be substantial. For instance, emergency surgery for a broken bone might range from $2,000 to $5,000, while cancer treatments can exceed $10,000. Chronic conditions like diabetes or arthritis require continuous management, adding up significantly over a dog’s lifetime.

According to the American Veterinary Medical Association (AVMA), pets are living longer, healthier lives thanks to improved veterinary care, which can also mean more opportunities for age-related illnesses. Protecting your pet with a robust insurance plan is a proactive step against these financial challenges.

Types of Dog Insurance Coverage

Understanding the different types of pet insurance policies is crucial for selecting the right plan for your dog. Each offers varying levels of protection and comes with its own set of benefits and limitations.

- Accident-Only Plans: These are the most basic and typically the most affordable plans. They cover injuries resulting from accidents, such as broken bones, swallowed objects, or car accidents. They do not cover illnesses, hereditary conditions, or routine care.

- Accident & Illness Plans: This is the most common and comprehensive type of pet insurance. It covers both accidents and a wide range of illnesses, including infections, cancer, digestive issues, and chronic conditions. Most accident & illness plans also cover diagnostics, surgeries, hospitalization, and prescription medications.

- Wellness Plans (Add-Ons): These are not standalone insurance policies but optional additions to an accident & illness plan. They cover routine preventative care like annual check-ups, vaccinations, flea and tick prevention, and dental cleanings. While helpful, they are often paid out on a fixed schedule and may not be the most cost-effective for every pet owner.

- Hereditary & Congenital Conditions: Many comprehensive plans now cover breed-specific or congenital conditions like hip dysplasia or certain heart defects, provided the condition isn’t pre-existing when you enroll. This coverage is particularly important for breeds known to have such predispositions.

Understanding Pet Insurance Costs

Several factors influence the monthly premium you’ll pay for insurance for dogs. Being aware of these elements helps you make an informed decision and budget accordingly.

Key Cost Factors

- Breed: Some breeds are predisposed to certain health issues, leading to higher premiums. For example, large breeds prone to hip dysplasia may cost more to insure.

- Age: Younger dogs are generally cheaper to insure than older dogs, who are more susceptible to age-related illnesses. It’s often best to get coverage when your dog is a puppy.

- Location: Veterinary costs vary by region, and your premium will reflect the average cost of care in your area.

- Coverage Level: More comprehensive plans with higher reimbursement rates and lower deductibles will naturally have higher premiums.

Deductibles, Reimbursement, and Annual Limits

These three terms are fundamental to how pet insurance plans operate:

- Deductible: This is the amount you must pay out-of-pocket before your insurance coverage kicks in. Deductibles can be annual (once per year) or per-incident. Common deductibles range from $100 to $1,000. A higher deductible usually means a lower monthly premium.

- Reimbursement Level: This is the percentage of the covered vet bill that the insurance company will pay after your deductible is met. Common reimbursement levels are 70%, 80%, or 90%. If your plan has an 80% reimbursement level, you are responsible for the remaining 20% of the bill.

- Annual Limit: Most plans have a maximum amount they will pay out in a policy year. This can range from a few thousand dollars to unlimited coverage. Higher annual limits offer more protection but come with higher premiums.

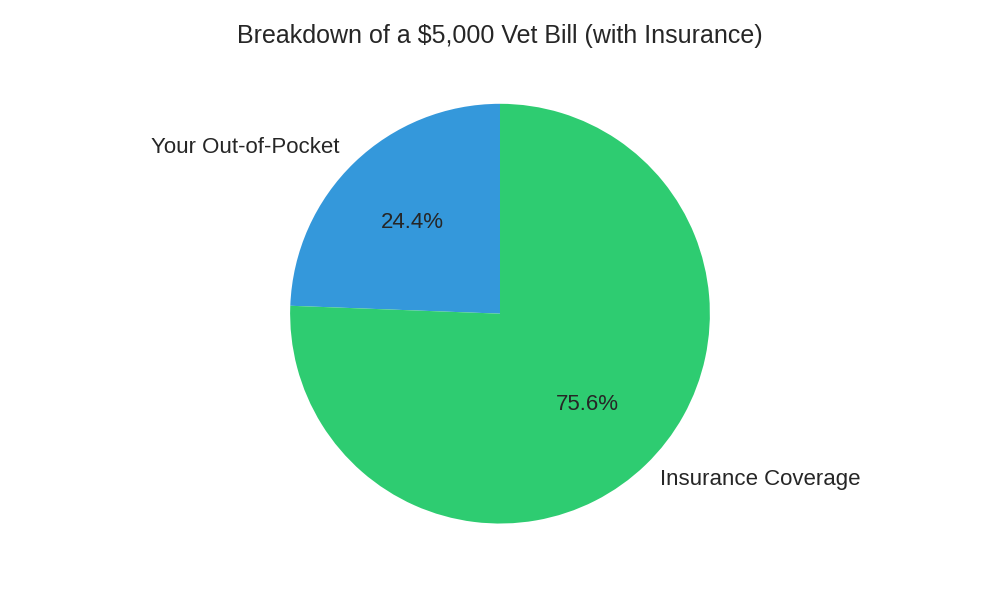

Cost Impact of a Major Vet Bill: Scenario Comparison Table

To illustrate how these factors affect your actual out-of-pocket costs, consider a hypothetical $5,000 vet bill for an emergency surgery. This table demonstrates the financial impact under different deductible scenarios, assuming an 80% reimbursement rate once the deductible is met. This simplified approach helps you grasp the practical benefits of pet insurance.

| Scenario | Annual Deductible | Your Final Out-of-Pocket Cost |

|---|---|---|

| No Insurance | N/A | $5,000 |

| Plan with $250 Deductible | $250 | $1,200 (Deductible + 20% of $4,750) |

| Plan with $500 Deductible | $500 | $1,400 (Deductible + 20% of $4,500) |

| Plan with $1,000 Deductible | $1,000 | $1,800 (Deductible + 20% of $4,000) |

How to Choose the Best Plan for Your Dog

Selecting the ideal pet insurance plan involves careful consideration of your dog’s needs, your budget, and the specific terms of various providers. It’s not a one-size-fits-all decision.

Key Factors to Evaluate

- Pre-existing Conditions: Most policies do not cover conditions that were present before the policy started or during a waiting period. Be clear on how each insurer defines and handles these.

- Waiting Periods: There’s typically a waiting period (e.g., 2-14 days for accidents, 14-30 days for illnesses, longer for orthopedic conditions) before coverage begins.

- Customization Options: Look for plans that allow you to adjust deductibles, reimbursement percentages, and annual limits to fit your budget.

- Customer Reviews and Reputation: Research the insurer’s reputation for customer service, claim processing, and transparency. Sites like NerdWallet often provide comparative reviews.

- Direct Vet Pay: Some insurers offer the option to pay your vet directly, rather than you paying upfront and waiting for reimbursement. This can be a significant benefit for large bills.

Step-by-Step Guide to Getting Dog Insurance

Navigating the process of obtaining pet insurance can seem daunting, but breaking it down into manageable steps makes it straightforward.

- Research Providers: Start by researching reputable pet insurance companies. Look at their coverage options, customer reviews, and financial stability.

- Gather Information About Your Dog: You’ll need your dog’s breed, age, and any existing medical history. Be honest about pre-existing conditions.

- Get Multiple Quotes: Obtain quotes from at least three different providers. Compare their offerings side-by-side, paying close attention to deductibles, reimbursement rates, annual limits, and exclusions.

- Read the Fine Print: Carefully review the policy document for exclusions, waiting periods, and how claims are processed. Understand what is covered and what isn’t. The Federal Trade Commission (FTC) provides valuable tips on understanding consumer protections in insurance.

- Choose Your Plan: Select the plan that best fits your dog’s needs and your financial situation. Consider whether an accident-only, accident & illness, or a comprehensive plan with wellness add-ons is appropriate.

- Enroll and Pay Your First Premium: Once enrolled, your coverage will begin after the specified waiting periods. Keep your policy documents accessible.

Making a Claim

When your dog needs vet care, the claims process typically involves:

- Pay Your Vet: Most pet insurance plans operate on a reimbursement model. You pay the vet bill upfront at the time of service.

- Submit a Claim: Fill out a claim form, usually available online or via the insurer’s app, and submit it.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.