Navigating the world of insurance health plans can feel overwhelming, like deciphering a complex code. Yet, choosing the right coverage is one of the most critical financial and health decisions you’ll make. A well-selected health plan protects you from unforeseen medical costs and ensures access to necessary care. This comprehensive guide will demystify the process, helping you understand your options and confidently select the perfect and affordable insurance health plans tailored to your needs.

Understanding the Basics of Health Insurance

Before diving into specific plans, it’s essential to grasp the fundamental terminology that underpins all insurance health plans. Familiarity with these terms will empower you to compare options effectively and make informed choices.

What is Health Insurance?

Health insurance is a contract that requires an insurer to pay some or all of a person’s medical expenses in exchange for a premium. It protects you from high, unexpected healthcare costs, ensuring you can afford necessary doctor visits, hospital stays, prescription drugs, and preventive care.

Here are key terms you’ll encounter:

- Premium: The amount you pay monthly to your insurance company, regardless of whether you use medical services. This is the regular cost of having coverage.

- Deductible: The amount you must pay out of pocket for covered medical services before your insurance plan starts to pay. For example, if your deductible is $2,000, you pay the first $2,000 of your medical bills yourself each year.

- Copayment (Copay): A fixed amount you pay for a covered health service after you’ve paid your deductible. For instance, a $30 copay for a doctor’s visit.

- Coinsurance: Your share of the cost of a covered health service, calculated as a percentage (e.g., 20%) after you’ve met your deductible. If your coinsurance is 20% and the bill is $1,000 after your deductible, you pay $200.

- Out-of-Pocket Maximum: The most you have to pay for covered services in a plan year. After you reach this amount, your health plan pays 100% of the cost of covered benefits. This limit includes deductibles, copayments, and coinsurance.

Types of Insurance Health Plans

The structure of a health plan dictates how you access care and what you pay. Understanding these common types will help you narrow down your choices:

- Health Maintenance Organization (HMO): These plans generally limit coverage to care from doctors who work for or contract with the HMO. They often require you to choose a primary care physician (PCP) who refers you to specialists. HMOs typically have lower premiums.

- Preferred Provider Organization (PPO): PPOs offer more flexibility. You don’t usually need a PCP referral to see a specialist, and you can see out-of-network providers, though at a higher cost. Premiums tend to be higher than HMOs.

- Exclusive Provider Organization (EPO): EPOs are similar to PPOs but will not cover care outside of the plan’s network, except in an emergency. You don’t need a PCP referral for specialists within the network.

- Point of Service (POS): POS plans combine elements of HMO and PPO plans. You typically need a PCP referral for specialists, but you can go out-of-network for care, usually at a higher cost.

- High Deductible Health Plan (HDHP): These plans feature higher deductibles than traditional plans but often come with lower monthly premiums. They can be combined with a Health Savings Account (HSA) to pay for qualified medical expenses with pre-tax dollars.

Navigating the Health Insurance Marketplace

Finding the right coverage means knowing where to look and what factors are most important for your unique situation. The marketplace offers various avenues to secure health coverage.

Where to Find Insurance Health Plans

Your options for obtaining coverage are diverse, catering to different employment statuses, income levels, and life stages:

- Employer-Sponsored Plans: Many people get coverage through their job. Employers often subsidize a significant portion of the premiums.

- Health Insurance Marketplace (Healthcare.gov): Established by the Affordable Care Act (ACA), the federal and state marketplaces offer various plans from private insurers. You may be eligible for subsidies (premium tax credits) to lower your monthly costs based on your income. You can explore plans and eligibility at Healthcare.gov.

- Private Insurers: You can purchase plans directly from insurance companies outside the marketplace. However, you won’t be eligible for ACA subsidies this way.

- Medicaid: A joint federal and state program that provides health coverage to millions of low-income Americans, including children, pregnant women, elderly adults, and people with disabilities. Eligibility varies by state.

- Medicare: The federal health insurance program for people aged 65 or older, certain younger people with disabilities, and people with End-Stage Renal Disease.

Key Factors to Consider When Choosing a Plan

Selecting among the myriad of insurance health plans requires careful evaluation of your personal circumstances. Consider these factors:

- Your Budget: Balance monthly premiums with potential out-of-pocket costs (deductibles, copays, coinsurance). A lower premium often means a higher deductible, and vice versa.

- Your Health Needs: Do you have chronic conditions, require frequent doctor visits, or take regular prescription medications? A plan with lower deductibles and copays might be more cost-effective for high users of healthcare.

- Doctor and Hospital Networks: Ensure your preferred doctors, specialists, and hospitals are in the plan’s network. Out-of-network care can be significantly more expensive.

- Prescription Drug Coverage: Check the plan’s formulary (list of covered drugs) to ensure your medications are included and understand their cost tiers.

- Anticipated Services: If you’re planning for surgery, pregnancy, or other major medical events, compare how different plans cover these specific services.

Decoding Costs: Premiums, Deductibles, and More

Understanding how different costs interact is crucial for predicting your total healthcare expenses. It’s not just about the premium; the deductible, copay, and coinsurance all play a significant role in your financial outlay for medical care.

For instance, a plan with a low premium might seem attractive initially. However, if it comes with a high deductible and high coinsurance, you could end up paying a substantial amount out-of-pocket before your insurance truly kicks in, especially if you have significant medical needs. Conversely, a higher premium often means a lower deductible and lower out-of-pocket costs when you receive care.

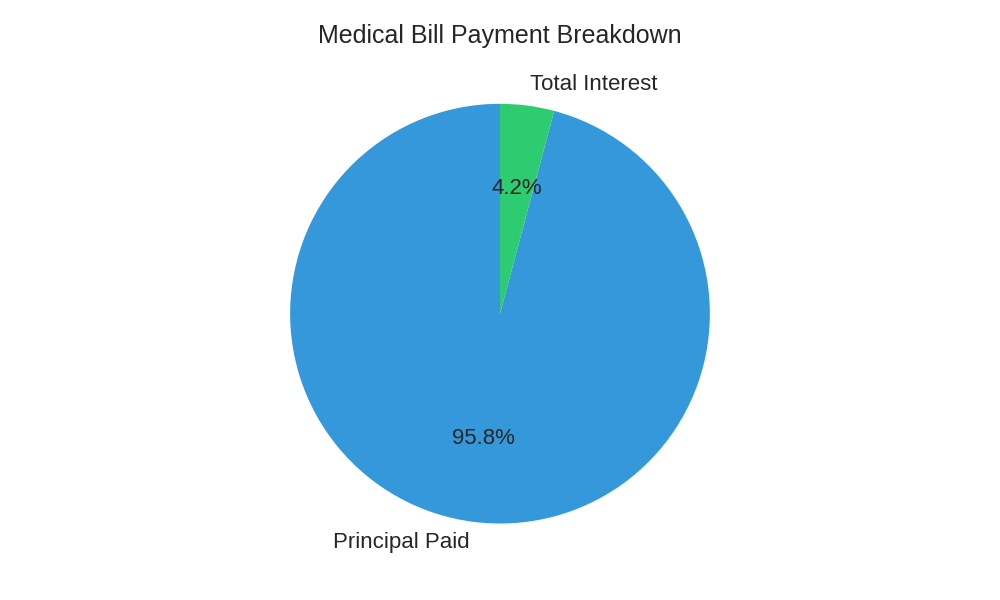

When faced with a significant medical expense, such as a high deductible or a portion of a bill not covered by insurance, you might need to consider payment options. If you were to finance a $5,000 medical bill, for example, over 12 months at an annual interest rate of 8%, understanding your repayment schedule is key to managing your finances. This illustrates how even with insurance, large medical costs can still require careful financial planning.

| Month | Monthly Payment | Remaining Balance |

|---|---|---|

| 1 | $434.94 | $4,598.40 |

| 2 | $434.94 | $4,193.36 |

| 3 | $434.94 | $3,784.86 |

| 4 | $434.94 | $3,372.88 |

| 5 | $434.94 | $2,957.39 |

| 6 | $434.94 | $2,538.35 |

| 7 | $434.94 | $2,115.74 |

| 8 | $434.94 | $1,689.52 |

| 9 | $434.94 | $1,259.66 |

| 10 | $434.94 | $826.13 |

| 11 | $434.94 | $388.90 |

| 12 | $391.56 | $0.00 |

| Total Paid: | $5,216.70 (includes ~$216.70 in interest) | |

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.