Finding the right insurance can feel like a maze, but it’s a critical financial decision that protects your assets and future. Many people wonder, “How can I find the best insurance near me?” The direct answer is through a systematic comparison process that combines understanding your needs with researching local providers. This guide will equip you with the knowledge and steps to confidently compare local rates and secure the optimal coverage, ensuring you don’t overpay for your peace of mind. Whether you’re searching for auto, home, or health insurance near me, the principles remain the same: clarity, comparison, and informed choice.

Understanding Your Insurance Needs

Before you even start looking for “insurance near me,” it’s essential to define what you’re trying to protect. This isn’t just about checking a box; it’s about safeguarding your financial well-being against unexpected events. Different types of insurance serve different purposes, from covering your vehicle after an accident to protecting your home from natural disasters.

Why this matters in real life: Imagine you’re a homeowner. Without proper home insurance, a severe storm could cause tens of thousands of dollars in damage, leaving you financially devastated. Conversely, if you purchase excessive coverage you don’t need, you’re simply throwing money away each month. Knowing your specific risks helps tailor your coverage effectively.

Common Types of Insurance to Consider

- Auto Insurance: Protects you financially in case of a car accident, theft, or damage to your vehicle. Liability coverage is often legally required.

- Homeowners/Renters Insurance: Covers your dwelling and belongings against perils like fire, theft, and natural disasters. Renters insurance specifically protects your possessions and offers liability coverage if someone is injured in your rented space.

- Health Insurance: Helps cover medical expenses, prescription drugs, and other healthcare services. Crucial for managing the high costs of healthcare.

- Life Insurance: Provides financial security for your loved ones after your passing, covering expenses like mortgages, education, or daily living costs.

- Disability Insurance: Replaces a portion of your income if you become unable to work due to illness or injury.

Key Factors Influencing Your Insurance Rates

Insurance premiums aren’t arbitrary; they’re based on a complex calculation of risk. Understanding these factors can empower you to take steps to lower your costs. Local demographics, crime rates, and even common weather patterns significantly impact what providers charge.

Why this matters in real life: Consider two drivers: one with a perfect record living in a low-crime suburb, and another with a few speeding tickets living in an urban area with high auto theft rates. The latter will almost certainly pay significantly more for auto insurance. Knowing these influences helps you understand quotes and potentially modify your risk profile.

Factors That Affect Premiums

- Location: Your zip code heavily influences rates due to factors like crime rates, traffic density, and local repair costs.

- Demographics: Age, gender (in some states), marital status, and credit score (where permitted) can impact rates. Insurers use these to assess risk.

- Coverage Level and Deductible: Higher coverage limits mean higher premiums. A higher deductible (the amount you pay out-of-pocket before insurance kicks in) typically results in lower premiums.

- Claims History: A history of past claims signals higher risk to insurers, leading to increased rates.

- Asset-Specific Factors: For auto insurance, the make, model, and safety features of your car matter. For homeowners insurance, the age, construction, and safety features of your home are crucial.

The Step-by-Step Guide to Comparing Local Rates

Comparing insurance isn’t just about picking the lowest number. It’s about finding the best value – the right coverage at a competitive price. This systematic approach ensures you consider all critical aspects.

Why this matters in real life: Imagine you receive two auto insurance quotes. One is significantly cheaper, but you later discover it offers minimal liability and a very high deductible, leaving you exposed to massive out-of-pocket costs after a minor accident. A thorough comparison prevents such costly mistakes.

1. Assess Your Current Coverage and Needs

Start by reviewing your existing policies (if any) or listing what you need to protect. Consider your assets, lifestyle, and potential risks. For example, if you’ve recently installed a home security system, that might qualify you for discounts on homeowners insurance.

2. Gather Necessary Information

Have all relevant details ready before requesting quotes. This includes personal identification, property details (address, age of home, safety features), vehicle information (VIN, mileage, safety features), and your claims history. This makes the quoting process smoother and more accurate.

3. Get Quotes from Multiple Providers

This is where finding “insurance near me” truly begins. Don’t settle for the first quote. Reach out to at least 3-5 different insurance companies. You can do this through:

- Online Comparison Tools: Many websites allow you to enter your information once and receive multiple quotes.

- Independent Insurance Agents: These agents work with various companies and can shop around for you, often finding competitive rates.

- Direct Insurers: Contact companies directly, either online or by phone.

The National Association of Insurance Commissioners (NAIC) offers valuable resources for understanding state-specific regulations and finding reliable companies.

4. Compare Apples to Apples

When reviewing quotes, look beyond the premium amount. Ensure you’re comparing policies with similar coverage limits, deductibles, and endorsements. A lower premium might indicate less coverage, which isn’t always a good deal.

5. Look for Discounts

Many insurers offer a variety of discounts. These can include multi-policy discounts (bundling auto and home), good driver discounts, safe home discounts (for security systems), or even professional affiliation discounts. Always ask what’s available.

6. Read Reviews and Check Financial Strength

A good price is meaningless if the company won’t pay out when you need them. Check customer reviews on sites like ConsumerReports.org and look up financial strength ratings from agencies like A.M. Best or Standard & Poor’s. A strong rating indicates the company’s ability to meet its financial obligations.

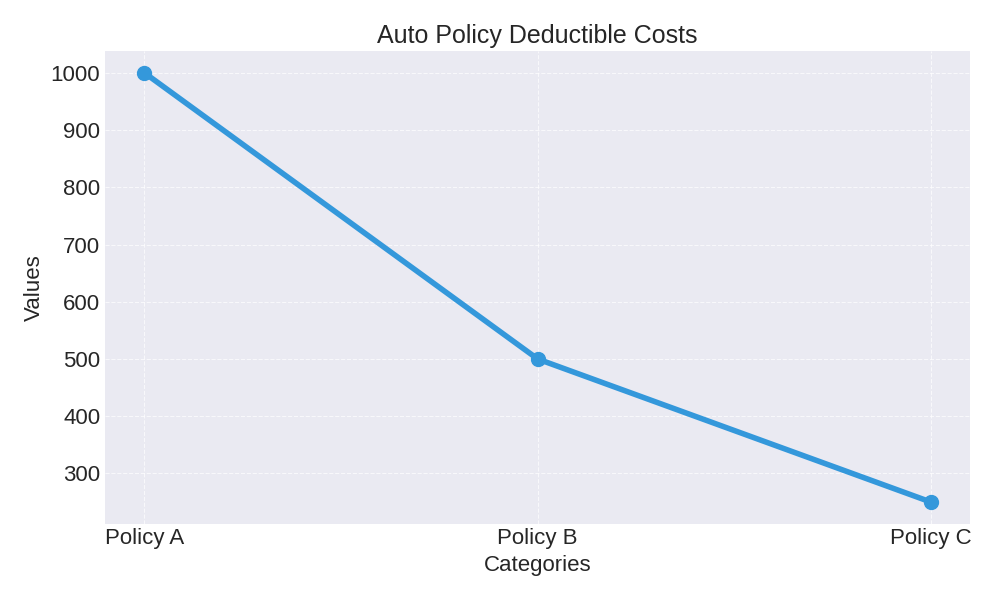

Example Scenario: Auto Insurance Comparison

Let’s say you’re comparing three auto insurance policies:

| Policy Feature | Policy A (Basic) | Policy B (Standard) | Policy C (Premium) |

|---|---|---|---|

| Liability Coverage | $25k/$50k/$10k | $100k/$300k/$50k | $250k/$500k/$100k |

| Collision Deductible | $1,000 | $500 | $250 |

| Comprehensive Deductible | $1,000 | $500 | $250 |

| Roadside Assistance | No | Yes | Yes |

| Rental Car Reimbursement | No | Limited | Full |

| Estimated Annual Premium | $1,200 – $1,500 | $1,800 – $2,200 | $2,500 – $3,000 |

While Policy A looks cheapest upfront, its low liability limits could leave you personally responsible for significant damages in a severe accident. Policy B offers a good balance, and Policy C provides maximum protection with lower out-of-pocket costs if you file a claim, but at a higher annual premium. Your choice depends on your risk tolerance and budget.

Calculating Your Potential Savings

Understanding your costs and potential savings doesn’t require complex mathematical formulas. It’s more about comparing the value you receive for your premium. This helps you quantify the benefit of switching or optimizing your policy.

Why this matters in real life: By calculating savings, you move from a gut feeling to a concrete financial decision. For example, if switching providers saves you $300 annually, that’s $300 more in your pocket for other financial goals or emergencies.

How to Estimate Your Savings

To estimate your savings when looking for “insurance near me,” follow these plain-language steps:

- Current Annual Cost: Look at your current insurance policy’s total annual premium. If you pay monthly, multiply that by 12.

- New Annual Cost: Take the lowest annual premium from a new quote that offers comparable or better coverage.

- Subtract: Take your new annual cost and subtract it from your current annual cost.

- The Result: The number you get is your estimated annual savings.

For example, if your current policy costs $2,000 per year and a new comparable policy costs $1,700 per year, your estimated annual savings would be $300.

You can also consider the long-term impact of deductibles. A policy with a $500 deductible might have a higher premium than one with a $1,000 deductible. Calculate the difference in premium over several years versus the extra out-of-pocket expense if you ever file a claim. This helps you decide if the lower premium with a higher deductible is truly saving you money in the long run, especially if you rarely file claims.

For deeper insights into managing insurance costs and overall financial planning, resources like Investopedia.com can be very helpful.

Insurance Savings Estimator

Common Questions About Finding Local Insurance (FAQ)

Q1: Can my credit score affect my insurance rates?

A: Yes, in many states, insurers use a credit-based insurance score as one factor in determining your premium. A higher score often indicates lower risk and can lead to lower rates. However, some states have banned or restricted the use of credit scores for insurance.

Q2: Is it better to go with a large national insurer or a smaller local company?

A: Both have pros and cons. Large national insurers often have extensive resources, broad coverage options, and strong financial stability. Smaller local companies or independent agents might offer more personalized service and a deeper understanding of local risks. It’s wise to get quotes from both types to compare.

Q3: How often should I compare insurance rates?

A: It’s a good practice to compare rates at least once a year, or whenever you experience a significant life event. This includes moving to a new area, buying a new car or home, getting married, or having a change in your credit score. Market rates and your personal circumstances change, so regular checks can save you money.

Q4: What’s the difference between an insurance agent and a broker?

A: An insurance agent typically represents one or more specific insurance companies and sells their products. An insurance broker works for you, the client, and shops around with many different companies to find the best policy that fits your needs. Independent agents often function similarly to brokers.

Q5: Does bundling policies actually save money?

A: Most often, yes! Many insurance companies offer discounts if you purchase multiple policies (e.g., auto and home) from them. This “multi-policy discount” can be substantial, making bundling a smart strategy to reduce your overall insurance costs.

Conclusion

Finding the best “insurance near me” isn’t about guesswork; it’s about being informed and methodical. By understanding your needs, knowing what influences your rates, and systematically comparing options, you can secure robust protection without overspending. Remember that insurance is an investment in your financial security, so making an educated decision is paramount.

Ready to Compare and Save?

Take control of your finances today. Use the strategies outlined in this guide to start comparing local insurance rates. Get quotes from multiple providers, ask about discounts, and choose the policy that offers the best value for your specific needs. Your peace of mind is worth the effort!

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.