Embarking on the journey to financial freedom often feels daunting, but it doesn’t have to be. The most crucial first step for many is understanding and opening an investing account. This guide will demystify the process, explain complex concepts in clear terms, and provide actionable steps to help you leverage an investing account as a powerful tool for building wealth.

In essence, an investing account is a dedicated financial account used to hold various investment vehicles like stocks, bonds, mutual funds, and exchange-traded funds (ETFs). It’s your personal portal to the financial markets, allowing your money to grow over time through the power of compounding. Think of it as your strategic command center for future prosperity.

What is an Investing Account?

An investing account is a specific type of financial account established with a brokerage firm or financial institution. Unlike a regular savings account, which typically offers minimal interest, an investing account is designed for purchasing and holding assets that have the potential for higher returns.

These accounts provide access to a wide array of investment opportunities. They serve as the legal and administrative framework for managing your investments, tracking their performance, and handling transactions. Your choice of an investing account depends heavily on your financial goals, time horizon, and tax considerations.

Why Open an Investing Account?

Opening an investing account unlocks several key benefits that are fundamental to long-term financial health:

- Wealth Accumulation: It allows your money to work for you, growing through capital appreciation and dividends.

- Inflation Protection: Investments often outpace inflation, preserving your purchasing power over time.

- Goal Achievement: Essential for funding significant life goals like retirement, a down payment on a home, or your children’s education.

- Diversification: Enables you to spread risk across various assets, reducing reliance on a single investment.

Types of Investing Accounts

The world of investing accounts offers a variety of structures, each with unique features and tax implications. Understanding these differences is crucial for selecting the right option for your specific needs.

Taxable Brokerage Accounts

These are the most common and flexible types of investing accounts. Funds deposited into a taxable brokerage account are post-tax, meaning you’ve already paid income tax on them. Any capital gains or dividends generated within this account are typically subject to taxes in the year they are realized or received.

- Flexibility: No limits on contributions (beyond individual brokerage policies) and funds can be withdrawn at any time without age restrictions or penalties.

- Investment Options: Offers the broadest range of investment products, including stocks, bonds, mutual funds, ETFs, and options.

- Ideal For: Short-term goals, emergency funds that need growth, or supplemental investing beyond tax-advantaged accounts.

Retirement Accounts

Designed specifically for retirement savings, these accounts offer significant tax advantages to encourage long-term investing. The U.S. government provides these benefits, which you can learn more about through official sources like the IRS.

- Individual Retirement Arrangements (IRAs):

- Traditional IRA: Contributions may be tax-deductible, reducing your taxable income now. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are made with after-tax money, but qualified withdrawals in retirement are entirely tax-free.

- Employer-Sponsored Plans (e.g., 401(k), 403(b)):

- Offered through your workplace, these allow pre-tax contributions to grow tax-deferred. Many employers offer matching contributions, which is essentially “free money” for your retirement.

- Like Traditional IRAs, withdrawals in retirement are taxed as ordinary income. Some plans also offer a Roth 401(k) option.

Specialty Accounts

Beyond general investing and retirement, specific accounts cater to niche financial goals:

- 529 Plans: Tax-advantaged savings plans designed to encourage saving for future education costs.

- Health Savings Accounts (HSAs): A triple tax-advantaged account (tax-deductible contributions, tax-free growth, tax-free withdrawals for qualified medical expenses) available to those with high-deductible health plans.

How to Choose the Right Investing Account

Selecting the best investing account involves aligning it with your personal financial situation and objectives. Consider these crucial factors:

Your Financial Goals

Are you saving for a short-term goal (e.g., a down payment in 3-5 years) or a long-term one (e.g., retirement in 30 years)? Short-term goals might favor taxable brokerage accounts for liquidity, while long-term goals strongly benefit from the tax advantages of retirement accounts.

Time Horizon

The length of time you have until you need the money significantly impacts your investment strategy and account choice. Longer time horizons allow for more aggressive investments and greater compounding potential within tax-advantaged accounts.

Risk Tolerance

How comfortable are you with the potential for your investment value to fluctuate? Your comfort level with risk will influence the types of assets you choose to hold within your investing account. Always ensure your investments align with your personal risk profile.

Tax Implications

Understanding the tax treatment of contributions, earnings, and withdrawals is paramount. Taxable accounts offer flexibility but often lead to annual tax liabilities on gains. Retirement accounts provide tax benefits upfront or upon withdrawal, depending on the type, but come with withdrawal restrictions.

Steps to Open an Investing Account

Opening an investing account is a straightforward process once you’ve decided on the type of account that suits you best. Here are the typical steps:

- Define Your Goals: Clarify what you’re saving for and your timeline. This will guide your account choice.

- Choose a Brokerage Firm: Research different online brokers or financial advisors. Compare fees, available investment products, customer service, and educational resources. Reputable sites like FINRA can help you check brokerage firms and professionals.

- Select Account Type: Based on your goals and tax situation, decide between a taxable brokerage account, IRA, Roth IRA, etc.

- Gather Required Information: You’ll typically need your Social Security number, driver’s license or state ID, and bank account information for funding.

- Complete the Application: Most brokerage applications are online and take about 10-15 minutes to complete.

- Fund Your Account: Link your bank account to transfer funds. You can often set up recurring deposits to automate your savings.

- Choose Your Investments: Once funded, you can start selecting investments that align with your risk tolerance and goals. Consider starting with low-cost index funds or ETFs.

Understanding Investment Growth: A Simple Calculation

One of the most powerful concepts in investing is compound interest, where your earnings themselves begin to earn returns. It’s what makes investing account growth so impactful over the long term.

Imagine you invest a certain amount of money, and it earns a return. The next year, you earn a return not just on your initial investment, but also on the earnings from the previous year. This snowball effect is how wealth truly builds over time. While complex formulas exist, you can think of it simply:

Start with your initial investment. Each year, calculate the percentage gain on your total money (initial investment plus any accumulated earnings). Add that gain to your total, and that new, larger sum becomes your starting point for the next year’s calculation.

For example, if you invest $1,000 and earn a 5% return in year one, you gain $50, making your total $1,050. In year two, you earn 5% on the new total of $1,050, yielding $52.50, bringing your total to $1,102.50. This small difference grows substantially over decades.

Monthly Payment Calculator

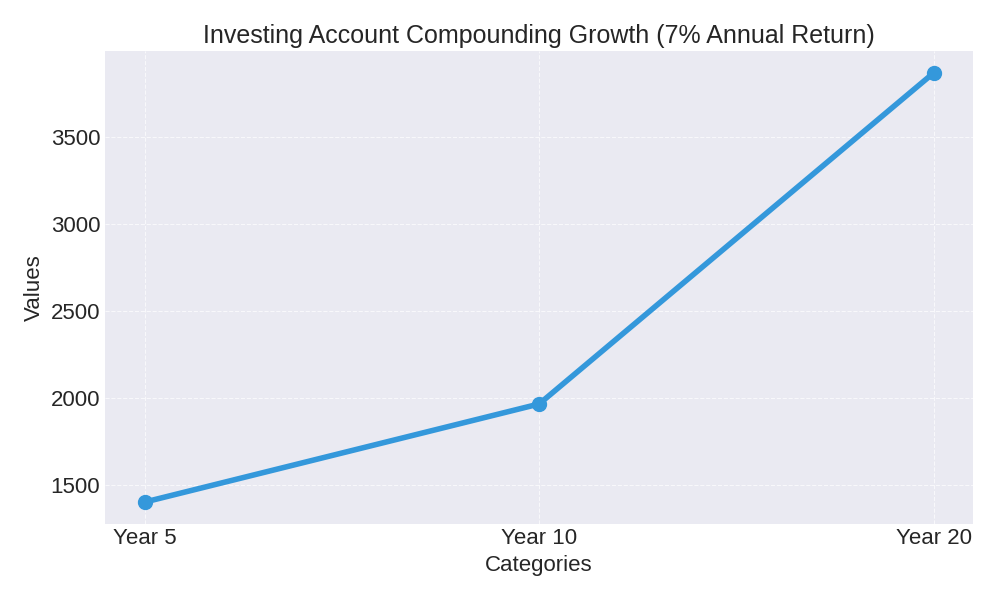

To illustrate the power of compounding with an investing account, consider the following scenario, assuming a consistent annual return of 7%:

| Investment Horizon | Value (Initial $1,000) | Value (Initial $5,000) |

|---|---|---|

| Year 5 | $1,403 | $7,013 |

| Year 10 | $1,967 | $9,836 |

| Year 20 | $3,870 | $19,350 |

Frequently Asked Questions (FAQ)

Here are answers to some common questions about investing accounts:

- How much money do I need to start an investing account?

Many online brokerages have no minimums to open an account. You can often start investing with as little as $50 or $100 through fractional shares or low-cost ETFs. - What are the risks involved in investing?

All investments carry some level of risk, meaning you could lose money. The value of investments can fluctuate due to market conditions, economic changes, and company-specific news. Diversification and a long-term perspective can help mitigate some risks. - Should I get a financial advisor?

If you’re unsure about managing your own investments, a qualified financial advisor can provide personalized guidance. They can help you set goals, determine risk tolerance, and build a suitable portfolio. Make sure to choose a fiduciary advisor who is legally obligated to act in your best interest. - How are capital gains taxed?

Capital gains are profits from selling an investment. Short-term capital gains (assets held for one year or less) are taxed at your ordinary income tax rate. Long-term capital gains (assets held for more than one year) typically qualify for lower preferential tax rates. - Can I have multiple investing accounts?

Yes, you can have multiple investing accounts, often for different purposes. For example, you might have a Roth IRA for retirement, a 529 plan for education, and a taxable brokerage account for a down payment on a house.

Conclusion

Opening an investing account is more than just a financial transaction; it’s a commitment to your future self. It empowers you to harness the formidable force of compound growth, turning modest contributions into substantial wealth over time. By understanding the different types of accounts, aligning them with your goals, and consistently contributing, you lay a solid foundation for financial independence.

Don’t let the complexity deter you. Start small, stay consistent, and continue to educate yourself. Your journey to financial freedom begins with that crucial first step. Take control of your financial destiny today.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.