Embarking on the journey of investing and retirement planning is your most direct route to financial freedom. This guide will cut through the complexity, offering clear, actionable steps to build wealth, secure your future, and achieve peace of mind. By understanding core principles and applying smart strategies, you can transform your financial outlook, no matter where you’re starting from.

The essence of effective investing and retirement planning lies in starting early, making consistent contributions, and letting the power of compound interest work for you. We’ll explore various investment vehicles, suitable retirement accounts, and practical tips to navigate market fluctuations, ensuring your money works as hard as you do.

The Foundation of Financial Freedom: Why Investing Matters

Many people think investing is just for the wealthy, but it’s a powerful tool accessible to everyone. The core principle that makes investing so effective is compound interest. This isn’t just interest on your initial savings; it’s interest on your savings PLUS all the accumulated interest from previous periods.

Why this matters in real life? Imagine you start investing $100 per month at age 25. By the time you’re 65, even with modest returns, your total contributions might be $48,000, but your investment could be worth several hundred thousand dollars. This growth far outpaces inflation, protecting your purchasing power over time. It essentially means your money starts making money for you, accelerating your wealth accumulation.

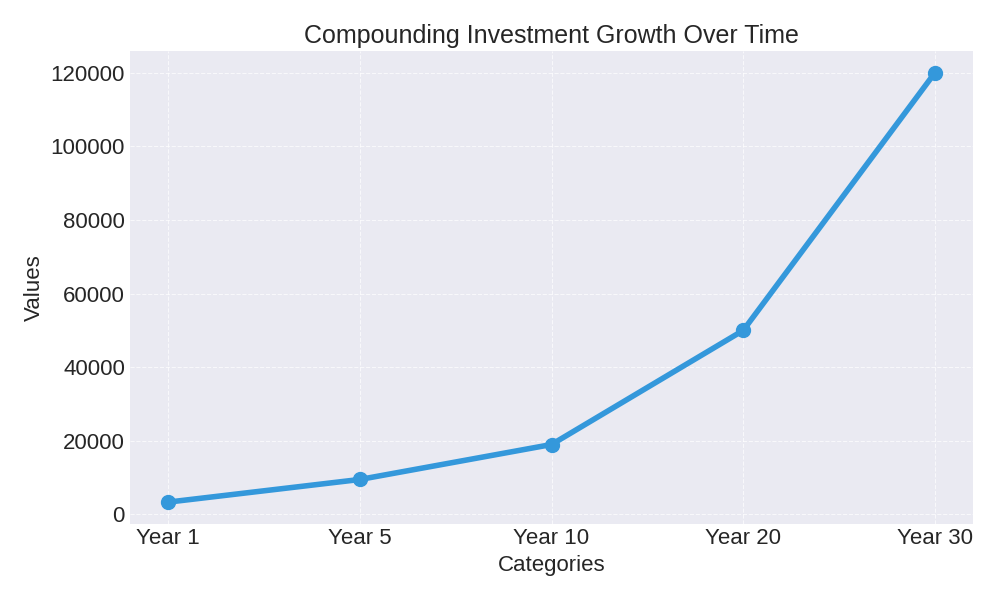

Understanding Compound Growth

Let’s consider a practical scenario. Imagine you begin with an initial investment of $2,000 and consistently add $100 each month. If your investments achieve an average annual return of 7%, the growth over time is significant, thanks to compounding. This isn’t just about how much you put in; it’s about how long your money has to grow.

Here’s a simplified look at how compounding can grow an initial investment with regular contributions over time:

| Year | Total Contributions (Approx.) | Investment Value (Approx. at 7% annual return) |

|---|---|---|

| 1 | $3,200 | $3,350 – $3,450 |

| 5 | $8,000 | $9,500 – $10,500 |

| 10 | $14,000 | $19,000 – $21,000 |

| 20 | $26,000 | $50,000 – $60,000 |

| 30 | $38,000 | $120,000 – $140,000 |

This table illustrates how the total value of your investment grows much faster than your direct contributions due to the power of compounding. Small, consistent efforts over a long period yield substantial results.

Crafting Your Plan for Investing and Retirement

A successful retirement doesn’t just happen; it’s built with intentional planning. Your first step is to define what retirement looks like for you. Will you travel, pursue hobbies, or simply enjoy a quiet life at home? This vision will help you set concrete financial goals.

Why this matters in real life? Without a clear destination, it’s hard to chart a course. Setting goals, like wanting to retire by age 60 with an income of $X per year, provides a measurable target. This allows you to work backward and determine how much you need to save and invest each month.

Key Retirement Accounts

The government offers various tax-advantaged accounts to encourage saving for retirement. Utilizing these accounts can significantly boost your savings over time.

- 401(k) and 403(b): Employer-sponsored plans often come with employer matching contributions – essentially free money! Your contributions are typically pre-tax, lowering your taxable income now. You can learn more about these plans from official sources like the U.S. Department of Labor.

- Traditional IRA: Individual Retirement Accounts (IRAs) offer tax-deductible contributions in many cases, growing tax-deferred until retirement. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are made with after-tax dollars, meaning withdrawals in retirement are completely tax-free, provided certain conditions are met. This can be very advantageous if you expect to be in a higher tax bracket later in life.

Why these matter in real life? These accounts provide significant tax benefits and allow your money to grow largely unburdened by annual taxes. For example, an employer matching your 401(k) contributions up to 5% means you are getting an immediate 100% return on that portion of your investment, which is an incredible boost to your savings.

Demystifying Investment Options

Understanding where to put your money is key. While the world of investments can seem daunting, most options fall into a few core categories, each with varying levels of risk and potential return.

The most common investment types include stocks (ownership in companies), bonds (loans to governments or corporations), and mutual funds or Exchange-Traded Funds (ETFs), which are collections of stocks and/or bonds. Each plays a different role in a diversified portfolio.

Diversification and Risk Management

Diversification is the strategy of spreading your investments across various assets to reduce risk. It’s like the old adage, “Don’t put all your eggs in one basket.” If one investment performs poorly, the others can help offset losses.

Why this matters in real life? Imagine you invested all your savings in a single company’s stock, and that company suddenly faces severe financial trouble. Your entire investment could be wiped out. However, if you diversified across 20-30 different companies, various industries, and even different asset classes (like stocks and bonds), a downturn in one area would have a much smaller impact on your overall portfolio. The U.S. Securities and Exchange Commission (SEC) provides excellent resources on understanding investment risks.

How to Calculate Your Retirement Needs

Estimating how much money you’ll need in retirement might seem like pulling a number out of thin air, but you can approach it systematically. Start by considering your current expenses and how they might change in retirement. Will you have a mortgage? Will your healthcare costs increase?

Here’s a practical way to think about it:

First, project your annual expenses in retirement. Many financial planners suggest aiming for 70-80% of your pre-retirement income to maintain your lifestyle. So, if someone earns between $60,000 and $80,000 per year, they might target $42,000-$64,000 annually in retirement.

Next, account for inflation. Prices increase over time, so $50,000 today won’t buy as much in 30 years. You need your savings to keep pace. Finally, consider how long your retirement will last. If you retire at 65 and live to 90, you’ll need funds for 25 years.

You can then use a simple process to estimate your lump sum need. Multiply your estimated annual retirement expenses by the number of years you expect to be retired. This gives you a rough total. Then, factor in a reasonable withdrawal rate (e.g., 4% per year) which helps your money last longer while still growing. This kind of calculation helps you set a clear savings target.

Your Future Value Calculator

Why this matters in real life? This calculation transforms an abstract goal into a concrete number. Knowing you need, for example, $1million, makes it a tangible goal rather than a vague aspiration. This specific figure empowers you to work backward and determine the exact amount you need to save each month or year to reach that milestone.

Setting a clear numerical target also allows for regular progress tracking. Without a defined goal, it’s difficult to assess if you’re on the right path or if adjustments are needed. It helps answer questions like: Am I saving enough? Do I need to increase my contributions? Should I re-evaluate my investment strategy?

Consider the difference between saying, “I want to save for retirement,” and “I need to save $1.2 million for retirement by age 65.” The latter provides clarity and urgency. It allows you to build a practical roadmap, factoring in your current age, expected investment returns, and contributions. This process often involves using various online calculators or consulting with a financial advisor to create a personalized plan.

Furthermore, understanding your specific financial need can motivate you to make smarter financial decisions in your everyday life, from budgeting to managing debt. Every dollar saved and invested with your retirement goal in mind brings you closer to financial independence.

Diversification: Spreading Your Bets

Diversification is a cornerstone of smart investing, often summarized by the adage, “Don’t put all your eggs in one basket.” In essence, it means spreading your investments across various assets, industries, and geographies to minimize risk. If one investment performs poorly, the impact on your overall portfolio is mitigated by the performance of others.

Key components of a diversified portfolio typically include:

- Stocks: Represent ownership in companies and offer potential for growth.

- Bonds: Loans to governments or corporations, providing income and stability.

- Cash Equivalents: Low-risk, highly liquid investments like money market funds.

- Real Estate: Can include direct property ownership or Real Estate Investment Trusts (REITs).

- Alternative Investments: Such as commodities or private equity, though these are often for more sophisticated investors.

A well-diversified portfolio aims to achieve a balance between risk and return. Different asset classes react differently to market conditions. For example, during an economic downturn, stocks might fall, but bonds might hold their value or even increase, providing a buffer.

Asset Allocation: Your Personal Risk Profile

Diversification goes hand-in-hand with asset allocation, which is the process of dividing your investment portfolio among different asset categories. Your ideal asset allocation depends heavily on your individual circumstances, including your age, financial goals, time horizon, and, most importantly, your risk tolerance.

Generally, younger investors with a longer time horizon until retirement might opt for a more aggressive portfolio with a higher percentage of stocks, as they have more time to recover from market fluctuations. Conversely, those nearing retirement often shift to a more conservative allocation with a greater emphasis on bonds and cash to preserve capital.

A common rule of thumb for determining the percentage of stocks in your portfolio is to subtract your age from 100 or 110. For instance, if you are 30 years old, you might aim for 70-80% stocks and 20-30% bonds/other assets. This is a simplified guideline, and individual situations can vary significantly. The key is to regularly review and rebalance your portfolio to ensure it aligns with your evolving financial situation and risk appetite.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.