Are you looking for a powerful, yet often overlooked, strategy to boost your financial health? Look no further than investing HSA funds. A Health Savings Account (HSA) isn’t just for current medical expenses; when properly utilized, it transforms into one of the most powerful long-term investment vehicles available, offering a rare “triple tax advantage” that savvy investors can leverage for significant wealth growth. This guide will walk you through maximizing your HSA, from understanding its benefits to practical investment steps.

Understanding the Triple Tax Advantage of HSAs

The true power of an HSA lies in its unique triple tax benefit, making it superior to many other retirement or investment accounts for those who qualify. This advantage significantly enhances your potential returns over time. Understanding each component is key to appreciating why investing HSA dollars is so impactful.

- Tax-Deductible Contributions: When you contribute money to your HSA, those contributions are tax-deductible. This means they reduce your taxable income for the year, leading to immediate tax savings. For example, if you contribute $3,000 to your HSA and are in a 22% tax bracket, you could immediately save $660 on your federal income taxes. This is like getting a guaranteed return on your money right from the start.

- Tax-Free Growth: Once your funds are in an HSA and invested, any earnings – whether from interest, dividends, or capital gains – grow tax-free. This compounding growth accelerates your wealth accumulation without being eroded by annual taxes. Imagine you invest $5,000 and it grows by 7% per year. In a taxable account, you’d pay taxes on that $350 gain, reducing future growth. In an HSA, the full $350 keeps working for you.

- Tax-Free Withdrawals for Qualified Medical Expenses: The final, and arguably most compelling, advantage is that withdrawals for qualified medical expenses are entirely tax-free. This includes a wide range of health-related costs. In retirement, when healthcare expenses often increase, this tax-free access to funds can be incredibly valuable. Even if you don’t use it for medical expenses, after age 65, you can withdraw funds for any purpose, though non-medical withdrawals will be taxed as ordinary income, similar to a traditional IRA.

In essence, you get a tax break going in, tax-free growth while it’s invested, and tax-free withdrawals for healthcare costs. This trifecta makes the HSA a highly efficient financial tool.

Eligibility and Contribution Limits for Your HSA

Before you can start investing HSA funds, you need to ensure you’re eligible and understand the annual contribution limits. Eligibility is tied to your health insurance plan, while contribution limits are set by the IRS.

- HSA Eligibility: To be eligible for an HSA, you must be covered by a High-Deductible Health Plan (HDHP). This plan must meet specific annual deductible and out-of-pocket maximum thresholds. You cannot be enrolled in Medicare, or be claimed as a dependent on someone else’s tax return.

- Contribution Limits: The IRS sets annual limits on how much you can contribute. These limits typically increase slightly each year. For example, in a recent year, an individual might contribute between $3,850 and $4,100, while a family might contribute between $7,750 and $8,300. If you are age 55 or older, you can often contribute an additional “catch-up” contribution (e.g., $1,000) beyond these limits.

Understanding these rules is critical. Maxing out your contributions each year is often the best strategy to fully leverage the HSA’s benefits. For the most current and official contribution limits, always refer to the Internal Revenue Service website.

When to Start Investing Your HSA Funds

Deciding when to start investing your HSA balance is a strategic decision, balancing immediate healthcare needs with long-term growth potential. Most experts recommend a hybrid approach.

- Build a Medical Emergency Fund First: It’s wise to keep a portion of your HSA funds in cash (or a money market account) to cover immediate, unexpected medical expenses. This “cash buffer” typically ranges from a few hundred to a few thousand dollars, depending on your deductible and comfort level. This ensures you can cover costs without tapping into your investments during a market downturn.

- Long-Term Investment Strategy: Once you have a comfortable cash buffer, you should begin investing the remainder of your HSA balance. The longer your money is invested, the more it benefits from tax-free compounding. Imagine two individuals, both 30. John keeps his entire HSA balance in cash, earning negligible interest. Sarah keeps $2,000 in cash and invests the rest. If both contribute $3,000 annually and Sarah’s investments average 6% growth, after 20 years, Sarah’s invested portion could be significantly higher than John’s cash balance, even after accounting for some minor medical withdrawals.

Think of your HSA as a dual-purpose account: an immediate fund for healthcare costs and a powerful, long-term retirement investment vehicle, especially after age 65.

Choosing the Right HSA Provider for Investing

Not all HSA providers are created equal when it comes to investing. Choosing the right one can significantly impact your investment performance and overall experience.

- Fees: Be mindful of administrative fees, investment fees, and expense ratios. Some providers charge monthly maintenance fees, while others offer commission-free trading. High fees can erode your returns, so always compare.

- Investment Options: Look for a provider that offers a wide range of investment options, such as low-cost index funds, ETFs (Exchange Traded Funds), and mutual funds. Having diverse choices allows you to build a portfolio that aligns with your risk tolerance and financial goals.

- Ease of Use: A user-friendly platform with intuitive navigation and helpful resources can make managing your HSA investments much simpler. Check for mobile app availability, clear statements, and responsive customer service.

Carefully evaluating these factors will help you select an HSA provider that supports your investing journey effectively.

Step-by-Step Guide to Investing HSA Funds

Ready to start? Here’s a practical guide to get your HSA funds invested and working for you.

- Confirm Eligibility and Open Your HSA: Ensure you are enrolled in an HDHP and meet all IRS eligibility criteria. If your employer offers an HSA, that’s usually the easiest route. Otherwise, you can open one with a private provider.

- Fund Your HSA: Contribute money through payroll deductions (which often have an added FICA tax benefit) or direct transfers from your bank account. Aim to contribute regularly to maximize compounding.

- Meet Cash Threshold (if applicable): Many HSA providers require you to have a minimum cash balance (e.g., $1,000 or $2,000) before you can move funds into investment options. Once this threshold is met, you can transfer excess funds.

- Select Investment Options: Log into your HSA account’s investment portal. Choose investments that align with your risk tolerance and long-term goals. For most long-term investors, diversified, low-cost index funds or target-date funds are excellent choices.

- Monitor and Rebalance: Periodically review your investment performance and adjust your portfolio as needed. Rebalancing ensures your asset allocation stays in line with your strategy. For instance, if stocks have done particularly well, you might trim some to maintain your desired equity percentage.

By following these steps, you can effectively transition your HSA from a simple savings account to a powerful investment vehicle.

How to Calculate Potential HSA Growth

Understanding how your HSA funds can grow is crucial for appreciating its long-term power. While exact figures depend on market performance, we can illustrate the potential through compound interest.

Imagine your investment growing over time, not just on your initial contributions, but on all the accumulated earnings from previous years too. This “money making money” effect is called compound interest.

Here’s how to think about it in plain language:

Start with your initial investment. Add your yearly contributions. Then, estimate a reasonable annual return (like 5% to 7%). This return is applied to your entire balance at the end of the year, including any gains from prior years. The next year, the same return is applied to this new, larger balance, leading to even bigger dollar gains. This snowball effect is what makes long-term investing so powerful, especially with an HSA’s tax advantages.

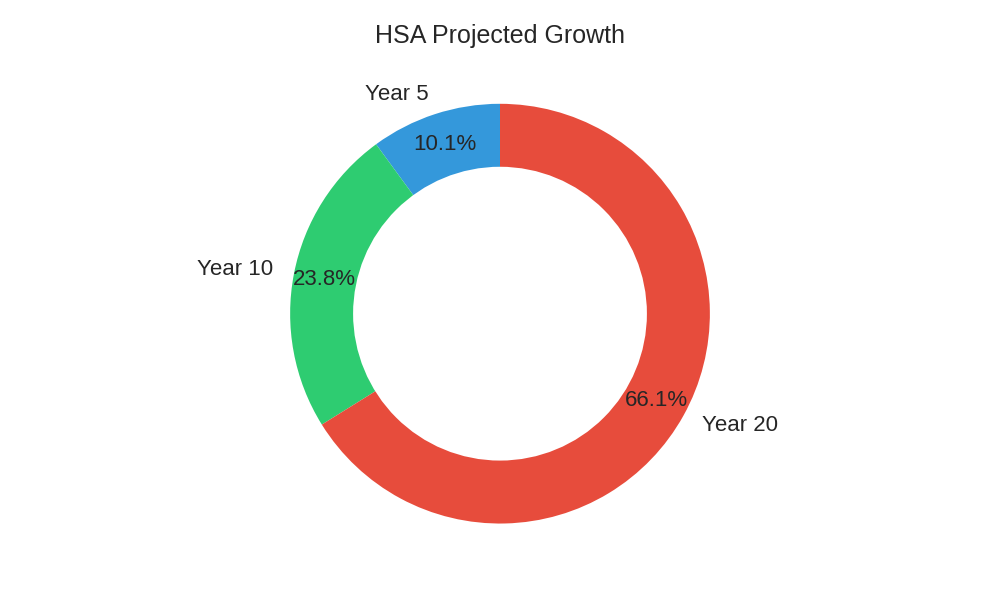

HSA Triple Tax Advantage Growth Calculator

To demonstrate this, consider a hypothetical “Compound Growth Scenario” where someone consistently invests in their HSA.

| Scenario Detail | Initial Balance (Year 0) | Annual Contributions (Estimated Range) | Estimated Annual Return |

|---|---|---|---|

| Example Investor | $1,000 | $3,000 – $4,000 | 6% |

| Time Horizon | Projected Invested Value (Approx.) |

|---|---|

| Year 5 | $19,000 – $22,000 |

| Year 10 | $45,000 – $52,000 |

| Year 20 | $125,000 – $145,000 |

These projections are illustrative and highlight the power of sustained contributions and compound growth. Actual returns will vary based on market conditions, investment choices, and specific contribution amounts. To learn more about general investment principles and market dynamics, resources like Bloomberg can provide valuable insights.

Strategic HSA Withdrawal Considerations

Maximizing your HSA isn’t just about investing; it’s also about smart withdrawal strategies to maintain its tax-free status. The key is understanding what constitutes a “qualified medical expense.”

- What Qualifies: The IRS defines qualified medical expenses broadly. This includes deductibles, co-pays, prescriptions, dental care, vision care, and even certain long-term care insurance premiums. For a comprehensive list, consult IRS Publication 502.

- Keeping Meticulous Records: To ensure your withdrawals remain tax-free, it is crucial to keep detailed records of all your medical expenses and corresponding payments. This includes receipts, Explanation of Benefits (EOB) statements, and any other documentation.

- The “Retroactive Reimbursement” Strategy: A powerful technique is to pay for qualified medical expenses out-of-pocket, keep the receipts, and then reimburse yourself from your HSA years or even decades later. Your HSA funds can continue to grow tax-free, and you can withdraw a tax-free lump sum later using those old receipts. This effectively allows your HSA to function like a super-charged retirement account while still being available for medical needs.

By carefully tracking your medical expenses and strategically timing your reimbursements, you can greatly extend the tax-free growth period of your HSA investments.

Frequently Asked Questions (FAQ) about Investing HSAs

Here are answers to some common questions about investing your Health Savings Account.

- Can I lose money investing my HSA?

Yes, any investment carries risk, and the value of your HSA investments can fluctuate with market conditions. It’s important to choose investments that match your risk tolerance and time horizon.

- What if I don’t use it for medical expenses?

After age 65, you can withdraw funds from your HSA for any purpose without penalty. These withdrawals will be taxed as ordinary income, similar to a traditional IRA. Before age 65, non-qualified withdrawals are subject to your ordinary income tax rate plus a 20% penalty.

- Can I contribute to an HSA and an FSA?

Generally, no. You cannot contribute to both a general Health Savings Account (HSA) and a general Flexible Spending Account (FSA) in the same year. However, you might be eligible for a “Limited Purpose FSA” (for dental and vision only) alongside an HSA.

- Is an HSA better than a 401(k) or IRA?

An HSA offers unique advantages due to its triple tax benefits, especially if you anticipate significant medical expenses in retirement. Many financial experts recommend prioritizing contributions to an HSA after maximizing employer-matched 401(k) contributions. It often complements, rather than replaces, other retirement accounts.

Conclusion

Investing your HSA funds is a strategic financial move that can significantly enhance your long-term wealth and secure your healthcare future. By understanding the triple tax advantage, adhering to eligibility and contribution rules, and making informed investment choices, you can transform your Health Savings Account into a powerful asset. It’s a journey that combines smart healthcare planning with robust investment growth.

Take Action Now!

Don’t let the power of your HSA sit idle in a cash account. Explore your HSA provider’s investment options today. If you need personalized guidance on tailoring an investment strategy, consider consulting a qualified financial advisor. Start investing HSA funds and unlock its full potential for your financial future.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.