Embarking on the journey of investing long term is not just about growing your wealth; it’s about building a foundation for true financial freedom. This comprehensive guide will demystify the process, transforming complex concepts into actionable strategies for anyone serious about securing their future. We’ll explore why investing long term outperforms short-term speculation, leveraging the incredible power of time and consistent effort. Understanding these principles is crucial for sustainable wealth creation. For those looking to confidently navigate the markets, committing to investing long term is arguably the most powerful decision you can make.

The core principle is simple: regularly invest money into assets that have historically appreciated over many years, allowing your gains to generate further gains. This approach minimizes the impact of short-term market fluctuations and maximizes the potential for substantial wealth accumulation. By staying invested for decades, you harness market resilience and the incredible power of compounding.

Understanding Long-Term Investing: A Foundation for Growth

Long-term investing means committing your capital for an extended period, typically five years or more. This strategy contrasts sharply with short-term trading, which focuses on quick profits from rapid price movements. The primary goal of long-term investing is to grow wealth steadily and significantly over time, often for major life goals like retirement or a child’s education.

Why Time is Your Most Valuable Asset

In the world of investments, time is not just money; it’s leverage. The longer your money is invested, the more opportunities it has to grow, compound, and recover from any temporary market downturns. This matters in real life because market volatility is a given. Short-term investors can be rattled by a sudden dip, but long-term investors understand that historically, markets recover and reach new highs over decades. Imagine you bought a diversified stock fund just before a market crash. While your portfolio might drop initially, history shows that after 10-20 years, it would likely have recovered and grown significantly beyond its initial value.

The Power of Compounding: Your Money’s Best Friend

Compounding is the phenomenon where the earnings from your investments generate their own earnings. It’s often called “interest on interest” and is arguably the most powerful force in finance. Albert Einstein reportedly called it the eighth wonder of the world.

How Compounding Works in Real Life

Let’s consider a simple scenario. Imagine you invest $10,000 in a diversified portfolio that earns an average annual return of 7%. After one year, you’d have $10,700. The next year, you earn 7% not just on your initial $10,000, but on the full $10,700. This snowball effect accelerates over time. This matters because even small, consistent contributions can lead to substantial wealth. Starting early is key because it gives compounding more time to work its magic.

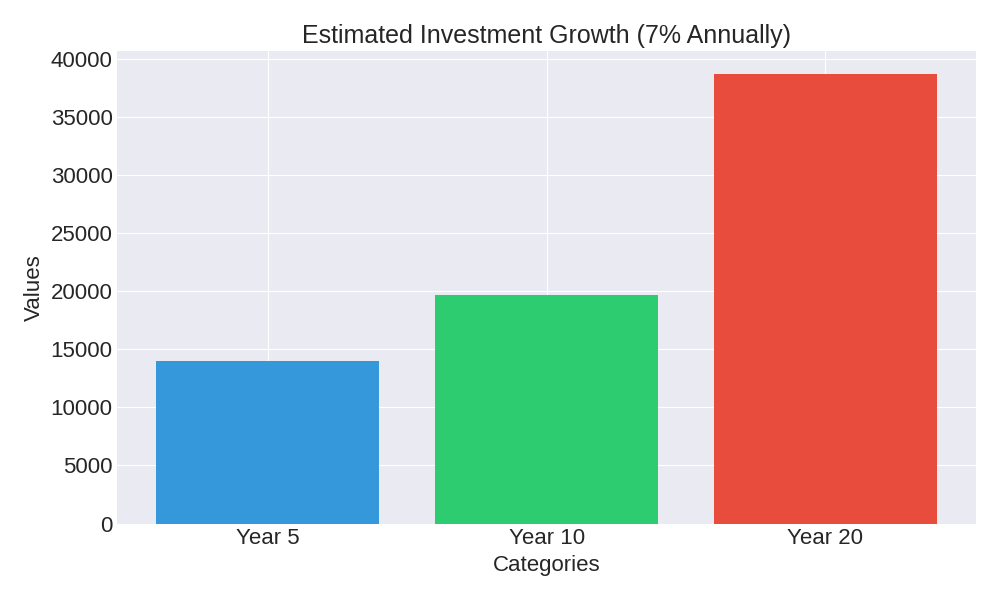

| Investment Period | Initial Investment | Estimated Value (7% Annual Growth) |

|---|---|---|

| Year 5 | $10,000 | $14,025 |

| Year 10 | $10,000 | $19,671 |

| Year 20 | $10,000 | $38,697 |

Key Principles for Successful Long-Term Investing

To truly secure your financial future, adhere to these fundamental principles. They act as your roadmap through the complexities of the market.

-

Start Early and Invest Consistently: The earlier you begin, the more time compounding has to work. Regular contributions, even small ones, add up significantly. This consistency helps you ride out market highs and lows.

-

Diversification: Do not put all your eggs in one basket. Spreading your investments across different asset classes (stocks, bonds, real estate) and within those classes (various industries, geographies) reduces risk. If one investment performs poorly, others may perform well, balancing your overall portfolio.

-

Understand Your Risk Tolerance: This refers to your comfort level with potential losses. A higher risk tolerance might mean more stock exposure, while a lower tolerance might lean towards bonds. Knowing this helps you choose investments you can stick with, even during downturns. The U.S. Securities and Exchange Commission (SEC.gov) offers valuable resources on understanding investment risks.

-

Minimize Fees and Taxes: High fees can significantly erode your returns over decades. Choose low-cost index funds or ETFs where possible. Similarly, be aware of tax implications and utilize tax-advantaged accounts like 401(k)s and IRAs to maximize your growth.

Choosing the Right Investment Vehicles

For those interested in investing long term, several common options exist. Each has different characteristics regarding risk and potential return.

1. Stocks (Equities): These represent ownership in a company. They offer high growth potential but also come with higher volatility. Owning a diverse portfolio of stocks reduces the risk associated with any single company.

2. Bonds: When you buy a bond, you’re essentially lending money to a government or corporation. Bonds generally offer lower returns than stocks but are less volatile, providing stability to a portfolio. The U.S. Treasury (Treasury.gov) issues various types of bonds.

3. Mutual Funds and Exchange-Traded Funds (ETFs): These are professionally managed collections of stocks, bonds, or other assets. They offer instant diversification and are a popular choice for long-term investors. Index funds, a type of mutual fund or ETF, simply track a market index like the S&P 500, offering broad market exposure at low cost.

4. Real Estate: This can be direct ownership of property or through Real Estate Investment Trusts (REITs). Real estate can provide income and appreciation, but direct ownership often requires significant capital and management.

Building Your Long-Term Investment Strategy

Developing a clear strategy is vital. It acts as your guide, preventing impulsive decisions.

Step-by-Step Approach:

Define Your Goals: Are you saving for retirement, a down payment, or college tuition? Specific goals help determine your timeline and how much risk you can take.

Assess Your Risk Tolerance: Honestly evaluate how much market fluctuation you can stomach without losing sleep. This will influence your asset allocation.

Determine Your Asset Allocation: This is the mix of different asset classes in your portfolio (e.g., 70% stocks, 30% bonds). Your age, goals, and risk tolerance will guide this decision. Younger investors with longer time horizons often opt for a higher percentage of stocks.

Choose Your Investment Accounts: Select appropriate accounts like 401(k)s, IRAs (Traditional or Roth), or taxable brokerage accounts. Each has unique tax advantages and withdrawal rules.

Select Specific Investments: Based on your asset allocation, choose specific funds or individual securities. For most beginners, diversified, low-cost index funds or ETFs are an excellent starting point.

Automate Your Investments: Set up automatic transfers from your bank account to your investment accounts. This ensures consistency and makes investing a habit. This practice is known as Dollar-Cost Averaging, reducing the impact of volatility by investing a fixed amount regularly.

Periodically Rebalance Your Portfolio: Over time, your asset allocation might drift. Rebalancing means adjusting your holdings back to your target percentages. For example, if stocks have done very well, you might sell some to buy more bonds, maintaining your desired risk level. Learn more about managing your money with resources from the Consumer Financial Protection Bureau (CFPB.gov).

Calculating Your Potential Growth

Understanding how your money might grow over time is empowering. While exact future returns are impossible to predict, you can estimate potential growth using simple calculations. You don’t need complex math formulas; just grasp the concept of growth over time.

To estimate, think about how much you invest initially, how much you add regularly, and a reasonable average annual growth rate. For example, if you start with $5,000 and add $200 each month, assuming a modest 6% average annual return, you can project your balance. Tools often simulate this, showing how your money compounds over 10, 20, or even 30 years. This simple projection helps visualize the benefits of consistent contributions and the power of time.

LONG-TERM INVESTMENT GROWTH CALCULATOR

Understanding and Managing Risk

All investments carry some level of risk. The key to successful long-term investing is to understand and manage these risks, not avoid them entirely. Major risks include market risk (the chance that the overall market declines), inflation risk (the erosion of purchasing power over time), and interest rate risk (affecting bond values).

Diversification is your primary defense against market risk. For inflation, investing in growth assets like stocks is crucial, as cash loses value over time. Regularly reviewing your portfolio and adjusting your strategy as you age helps manage your risk exposure effectively.

FAQ: Your Investing Questions Answered

Q1: Is it too late to start investing long term?

A1: It’s never too late to start. While starting early offers the greatest advantage, any time you begin investing is better than not starting at all. The principles of compounding and consistent contributions still apply, regardless of your age.

Q2: How much money do I need to start investing?

A2: You can start with very little. Many online brokers allow you to open accounts with no minimum balance. With fractional shares and low-cost ETFs, you can begin investing with as little as $5 to $50. The consistency of your contributions is more important than the initial amount.

Q3: Should I invest in individual stocks or funds?

A3: For most long-term investors, especially beginners, diversified index funds or ETFs are generally recommended. They offer broad market exposure and diversification with lower risk than picking individual stocks. Individual stocks require significant research and carry higher specific company risk.

Q4: How often should I check my investment performance?

A4: For long-term investors, over-checking your portfolio can lead to emotional decisions based on short-term market fluctuations. Reviewing your portfolio quarterly or annually is usually sufficient to ensure it aligns with your goals and to rebalance if necessary.

Conclusion: Your Path to Financial Freedom

Investing long term is a proven path to securing your financial future. By understanding the power of compounding, adhering to sound principles like diversification, and maintaining a consistent, disciplined approach, you can build substantial wealth over time. Remember, it’s not about timing the market, but about time in the market. Start today, stay patient, and watch your financial freedom grow.

Ready to Begin Your Investment Journey?

Take the first step towards a more secure financial future. Open an investment account, set up automatic contributions, and commit to the principles of long-term growth. Your future self will thank you.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.