That gut-wrenching feeling when your beloved pet is sick or injured is something no pet parent ever wants to experience. Beyond the emotional toll, the financial shock of an unexpected vet bill can be devastating. You’re left balancing your pet’s well-being against a potentially staggering cost, and often, that means making impossible choices. This is precisely where the question of whether insurance for animals is truly worth it to save on vet bills comes into sharp focus.

As a financial strategist and consumer advocate, I see too many individuals caught unprepared. You love your furry, feathered, or scaled family members unconditionally, but that love doesn’t come with a blank check. Deciding on insurance for animals isn’t just about crunching numbers; it’s about peace of mind and the ability to say “yes” to the best possible care without crippling your finances. Let’s cut through the noise and figure out if this investment makes sense for you.

The Real Cost of Pet Ownership: Beyond Food and Toys

Many pet owners underestimate the true financial commitment of animal companionship. It’s not just about the upfront cost, food, and toys. We’re talking about vaccinations, routine check-ups, dental care, and, most critically, unforeseen emergencies or chronic conditions. Imagine your energetic retriever suddenly limps home, leading to X-rays, diagnostics, and potentially surgery for a torn ACL. Or consider your beloved cat developing diabetes in their senior years, requiring lifelong medication and regular vet visits.

Why this matters in real life: These scenarios aren’t rare; they’re common realities. A single emergency can easily range from $800 to $5,000 or more, depending on the severity and required treatment. Chronic conditions, like arthritis or allergies, can rack up hundreds of dollars in medication and appointments every month. Without a financial safety net, these costs can quickly spiral out of control, forcing heartbreaking decisions that no one should have to make. Pet insurance aims to buffer these shocks, giving you the freedom to prioritize your pet’s health.

Common Myths to Avoid When Considering Insurance for Animals

Before diving into the benefits, let’s debunk some pervasive myths that can cloud your judgment:

- Myth 1: “My pet is young and healthy, so I don’t need it.” This is perhaps the most dangerous assumption. Accidents happen to young, healthy pets too – swallowed objects, broken bones, sudden illnesses. Moreover, conditions like hip dysplasia or certain cancers can manifest early. Waiting until your pet is older or sick means any existing condition will likely be considered “pre-existing” and excluded from coverage.

- Myth 2: “It’s just too expensive and never pays off.” While premiums are an ongoing cost, the value isn’t just in direct reimbursement. It’s in the financial security it provides. For example, if your dog needs emergency surgery costing $4,000, and your policy covers 80% after a $500 deductible, you’d save $2,700 out of pocket. That’s a significant return on a few hundred dollars in annual premiums.

- Myth 3: “All policies are basically the same.” Absolutely not. Policies vary wildly in terms of coverage (accident-only vs. comprehensive), reimbursement percentages (50% to 100%), deductibles (per incident vs. annual), and crucial exclusions. You need to read the fine print carefully to understand what you’re truly getting.

The “How to Calculate” Section: Is Pet Insurance Right for Your Wallet?

Deciding if insurance for animals is a smart financial move for you boils down to a personal risk assessment and a simple calculation. You need to weigh the consistent, predictable cost of premiums against the unpredictable, potentially massive cost of uncovered vet bills. Here’s how to think about it:

Step 1: Estimate Your Annual Premium Cost.

Look at quotes for different plans based on your pet’s breed, age, and location. This might be, for example, between $300 and $700 per year for a dog, or $200 to $400 for a cat. This is your known outgoing expense.

Step 2: Understand Your Deductible.

Most policies have a deductible you pay before coverage kicks in. It could be $100, $250, $500, or even $1,000. Decide if this is a per-incident deductible (you pay it each time for a new issue) or an annual deductible (you pay it once per year, no matter how many incidents).

Step 3: Know Your Reimbursement Rate.

This is the percentage of eligible vet bills the insurance company will pay after your deductible is met. Common rates are 70%, 80%, or 90%. A higher reimbursement rate means higher premiums but less out-of-pocket later.

Step 4: Factor in Potential Vet Costs.

This is the hardest part because it’s unpredictable. Consider your pet’s breed (some are prone to specific health issues), age, and lifestyle. Do they chew everything? Are they adventurous? A general range for a single major emergency or illness could be anywhere from $1,000 to $6,000. For chronic conditions, it could be thousands annually.

Simplified Calculation Example:

Imagine your annual premium is $480 ($40/month). Your deductible is $250 annually, and your reimbursement rate is 80%. If your pet has an accident costing $3,000:

- Total vet bill: $3,000

- You pay deductible: $250

- Remaining bill eligible for reimbursement: $3,000 – $250 = $2,750

- Insurance covers 80% of eligible bill: 0.80 * $2,750 = $2,200

- Your out-of-pocket for this incident (after insurance) = $3,000 – $2,200 = $800

- Total cost to you for the year (premium + out-of-pocket) = $480 + $800 = $1,280

Without insurance, that $3,000 bill would be entirely out of your pocket. In this scenario, insurance saved you $3,000 – $800 = $2,200 on that one incident, far outweighing the $480 premium.

Pro Tip: Build an Emergency Fund First.

Before pet insurance, ensure you have a general emergency fund for at least 3-6 months of living expenses. Then, consider a dedicated “pet emergency fund” of $500-$2,000 to cover deductibles and smaller, routine costs. Insurance isn’t for every small cut, but for those major, budget-busting events.

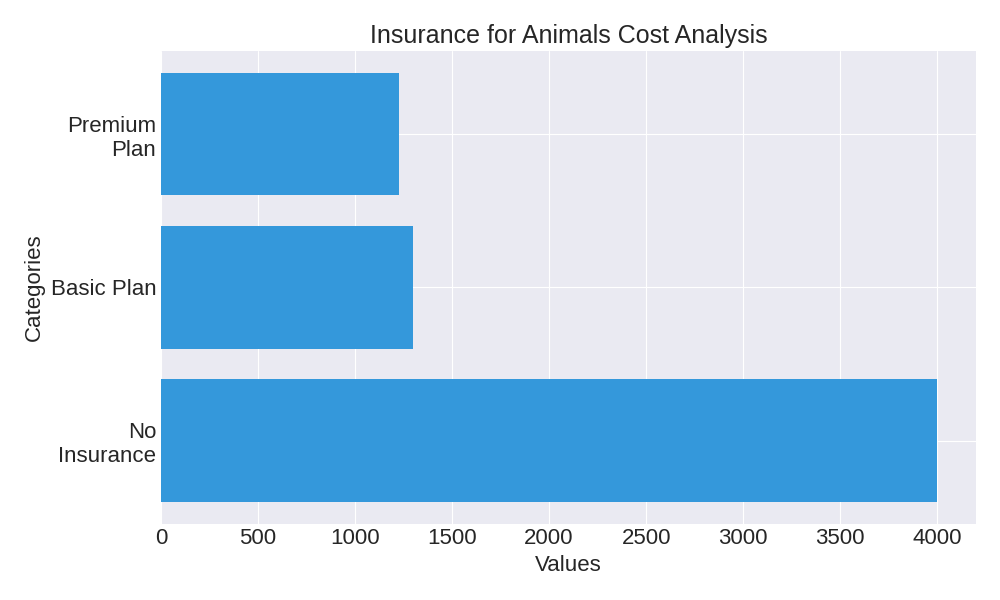

Pet Insurance Annual Cost Comparison

When assessing pet insurance, it’s not just about the immediate savings on a single bill, but the overall financial resilience it provides. You’re trading a smaller, predictable monthly cost for protection against large, unpredictable expenses. This matters because it removes the emotional burden of financial constraint during a crisis, allowing you to focus purely on your pet’s recovery.

Choosing the Right Policy: Insider Tips & What to Look For

Not all pet insurance is created equal. Being a savvy consumer means knowing what questions to ask and what details to scrutinize. Here’s an insider’s guide:

- Start Early: The younger and healthier your pet, the cheaper your premiums will be, and the fewer pre-existing conditions will be on their record. This is perhaps the most critical factor.

- Understand Pre-Existing Conditions: This is the biggest catch. Most policies won’t cover conditions diagnosed before your coverage starts or during a waiting period. Some plans may offer limited coverage for “curable” pre-existing conditions after a waiting period, but it’s rare. Always clarify this.

- Accident-Only vs. Comprehensive: Accident-only plans are cheaper but cover very little. Comprehensive plans cover accidents, illnesses, surgeries, medication, and often include wellness add-ons (for routine care). For true peace of mind, a comprehensive plan is usually the way to go, especially for dogs, which are more prone to varied health issues than cats.

- Annual vs. Per-Incident Deductible: An annual deductible means you pay it once a year. A per-incident deductible means you pay it each time your pet gets sick or injured for a different condition. Annual deductibles are generally more consumer-friendly if your pet has multiple issues in one year.

- Reimbursement Payout Limits: Check if there’s an annual limit on how much the policy will pay out. Some plans have unlimited payouts, while others cap it at a specific amount (e.g., $10,000 or $20,000 per year). For serious chronic conditions or multiple emergencies, higher limits are essential.

- Wellness Plans: These are usually separate add-ons for routine care like vaccinations, check-ups, and flea/tick prevention. They often operate like a savings plan where you pay in, and it covers predictable costs. Compare the cost of the wellness plan to what you’d typically spend out-of-pocket; sometimes, it’s not cost-effective.

- Check Reviews and Financial Stability: Look for providers with a strong reputation and stable financial backing. Websites like Consumer Reports or financial review sites can offer unbiased perspectives on different providers. You want a company that will be there when you need them.

| Scenario | Annual Premium (Example) | Major Incident Cost (Example) | Deductible (Example) | Reimbursement Rate (Example) | Net Out-of-Pocket for Incident | Total Yearly Cost to You |

|---|---|---|---|---|---|---|

| No Insurance | $0 | $4,000 (Surgery) | N/A | N/A | $4,000 | $4,000 |

| Basic Plan (80% / $500 Deductible) | $600 | $4,000 (Surgery) | $500 | 80% | $700 | $1,300 ($600+$700) |

| Premium Plan (90% / $250 Deductible) | $850 | $4,000 (Surgery) | $250 | 90% | $375 | $1,225 ($850+$375) |

| Multiple Incidents (2 x $2,000) – Basic Plan | $600 | $4,000 Total | $500 (Annual) | 80% | $700 | $1,300 ($600+$700) |

As you can see from the table, even with a basic plan, the savings in a major incident can be substantial. For pets with ongoing health issues, this protection becomes even more invaluable. Consider visiting resources like the American Veterinary Medical Association (AVMA) for insights into pet health costs and care standards, which can help you anticipate potential expenses.

The Final Verdict: A Strategic Investment for Peace of Mind

So, is insurance for animals worth it to save on vet bills? My authoritative answer as a financial strategist is this: for most pet owners, yes, it absolutely is a worthwhile and strategic investment. It’s not about guaranteed financial profit, but about risk management. You’re insuring against the unpredictability of significant veterinary expenses, which can be far more financially impactful than a human health deductible.

Think of it like car insurance. You pay for it every month, hoping you never need it. But if you do, that coverage saves you from potentially ruinous costs. Pet insurance provides the same crucial safety net. It allows you to prioritize your pet’s health and happiness without being paralyzed by financial anxiety.

Before committing, always compare multiple quotes. Look at companies like Healthy Paws, Embrace, Figo, or Nationwide. Read policy documents thoroughly, paying special attention to exclusions, waiting periods, and deductible structures. An excellent resource for comparing plans and understanding the nuanced financial implications can be found on sites like Forbes Advisor or similar financial news outlets that review pet insurance options.

Conclusion: Empowering Your Pet’s Future

Ultimately, the decision to invest in insurance for animals is a personal one, but it’s a decision rooted in financial prudence and deep care for your companion. By understanding the true costs, avoiding common myths, and strategically selecting a policy, you empower yourself to provide the best possible care for your pet, no matter what unexpected challenges life throws your way.

Call to Action: Don’t wait for an emergency. Start exploring pet insurance options today. Get a few quotes, compare plans, and secure your pet’s health and your financial peace of mind. Your future self – and your beloved pet – will thank you.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.