Embarking on the journey to homeownership is an exciting milestone, often accompanied by the significant decision of securing a home loan. Finding the right lender for home loan needs is paramount, as the chosen lender and the rate they offer can impact your financial health for decades. This comprehensive guide will equip you with the knowledge and strategies to navigate the complex world of mortgage lending, ensuring you unlock the best possible rate and terms for your dream home. We’ll start from the basics and move through advanced tips, demystifying the process step-by-step.

Understanding the Basics of a Home Loan

Before diving into lender specifics, it’s crucial to grasp the fundamental components of a home loan. A mortgage is essentially a loan taken out to purchase a property, using the property itself as collateral. Your monthly payments typically comprise principal and interest, and sometimes property taxes and homeowner’s insurance (escrow).

Key Terms to Know

- Principal: The actual amount of money you borrow.

- Interest Rate: The cost of borrowing the principal, expressed as a percentage. This is a crucial factor in your monthly payment.

- Annual Percentage Rate (APR): The total cost of the loan, including the interest rate plus other fees like points, broker fees, and other charges. It provides a more complete picture of your loan’s cost.

- Loan Term: The duration over which you agree to repay the loan, commonly 15 or 30 years.

- Down Payment: The upfront cash amount you pay towards the home’s purchase price. A larger down payment can often lead to better rates.

- Closing Costs: Various fees incurred during the buying and selling of a home, typically 2-5% of the loan amount.

Types of Mortgage Lenders

The landscape of mortgage providers is diverse, each with distinct advantages. Understanding the different types of lenders can help you target the best fit for your specific financial situation.

- Banks: Traditional retail banks offer a full range of financial services, including mortgages. They often have competitive rates for existing customers and can be a convenient option.

- Credit Unions: Member-owned financial cooperatives that often offer lower interest rates and fees due to their non-profit status. Membership is usually required.

- Mortgage Lenders/Brokers: Dedicated mortgage companies that specialize solely in home loans. Mortgage lenders underwrite and fund their own loans, while mortgage brokers act as intermediaries, connecting borrowers with various lenders and their products. Brokers can be excellent for comparing multiple offers.

- Online Lenders: Digital-first platforms that streamline the application process, often with competitive rates and lower overheads. They are known for speed and convenience but may offer less personalized service.

Factors Influencing Your Home Loan Rate

Several critical factors determine the interest rate you’ll be offered by a lender for home loan. Understanding these allows you to optimize your financial profile before applying.

- Credit Score: Your credit score is one of the most significant determinants. Lenders use it to assess your creditworthiness. A higher score (generally above 740) signals lower risk and typically qualifies you for the best rates.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 36%) indicates you can comfortably manage additional debt.

- Loan-to-Value (LTV) Ratio: Calculated by dividing the loan amount by the home’s appraised value. A lower LTV (meaning a larger down payment) suggests less risk for the lender and can secure better terms.

- Loan Term and Type: Shorter loan terms (e.g., 15 years) typically have lower interest rates than longer terms (e.g., 30 years). Fixed-rate mortgages offer stable payments, while adjustable-rate mortgages (ARMs) can start with lower rates but fluctuate over time.

- Market Conditions: Broader economic factors, such as inflation, Federal Reserve policies, and bond market performance, significantly influence prevailing mortgage rates. You can monitor these trends by visiting reputable financial news outlets like Bloomberg.com.

- Property Type and Location: Some property types (e.g., condos, multi-family homes) or locations might carry different risk profiles, affecting rates.

Step-by-Step: Unlocking Your Best Rate

Follow these steps to systematically find and secure the most favorable home loan rate.

Step 1: Optimize Your Financial Profile

- Boost Your Credit Score: Pay bills on time, reduce credit card balances, and avoid opening new lines of credit before applying.

- Lower Your DTI: Pay down existing debts, especially high-interest ones, to improve your ratio.

- Save for a Larger Down Payment: Aim for at least 20% to avoid private mortgage insurance (PMI) and potentially secure a better rate.

- Gather Documentation: Prepare essential documents like pay stubs, tax returns, bank statements, and investment account summaries.

Step 2: Research and Compare Lenders

- Shop Around: Do not settle for the first offer. Contact at least 3-5 different types of lenders (banks, credit unions, mortgage brokers, online lenders).

- Utilize Online Tools: Many websites, like Bankrate.com, allow you to compare rates and terms from various lenders.

- Check Reviews: Look for lender reviews and customer satisfaction ratings to gauge their service quality.

Step 3: Get Pre-Approved, Not Just Pre-Qualified

A pre-qualification is an estimate of how much you might be able to borrow. A pre-approval is a more thorough process where the lender verifies your financial information and commits to lending you a specific amount, subject to property appraisal. Pre-approval strengthens your offer to sellers and gives you a clear budget.

Step 4: Understand and Compare Loan Estimates

Once you apply, lenders must provide a Loan Estimate within three business days. This standardized form details the loan amount, interest rate, monthly payment, and estimated closing costs.

- Focus on the APR: This gives you the true cost of the loan, including fees.

- Compare Fees: Look closely at origination fees, appraisal fees, and other charges. Some fees are negotiable.

- Ask Questions: Don’t hesitate to ask your potential lender for home loan about anything you don’t understand.

Step 5: Lock In Your Rate

Mortgage rates fluctuate daily. Once you’re ready to proceed with a specific lender, you can “lock in” your rate for a set period (e.g., 30, 45, or 60 days). This protects you if rates rise during your home buying process.

How to Calculate Your Potential Payments

Understanding how your loan amount, interest rate, and term translate into monthly payments is vital. While the underlying formulas are complex, here’s a simplified breakdown and an example.

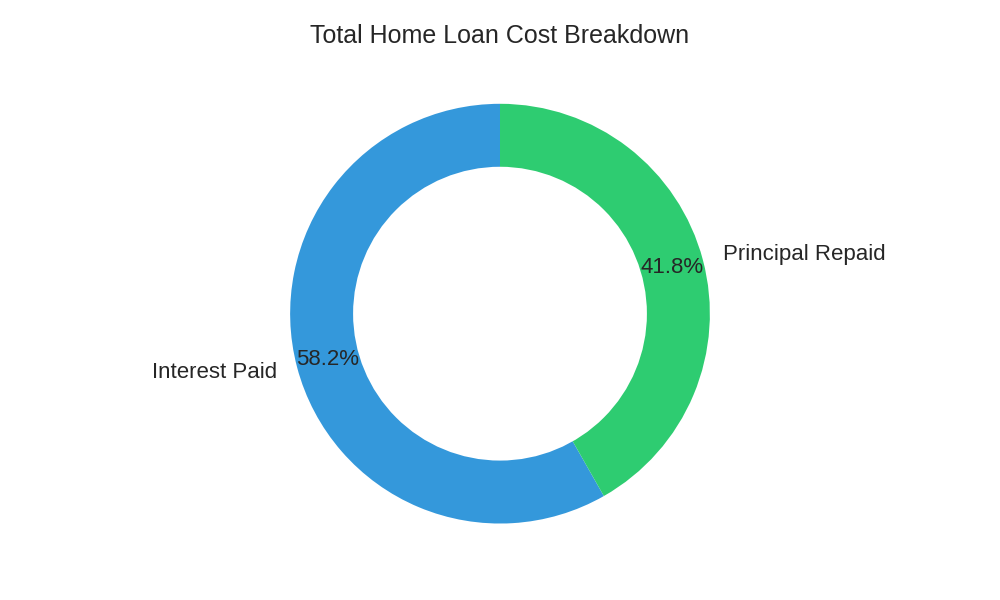

If you borrow a principal amount at a certain interest rate over a set number of years, your monthly payment covers both a portion of the principal and the interest accrued. Early payments are heavily weighted towards interest, while later payments pay down more principal. Over the life of a typical 30-year loan, you will often pay significantly more in interest than the original principal amount.

Consider a typical loan scenario to illustrate the financial impact:

| Loan Detail | Value |

|---|---|

| Loan Amount | $300,000 |

| Interest Rate | 7.0% |

| Loan Term | 30 Years (360 Months) |

| Monthly Payment | $1,995.56 |

| Total Interest Paid | $418,401.60 |

| Total Cost of Loan | $718,401.60 |

Monthly Payment Calculator

As you can see from the example, a slightly higher interest rate can dramatically increase your total interest payments over the loan’s lifetime. This highlights the importance of securing the best possible rate. For more detailed information on mortgage terms and calculations, the Consumer Financial Protection Bureau is an excellent resource.

FAQ: Common Questions About Home Loans

Q1: What is the difference between a fixed-rate and an adjustable-rate mortgage (ARM)?

A fixed-rate mortgage has an interest rate that remains constant for the entire loan term, providing predictable monthly payments. An adjustable-rate mortgage (ARM) typically starts with a lower, fixed interest rate for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a specified index, meaning your payments can go up or down.

Q2: How much money do I need for a down payment?

While a 20% down payment is often recommended to avoid private mortgage insurance (PMI), many loan programs allow for much lower down payments. Conventional loans may require as little as 3–5%, while FHA loans can go as low as 3.5%. The exact amount depends on your lender, loan type, and financial profile.

Q3: What credit score do I need to qualify for a home loan?

Credit score requirements vary by loan program and lender. Generally, a score of 620 or higher is needed for conventional loans, while FHA loans may accept lower scores. A higher credit score typically results in better interest rates and loan terms.

Q4: What documents are required when applying for a home loan?

Most lenders require proof of income, tax returns, bank statements, employment verification, and identification. Additional documents may be requested depending on your financial situation. Having these prepared in advance can speed up the approval process.

Q5: Can I get a home loan if I am self-employed?

Yes, self-employed borrowers can qualify for home loans, but they may need to provide additional documentation. Lenders often review two years of tax returns and consistent income history. Proper financial records improve your chances of approval.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.