Navigating the world of loans can feel overwhelming, but understanding the underlying mechanics of your payments is key to financial empowerment. Whether you’re considering a mortgage, a car loan, or personal financing, mastering the calculation of loan payments is a fundamental skill. This comprehensive guide will demystify the process, breaking down complex concepts into simple, actionable steps. By the end, you’ll have a clear understanding of how your payments are determined, enabling you to make informed decisions and manage your debt effectively.

What is a Loan and Why Understand Its Calculation?

A loan is essentially a sum of money borrowed by one party from another, with the expectation that the money will be repaid, often with interest. From a borrower’s perspective, a loan provides immediate access to funds for various needs, such as purchasing a home, funding education, or starting a business. The lender, in turn, earns a profit through the interest charged on the principal amount.

Understanding the calculation of loan payments isn’t just about knowing a number; it’s about comprehending your financial commitment. It allows you to budget accurately, compare different loan offers, and identify potential savings. Without this knowledge, you might pay more than necessary or struggle to meet your repayment obligations, potentially impacting your credit score and long-term financial health. The process of calculating loan payments, often called amortization, helps both borrowers and lenders structure predictable repayment schedules.

Key Components of Any Loan

Every loan, regardless of its purpose or size, is built upon a few core components that directly influence its cost and repayment structure. Familiarizing yourself with these terms is the first step towards mastering loan calculations.

- Principal: This is the initial amount of money you borrow. If you take out a $20,000 car loan, your principal is $20,000.

- Interest Rate: Expressed as a percentage, the interest rate is the cost of borrowing the principal. It’s the fee charged by the lender for the use of their money. Higher interest rates typically mean higher monthly payments and a greater total cost over the loan’s life.

- Loan Term: This refers to the duration over which you agree to repay the loan. Terms can range from a few months for personal loans to 15 or 30 years for mortgages. A longer term generally results in lower monthly payments but often means paying more interest overall.

- Payment Frequency: Most loans require payments on a monthly basis. However, some might allow bi-weekly or quarterly payments, which can subtly impact the total interest paid due to how interest accrues.

- Annual Percentage Rate (APR): The APR represents the total cost of borrowing, including the interest rate and certain additional fees, expressed as a yearly percentage. It provides a more comprehensive picture of the loan’s true cost, making it easier to compare different offers. For more details on APR, visit the Consumer Financial Protection Bureau.

Step-by-Step Guide to Loan Calculation

While the underlying formulas can be complex, you don’t need to be a mathematician to understand your loan payments. Modern tools and simple logic can help you grasp the essential outcomes.

Step 1: Gather Your Loan Details

Before you can perform any calculation, you need to know the specific parameters of your loan. This includes the principal amount you wish to borrow, the annual interest rate (not just the nominal rate, but the actual rate applied to your loan), and the desired loan term in years or months. Having these figures readily available ensures accuracy in your estimates.

Step 2: Understand the Impact of Interest

Interest is the core cost of borrowing. It can be calculated in different ways, but most consumer loans use a form of compound interest, where interest is charged not only on the principal but also on the accumulated interest from previous periods. This is why paying down your principal quickly can potentially save you a substantial amount over time. Early payments often apply more heavily to the interest portion of your loan.

Step 3: Calculating Your Monthly Payment (Amortization)

This is often the most critical calculation for borrowers. While the exact formula involves exponents and specific financial terms, the principle is straightforward: your monthly payment is designed to gradually pay off both the principal and the interest over the loan term. Early in the loan, a larger portion of your payment goes towards interest, and a smaller portion towards principal. As the loan matures, this ratio shifts.

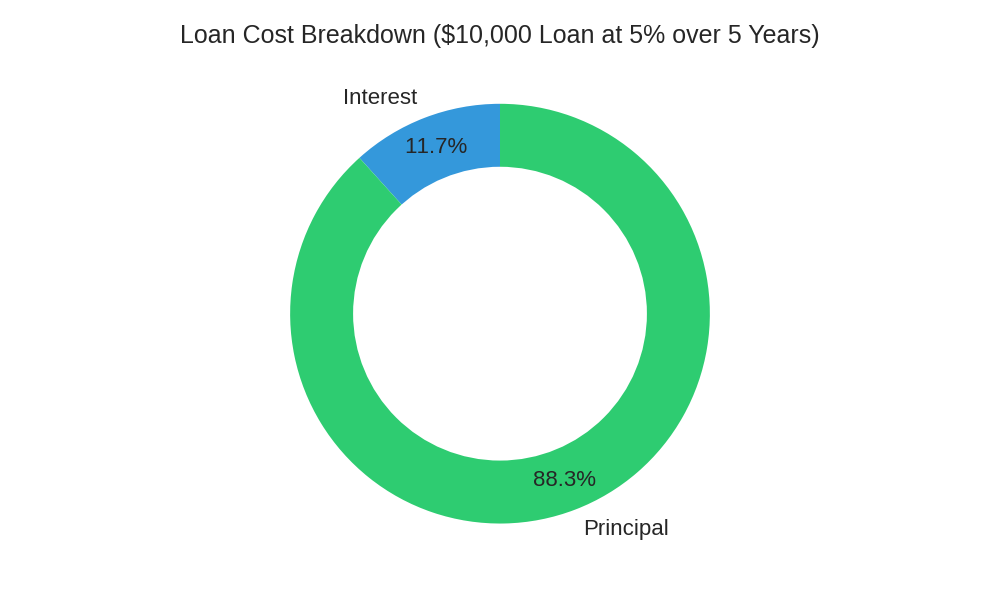

Let’s illustrate with a common scenario. If you borrow $10,000 at an annual interest rate of 5% over a 5-year term, your monthly payment will be approximately $188.71. Over the entire 60 months, you would pay a total of $11,322.60, which includes $10,000 in principal and $1,322.60 in interest.

Below is a simplified repayment table, also known as an amortization schedule, for a loan of $10,000 at 5% annual interest over 5 years. This table illustrates how your balance decreases over time.

| Year | Remaining Balance | Monthly Payment |

|---|---|---|

| Start | $10,000.00 | N/A |

| End of Year 1 | $8,294.62 | $188.71 |

| End of Year 2 | $6,500.27 | $188.71 |

| End of Year 3 | $4,611.85 | $188.71 |

| End of Year 4 | $2,624.08 | $188.71 |

| End of Year 5 | $0.00 | $188.71 |

Monthly Payment Calculator

Step 4: Total Interest Paid and Total Cost

Beyond the monthly payment, it’s crucial to understand the total interest paid over the life of the loan. This is simply the sum of all your monthly payments minus the original principal amount. For the example above ($10,000 at 5% over 5 years), the total payments are $11,322.60, meaning you pay $1,322.60 in interest. Knowing this figure helps you assess the overall expense of borrowing and compare it against other financial options.

Factors Affecting Your Loan Payments

Several variables can influence the final `calculation of loan` payments and the overall cost. Being aware of these can help you seek better terms.

- Credit Score: A higher credit score generally qualifies you for lower interest rates, which can significantly reduce your monthly payments and total interest. Lenders view borrowers with excellent credit as less risky.

- Down Payment: For secured loans like mortgages or auto loans, a larger down payment reduces the principal amount borrowed. This directly lowers your monthly payments and the total interest you’ll pay over the loan term.

- Fees: Loans can come with various fees, such as origination fees, application fees, or closing costs. While not always directly part of the monthly payment calculation, these fees increase the overall cost of borrowing and are often reflected in the APR.

- Repayment Schedule: While monthly is standard, some loans offer bi-weekly payments. Paying every two weeks (26 payments a year) instead of once a month (12 payments) effectively adds an extra monthly payment each year, accelerating principal repayment and potentially saving interest.

Strategies to Reduce Your Loan Costs

Understanding how loans are calculated empowers you to explore ways to minimize your financial burden.

- Making a Larger Down Payment: As mentioned, this reduces the principal, leading to lower monthly payments and less interest paid overall.

- Considering a Shorter Loan Term: While this often means higher monthly payments, it can drastically reduce the total interest paid over the life of the loan. For instance, a 15-year mortgage typically saves tens of thousands in interest compared to a 30-year mortgage.

- Improving Your Credit Score: Before applying for a loan, taking steps to boost your credit score can qualify you for more favorable interest rates. This is one of the most impactful long-term strategies. Visit the Federal Reserve website for resources on credit.

- Considering Refinancing Your Loan: If interest rates drop or your credit score improves, you might be able to refinance your existing loan to a lower rate, potentially reducing your payments or the total interest.

- Making Extra Payments: Even small additional payments directly towards the principal can significantly cut down the total interest paid and shorten your loan term. Always ensure extra payments are applied to the principal, not future interest.

FAQ: Common Questions About Loan Calculation

Can I pay off my loan early?

Most loans allow early repayment without penalty, but it’s crucial to check your loan agreement for any prepayment penalties. Paying early reduces the total interest you’ll owe, saving you money.

What is an amortization schedule?

An amortization schedule is a table detailing each periodic loan payment, showing how much goes towards interest and how much towards the principal.

Does my interest rate affect the total loan cost?

Yes, the interest rate has a significant impact on the total amount you repay. Even a small difference in rates can result in paying much more or less over the life of the loan. Comparing interest rates before borrowing is essential.

What happens if I miss a loan payment?

Missing a payment can result in late fees, damage to your credit score, and increased interest costs. Repeated missed payments may lead to default. If you’re struggling, contact your lender early to discuss possible solutions.

Can loan calculators give exact results?

Loan calculators provide accurate estimates based on the information entered, but they may not include fees, insurance, or variable interest changes. Always review the final loan terms from your lender for precise figures.

How does loan term length affect payments?

A longer loan term lowers monthly payments but increases the total interest paid. Shorter terms usually cost less overall, even though monthly payments are higher. Choosing the right term depends on your budget and financial goals.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.